Welcome to the weekly letter (#20) from TheIntersection team. Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: The Bank of England softens its stance on stablecoins

- Data: Stock tokens found their catalyst, and it was a blast

- Analysis: Tokens for all? Really?

- Opinion: Tokenized Stocks Are Up 422%. Most of Them Aren't Stocks

- Our weekly events round-up

And it's all free! Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

News in Brief

Coinbase brings tokenised U.S. stocks to international . Coinbase has announced plans to launch tokenised U.S. equities for non-U.S. customers next month. The tokens will be backed 1:1 by underlying shares and are expected to include shareholder rights, dividend payments and the ability to be used as collateral or lent for yield. Why it matters: Coinbase is positioning itself to offer stocks, crypto and derivatives within a single platform, further blurring the line between traditional and digital markets.

SEC debates scope of tokenisation sandbox. The SEC's proposed "innovation exemption" for tokenised securities has reportedly been delayed as regulators debate whether relief should apply only to issuer-backed tokenised assets or extend to third-party wrapped securities. Why it matters: The outcome could determine how quickly tokenised securities scale in the U.S. and which business models are permitted to participate.

Ondo expands access to tokenised stocks through MetaMask. Ondo Global Markets has made more than 430 tokenised U.S. stocks and ETFs available directly through MetaMask for eligible users outside the United States, enabling mobile-first access without traditional brokerage accounts. Why it matters: Tokenised equities are increasingly moving beyond institutions and becoming accessible through mainstream crypto wallets.

Deep Dive — The Bank of England softens its stance on stablecoins

The Top Line

The UK has taken a significant step towards bringing stablecoins into the financial mainstream. After months of industry criticism, the Bank of England has eased several key elements of its proposed stablecoin framework, dropping limits on how many stablecoins individuals can hold and relaxing reserve requirements for issuers. The move signals a shift from caution towards controlled adoption as regulators attempt to balance innovation with financial stability.

The Details

When the Bank of England first outlined its plans for regulating sterling-backed stablecoins, the response from industry was swift. Banks, fintechs and crypto firms argued that proposed holding limits and strict reserve rules would make it difficult for a UK stablecoin market to develop, especially as the US and EU moved towards more permissive frameworks. In its updated framework, the Bank has now abandoned plans to cap the amount of stablecoins individuals can hold. Instead, it will impose an initial £40 billion issuance limit on each systemic stablecoin issuer. The central bank has also loosened reserve requirements. Issuers will be allowed to hold up to 70% of backing assets in short-term government debt, up from the previously proposed 60%, with the remainder held as deposits at the Bank of England.

The changes may sound technical, but they have a major impact on the economics of stablecoin issuance. Government bonds generate yield, making stablecoin businesses more commercially viable while still maintaining a high-quality reserve base. Yet the Bank remains cautious. Officials continue to warn that large-scale stablecoin adoption could draw deposits away from traditional banks, potentially affecting lending and credit creation across the economy. The Bank of England hasn't thrown the doors open to stablecoins, but it has clearly moved away from the restrictive approach it initially proposed.

The revised framework suggests regulators now see stablecoins as a legitimate part of the future payments landscape. The challenge from here is ensuring the UK remains attractive enough for issuers to build there, while maintaining the safeguards policymakers believe are necessary for a system that could eventually operate at national scale.

Sources

- Reuters: Bank of England softens stablecoin rules in final policy draft

- Financial Times: Bank of England dilutes stablecoin rules with plan for £40bn issuer limit

- Reuters (background): Bank of England faces calls from UK lawmakers to ease stablecoin plans

- Reuters (background): Stablecoin demand may soon fade, BoE's Greene says

Stock tokens found their catalyst, and it was a blast

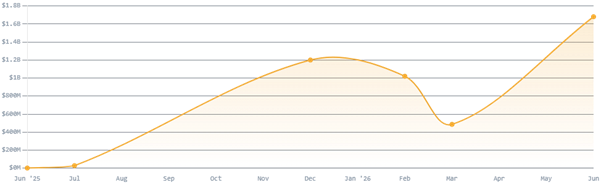

Tokenised stocks entered 2026 worth roughly $2.23 billion by the broadest measure and spent the first quarter consolidating. Q2 is where the line bent. On-chain trading hit an all-time daily high of $3.57 billion on 18 May, the same week the SEC published an innovation exemption that allows crypto-native platforms to offer on-chain US equities without full broker-dealer registration. Then SpaceX listed, and the category recorded its biggest month ever — $4.3 billion traded in 30 days.

The honest framing for readers: this is still around 0.001% of the $134 trillion global equity market — the same fractional starting point stablecoins occupied in 2020. The interesting part is not the absolute size but the slope, and the fact that the institutional rails (DTCC, Nasdaq, NYSE/ICE) are being laid at the same time.

Chart : Tokenised stock market capitalisation - On-chain value, USD · Jun 2025 → Jun 2026 · sources blended (RWA.xyz / CoinGecko / The Block)

Chart: Monthly on-chain spot volume - USD billions · four straight months above $4B before the June record

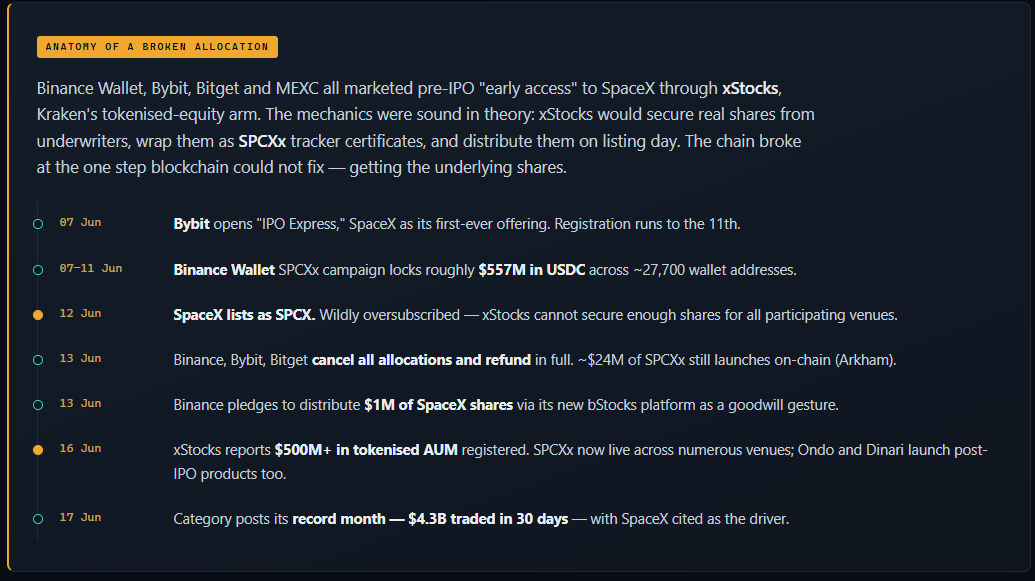

SpaceX completed its IPO on 12 June 2026 under the ticker SPCX, reserving a record 20% of the deal for individual buyers. The demand overwhelmed everyone — traditional brokerages filled retail orders only partially, and the crypto distribution chain broke outright.

The lesson most investors might focus on: creating a token is easy; sourcing the asset behind it is the whole game. Tokenisation added a link to the chain rather than removing one — every wrapper still depended on a centralised party winning an allocation in a deal where allocations were the scarce resource. As ARK's Lorenzo Valente put it after seeing dozens of venues advertise the same exposure, the real question was what, exactly, a buyer was buying.

General US equity token flow: perps still dominant

Strip out the SpaceX noise, and the structural picture is consistent with the prior quarter. xStocks (Backed Finance × Kraken) remains the spot leader — over $25 billion cumulative volume since its June 2025 launch, eight of the top eleven tokens by holder count, and roughly 68% of the top 25. Ondo Global Markets leads on listed-asset breadth and issuance value. But the larger flow story sits in perpetual futures: RWA perp volume hit $524.8 billion in Q1 alone, already dwarfing the $313 billion recorded across all of 2025, with Hyperliquid's HIP-3 framework driving over a third of that venue's total volume.

Table: SpaceX token timeline

Table: Stocks tokens across various issues

Chart: Tokens vs Perpetual Futures

Tokens For All?

By Damian Black

Tokenisation for everything, everywhere. That’s what some pundits are starting to talk about. In this view, tokens are seen as just another form of digital wrapper, another form of securitisation, if you want, superseding newer wrappers and structures such as exchange-traded funds, and sometimes even hosting them within the structure.

The idea is to create seamless, instant, real-time, 24-hour liquidity for anything from ETFs through Treasuries to private credit. And the big asset management firms are embracing the token at great speed – as are some of the mainly American exchanges. Nasdaq, for instance, recently published a white paper finding that more than half of firms expect to use tokenised collateral by the end of the year.

So, what’s going on? Is this really a “quiet revolution powered by asset tokenisation” as the World Economic Forum claimed in August 2025, or just everything much as it was inside a different wrapper?

There can be no doubt that the big institutions are getting into the game. In May, State Street announced a cautious but determined foray into tokenised assets. The $5.6 trillion asset manager previously viewed as a ‘tech naysayer’ says it wants to be an “early adopter” of tokenised funds; it’s indicative of a wider shift.

BlackRock, too, has been making no secret of its wish to offer tokenised services. It recently upgraded its $2.3 billion BUIDL tokenised fund to become a productive asset – meaning investors can use their tokenised funds to earn yields, an historic first. This new product has been strategically launched in the UAE because it benefits from the regulatory clarity provided by the dedicated Virtual Assets Regulatory Authority.

Clarity and on/off ramps

Clarity will be key to seeing the prediction of tokens everywhere for everything to come true. In the US, SEC chairman Paul Atkins gave a keynote speech in November, highlighting the importance of a “clear token taxonomy”.

“Developers, exchanges, custodians, and investors have been trying to navigate in a fog, without SEC guidance,” he said. “If the United States insists on making every on-chain innovation run through a securities-law minefield, those innovations will migrate to jurisdictions that are more willing to distinguish among different kinds of assets, and [...] write down the rules in advance.”

Another key issue is interoperability, which appears to be a major hurdle faced by stablecoins – the wheelhouse of tokenization. As a16zCrypto notes, last year, transactions in digital currency totalled an estimated $46 trillion – nearly 20 times that commanded by PayPal and triple that of Visa.

The facility is certainly there – you can send a stablecoin far and wide in less than a second for less than a cent. But as16z caveats: “What remains unsolved, however, is how to connect these digital dollars to the financial rails people actually use already every day — in other words, on/off ramps for stablecoins.”

Still a long way to go...

Toby Nicole is the founder of I Am My Own Asset and teaches her 39,000 TikTok followers the ins and outs of cryptocurrency, stablecoins, and tokenisation. She agrees that on- and off-ramps are an obstacle that the tokenisation industry will have to surmount before it can become available to a wider range of investors.

“I help everyday people learn to understand and position themselves in our evolving new financial system and the infrastructure being built around it,” Nicole says. “The on-and-off ramping problem is still the biggest friction point for retail investors and institutions. Getting dollars into the system and back out again is where the vision has to deal with reality.”

Right now, that reality consists of “know your customer delays, limited banking access and platforms freezing customers’ accounts without advance warning – I've seen this first-hand with my own community followers”. Matthew Schneider is CEO at Building, a company that specialises in the tokenisation of real-world assets (RWA). He believes the shift needed to make stablecoins interoperable is underway.

“Tokens will become much more common, but not because everything suddenly becomes liquid or accessible.” The coming shift is that financial instruments will become more programmable, more transparent, and easier to move between systems. Right now, stablecoins suffer from what Schneider calls a “reconciliation problem”.

“In theory, a fiat-backed stablecoin is simple: one token should correspond to one dollar, or dollar-equivalent asset, held somewhere off-chain,” he tells me. “The on-chain representation has to remain aligned with off-chain reserves, redemption rights, banking access, custody, and liquidity.”

The problem arises when stablecoin holders lose confidence in the digital asset’s ability to be redeemed like-for-like in fiat currency. This can cause a stablecoin to “detach from its intended value”.

“This is why reserve quality, reporting frequency, redemption mechanics, and independent oversight matter so much,” explains Schneider. “The same problem applies more broadly to tokenisation. When that asset is represented digitally, the token is only as reliable as the data and legal structure behind it. If ownership rights, asset performance, valuation, or reporting are not properly maintained, the on-chain instrument can become detached from the real-world asset it is supposed to represent.”

However, Schneider points out that this problem is not unique to blockchain. “Private markets already suffer from opacity,” he says. “Investors in real estate, private credit, or private equity often receive limited reporting compared with public markets.” However, poorly structured tokenisation runs the risk of exacerbating this. “It can actually amplify the problem if assets are distributed and traded without a better data infrastructure underneath.”

Time to clean house

Crypto expert Mark Langshaw of Echo Finance agrees that tidying up the digital industry’s messy infrastructure will be the key to ubiquitousness.

“Obviously, following the rapid expansion of the crypto market, we’ve seen projects launch without having efficient systems and strong infrastructure in place first. When you look at fiat-backed stablecoins, there needs to be complete transparency regarding their reserves.”

He adds: “Just like we prioritise due diligence when partnering with firms in the mortgage sector, crypto consumers need to know exactly what is backing these assets. A lack of regular, independent audits simply doesn’t provide the best outcome for consumers.”

Does he think tokenisation can spread by opening up the investment game to a wider field of smaller, retail investors? Langshaw concedes that fractionalization makes the investing process more streamlined and therefore more accessible. However, sustained growth on the back of this alone will not be possible.

“You have to form a solid foundation before leaping into continued growth,” he tells me. “If retail investors are going to be heavily involved in tokenised assets, there needs to be complete transparency.”

Langshaw suggests there is a learning curve to be surmounted, as potential investors familiarise themselves with the complex terms and conditions that apply to crypto-based assets. “[As with] complex products like equity release, platforms offering tokenised assets need to allow consumers additional time to digest the terms and other important information related to this type of product,” he says. “Obviously, regulators are becoming more focused on consumer rights in the digital asset space. I think these are positive changes that will lead to far better consumer outcomes across the industry over the next decade.”

Tokens – a new way to lose money?

However, those who dream of big bucks by starting small in fractionalized tokenized assets might want to manage their expectations a little. “Tokenisation does open the door and being able to own a fraction of assets that used to have $100K minimums is genuinely a big deal,” concedes Nicole, “but that does not automatically mean an even playing field for retail investors. Most people still do not understand what they are buying or the custodial risk that comes with it – so without education behind it, they really just found a new way to lose money.” Surely this is really just a case of “meet the new boss, same as the old boss” – with big players like BlackRock getting richer as smaller investors struggle?

“When it comes to BlackRock and institutions muscling in, the ‘meet the new boss’ question is something I think about a lot,” Nicole says. “The infrastructure being built around ISO 20022, the XRP Ledger and on-chain settlement was designed to move value more efficiently – but I question who ends up controlling these rails.”

Rather ominously, she adds: “Right now the biggest players like BlackRock [and] JP Morgan are positioning to own them – and that should concern everyone.” The best way to stop this happening is through better education: “I, as a retail investor, only win if the technology stays permissionless and everyday people learn how to use it before institutions lock in the big advantage for good.” But make no mistake – the big guns are firing loud and clear and “tokens will be everywhere before long”. And not only thanks to BlackRock and JP Morgan's tokenized treasury funds.

“Real estate is being put on the blockchain, stocks and bonds are next, and we can own fractional pieces of all of it,” Nicole says. “We will be able to trade them 24/7, cutting out the middleman. Stablecoins are just the currency flowing between the tokenized assets, they are what is making the whole system move.”

Regulations like the stalled Clarity Act, which aims at establishing a clear regulatory framework for digital assets, will be another key driver towards “mass adoption” as investors and consumers feel better protected – memories still loom large of the FTX scandal in 2022, which saw the $32 billion crypto exchange wiped out after it emerged that customers’ funds were misused.

Nicole adds: “Once these guardrails are solid [and] people understand what they are actually holding, then tokens being everywhere will not just be a prediction – it will become our reality.”

Tokenized Stocks Are Up 422%. Most of Them Aren't Stocks

by Gabor Gurbacs, CEO OpenAssets

The headline number is real. Binance Research put tokenized stocks up 422% since early 2025, the fastest-growing slice of a real-world-asset market that has more than tripled over the same period. The trajectory is not hard to read. Treasuries were the warm-up; equities and the funds built on them are where tokenization goes next. The asset class fund managers actually live in, and the one large enough to carry the market from a $30 billion niche into the trillions. So the direction is not in question. What's in question is what most of that 422% actually is.

A large share of it is synthetic: tokens that mirror a stock or fund's price without conveying ownership of it. No share. No unit. No vote. A price feed, not a security. When tokenized SpaceX shares traded this year, they moved with the company's valuation while conveying no ownership in it. That distinction is the whole story, and it is where the equities phase gets hard.

Why Treasuries were the easy asset

A tokenized Treasury is close to a wrapper around a single, well-behaved instrument. You hold it, it pays, you redeem it. One issuer. Few corporate actions. The question of who owns it rarely gets complicated. That simplicity is exactly why Treasuries went first. Equities and ETFs drag the entire apparatus onchain with them. Dividends. Splits. Tender offers. Proxy votes. Corporate actions that have to reach the right holder on the right date. And underneath all of it, the one record everything else depends on: the authoritative account of who owns which share or unit. Strip that away and a tokenized security is just a number that moves.

An ETF is the clearest case

Consider what makes an ETF trustworthy. Its price tracks net asset value only because authorized participants can create and redeem units against the underlying basket. A token that mirrors an ETF's price without that right isn't an ETF; it's a tracker of a tracker. And that same machinery is why the wrapper scaled: the ETF took the better part of two decades to reach its first trillion dollars and now sits near $22 trillion. It compounded because the plumbing underneath it held, and tokenized equities inherit that dependency.

The bottleneck is bookkeeping, not trading

Tokenizing the price of a security is easy, which is why so many have done it. Tokenising the ownership of one, in a form that an issuer, a regulator, and a court would all recognise, is the actual work. It lives in the part of the market that rarely makes headlines: the transfer agent, the issuer-of-record, the recordkeeping layer that maps tokens to legal owners and keeps that map correct through every corporate action. The established players are already organizing around this. Securitize, moving into tokenized equities, built the ownership record in rather than routing around it. DTCC – the entity behind nearly every U.S. stock trade – received SEC authorization to tokenize Russell 1000 names, major ETFs, and Treasuries, and built the service specifically to preserve existing ownership rights and legal protections. In both cases, the record came first.

Why this has to be a shared layer

Tokenized equities and funds will not trade in one place. They will move across venues, custodians, and chains. If every platform keeps its own private ledger of ownership, a tokenized share or unit means one thing here and something else there, and the record stops being trustworthy the moment it crosses a boundary. The ownership layer only works if it behaves consistently wherever the token travels. Which makes it a standards problem, not a single-company product.

What the 422% is really measuring

Right now, that number mostly measures appetite. It tells you investors want equity and fund exposure with onchain mechanics: 24/7, fractional, fast. That demand is genuine, and it is not going away.But appetite is not infrastructure. Global equities are a market worth more than $120 trillion, and moving any real share of it on-chain will be won by whoever can prove the token is the security: that what trades on-chain carries the ownership, the rights, and the record behind it.The price was always going to be easy to put onchain. Ownership is the product. The next phase of tokenization belongs to the firms building that layer.

Gabor Gurbacs is a Wall Street–trained strategist and technology entrepreneur with deep expertise in digital assets and tokenized markets. He previously led digital asset strategy at VanEck, helped pioneer industry-standard crypto indices, and advised institutions and regulators globally on market structure. Today, he leads OpenAssets as CEO in building the next generation of financial infrastructure.

Events on our radar

- TOKEN2049 Singapore, 7–8 October 2026, Singapore - tickets HERE

- WebX Asia (Tokyo), 13–14 July 2026, Tokyo, Japan - tickets HERE

- Blockchain Futurist Conference (Toronto), 21–22 July 2026, Toronto, Canada - tickets HERE

- European Blockchain Convention 12, Europe’s Deal Floor for Digital Assets. BARCELONA · 16-17 SEPTEMBER 2026 - tickets HERE