By Anna Fedorova

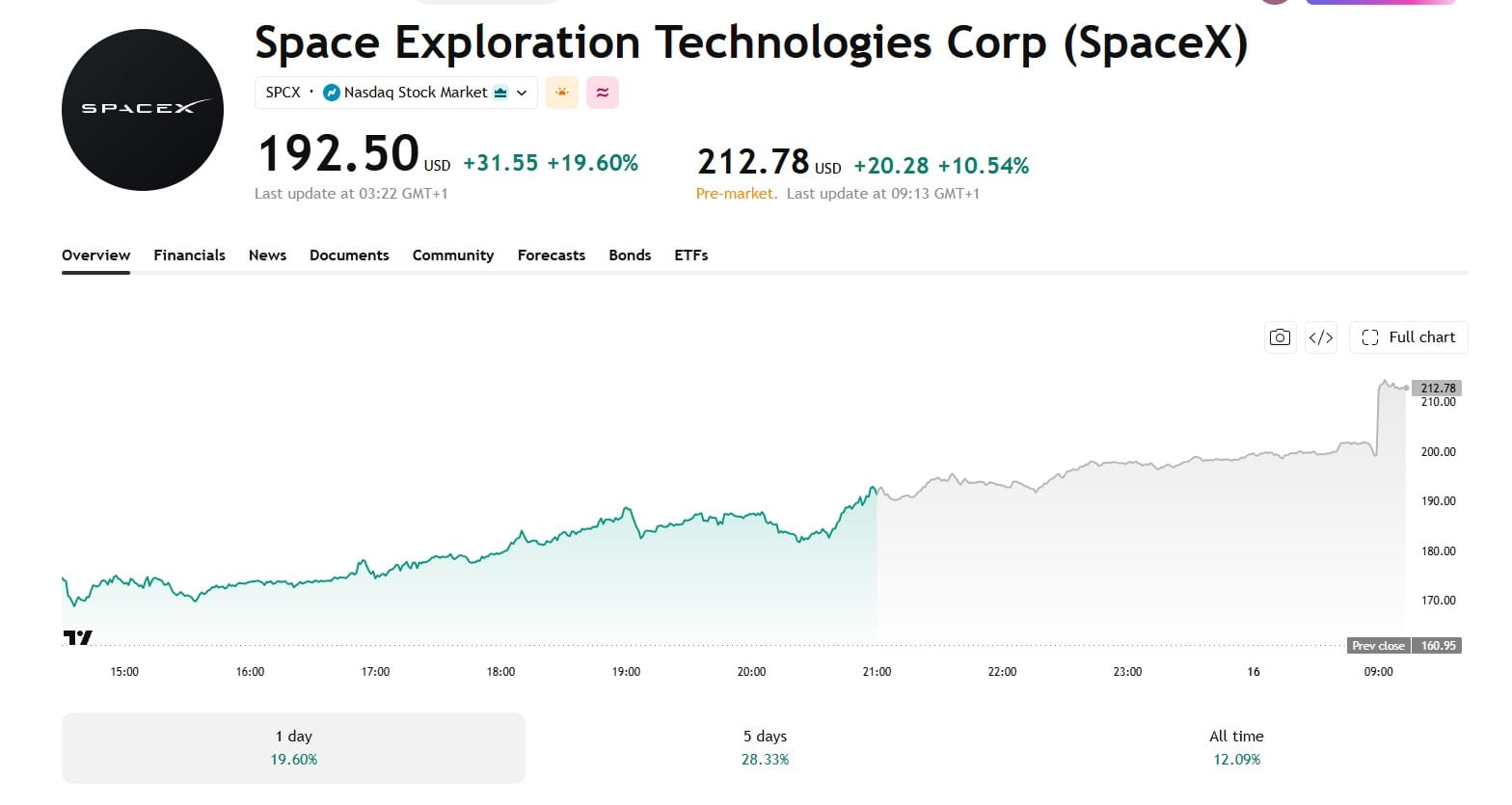

The SpaceX IPO kicked off a frenzy of tokenized stock trading – at least, when taken as a proportion of the modestly-sized tokenization market. Over the last 30 days, tokenized stocks saw $4.3 billion of trading volume on-chain, according to data from RWA.xyz cited by the Kobeissi Letter – the highest monthly volume since inception and 140% jump year-to-date (YTD). Many market watchers saw this IPO as the first real-life test of tokenisation. For the first time ever, investors would have the opportunity to access a soon-to-be-launched stock on the blockchain, with the possibility of trading it 24/7, regardless of the Nasdaq’s opening hours. Now that the launch is done and dusted, the question is: was it a pass or a fail? The answer depends on who you ask.

Promises, promises

As the week of the IPO arrived, the hype around it reached fever pitch – and that extended to the tokenised market. Crypto exchanges Kraken, Bybit and Binance had rolled out major pre-IPO tokenisation campaigns, pre-IPO perpetuals were trading, and investors rushed to pre-order tokenised SpaceX (SPCX) shares and derivatives.

In a newsletter a few days ahead of the historic launch, Bloomberg reporter Suvashree Ghosh, who has been closely watching the digital asset market, noted that the listing has become “an unexpected referendum on tokenisation itself” – but the verdict would come only after the stock was live on the Nasdaq. The deciding factor would be whether investors would still trade tokenized versions of SpaceX once it’s live, or abandon them for the real shares on traditional exchanges.

The promise of tokenisation in this case was simple: retail investors had been largely locked out of SpaceX while VCs, sovereign funds and institutions gained early access. Tokenised equities could level the playing field, living up to crypto’s promise of “democratising” investment – providing access to anyone, anywhere, anytime.

But the big question, according to Nathanael Cohen, CIO at crypto hedge fund Indigo Fund, quoted in the Bloomberg piece, was whether there would be adequate liquidity available on tokenised platforms – an age-old problem for crypto tokens, which he called “a chicken-and-egg situation”. Given the size of the SpaceX IPO and the hype around it, liquidity constraints could become a really big problem.

The product selection

Liquidity wasn’t the only problem, though. Before the IPO even launched, the selection of tokenised products supposedly tracking SpaceX was confusing. Simply buying an “SPCX” token on-chain could give you a whole raft of different exposures depending on the issuer. ARK Invest’s director of research, Lorenzo Valente, tweeted: “I've seen 40 exchanges and wallets advertising SpaceX stock. What exactly am I buying?”

There were share-backed tokens, redeemable one-to-one for real SpaceX shares – from xStocks ahead of the launch, and from Backpack and Ondo once SpaceX was live. But there were also perpetuals offering synthetic derivative exposure to SpaceX.

Then there was the Paimon SPV SPCX token, launched by Paimon Finance on BNB Chain. This one doesn’t provide exposure to SpaceX shares in any way at all, but rather represents fractional ownership in a British Virgin Islands (BVI) Special Purpose Vehicle (SPV) that invests in venture capital funds with SpaceX exposure – a claim on a fund, not on the shares.

Then there were so-called structured claims from PreStocks and Republic. Both are synthetic trackers that also don't offer any actual equity exposure to SpaceX – only exposure to the economic performance of the company, and both traded ahead of the IPO.

Republic's rSPAX is a "Mirror Token" – a tokenized contingent payout note, essentially an IOU from Republic's subsidiary rather than a share. It confers no ownership, voting or dividend rights, and pays out only on a liquidity event such as the IPO, based on SpaceX's per-share value at that time.

Meanwhile, PreStocks has Special Purpose Vehicles (SPVs) that hold actual SpaceX shares or equivalent equity exposure. However, now that SpaceX is trading publicly, holders of the PreStocks SPACEX token must manually swap it for $SPCXx or another tokenised SpaceX product before 12 March 2027, or their tokens become worthless. And they can’t do so cleanly yet: the underlying shares unlock in tranches over roughly six months, so the token trades at a steep discount in the meantime.

In short, it was a somewhat confusing alphabet soup even before SpaceX started trading on the Nasdaq. But when it did, a bigger problem emerged for the exchanges that had promised retail investors on-chain access to real SpaceX shares.

The xStocks failure

Once the IPO allocation was distributed, investors on crypto exchanges Binance, Bitget and Bybit discovered they hadn’t received their shares – supposed to be distributed by Kraken’s tokenised equity platform, xStocks. The underlying stocks simply weren’t there. The exchanges were forced to cancel all their promotional campaigns and refund more than $1 billion to disappointed customers.

In all fairness, it wasn’t a failure of the technology. The technology worked just fine. The problem was scarcity, created in a seemingly artificial manner – despite promising a 30% retail allocation, Musk ended up reserving just over 20% for retail investors. With the offering already oversubscribed, that meant many retail investors – not only those on crypto platforms but also those buying through traditional brokerages – weren’t able to get their hands on SpaceX tokens.

And to be fair to the exchanges, many users did receive some allocation – reportedly 4.3 SpaceX shares from a fixed pool – and various other rewards to sweeten the deal. So, as Fortune’s finance and crypto editor Jeff John Roberts put it, it was a “bummer” for investors, but “hardly a fiasco”.

He sees it as simply part and parcel of constrained supply coming up against insatiable demand – and crypto platforms, being newer to the market, naturally ended up at the back of the queue. And, crucially, the possibility that this would happen was disclosed in the small print, so investors should have known what they were getting themselves into.

But some were not quite so sanguine. Tom Farley, CEO of Bullish, tweeted: “Maybe tokens should actually be approved by the issuer and therefore be the actual underlying share. Just a thought.”

After the storm

Once the dust settled, though, it turned out the tokenised shares that were available were doing what they said on the tin. They were trading 24/7 and tracked the price pretty closely once the stock was trading on Nasdaq (apart from PreStocks, which isn’t quite like-for-like exposure). The products that held real shares worked as they were supposed to. Binance's whole-share SPCX orders were executed through an introducing broker and cleared through Alpaca – real shares, cleared and settled under Nasdaq rules. Even the refunds were sorted out on IPO day.

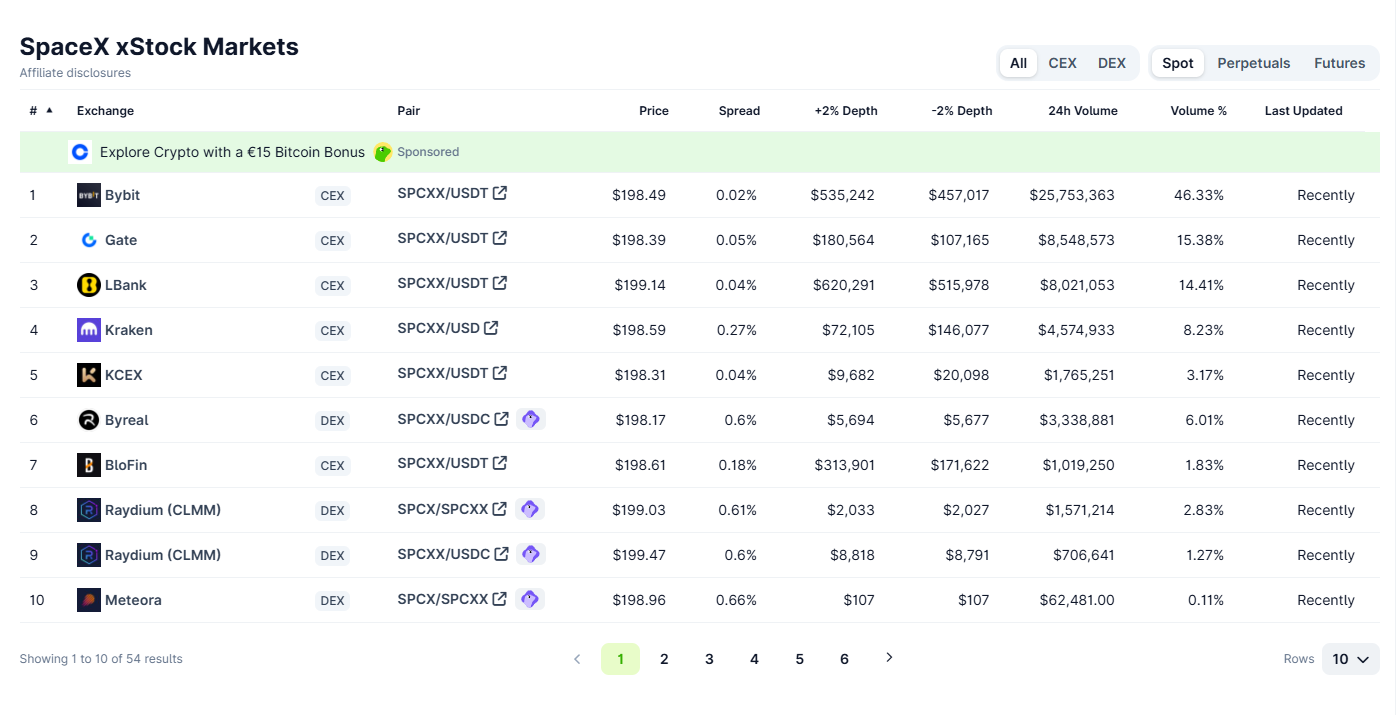

And there was some trading volume, much of it on Solana – a blockchain designed for fast transactions. Solana saw $100 million in 24-hour trading volume on Monday, 15 June, some 40% of that in Backpack Securities' SPCX token and the rest in competing products. And for the nascent blockchain sector, that number is impressive.By 17 June, the leading xStocks SpaceX token (SPCXX) was turning over roughly $40-48 million a day across 36 venues, with Bybit alone accounting for nearly half. That’s real, tradeable liquidity, even if it is concentrated in just a handful of centralised exchanges, and even if it remains a tiny fraction of the Nasdaq stock's turnover.

Tokenised stocks are slowly growing into a legitimate alternative to traditional market trading. As Gabor Gurbacs, CEO of OpenAssets, notes: “The SpaceX IPO demonstrated the potential of tokenised stocks. Despite initial hurdles, features like 24/7/365 markets enable broader participation from a wide range of investors.”

The verdict

By all accounts, then, it would be unfair to call the SpaceX tokenised stock rollout a fiasco. But it’s still a long way from a resounding victory. The reality is that the tokenised equity market is still tiny and niche compared to traditional markets. And the question is, what happens when traditional stock exchanges – like NYSE and Nasdaq – begin trading around the clock? Will tokenised equities continue to gain momentum due to their cross-border availability, instant settlement, and simpler user experience? Or will they lose their main appeal when the rest of the market is trading 24/7?

On top of this, one of the main concerns remains: tokens may offer access, but they don’t offer equivalence. Shareholder rights, market depth, and redemption certainty are still firmly reserved for traditional stock investors. And with SpaceX, the added irony is that the products promising to democratise access were the ones that couldn't deliver it, while others barred US investors outright.

The SpaceX IPO proved that tokenisation can work in practice. But if it is to become a real success, it needs more participation, deeper liquidity and reassurance that investors will be able to get their hands on tokenised shares when the time comes.

Gurbacs is convinced: “Future mega IPOs will likely feature more tokenised options, facilitating broader access to investors.” With a number of mega-IPOs slated for launch later this year, including OpenAI and Anthropic, we will soon find out.