Welcome to the weekly letter from TheIntersection team. Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: UK regulators map out digital assets vision

- Data: The UAE races ahead in RAW tokens and stablecoins

- Worth reading: The case for Euro Stablecoins

- Analysis: BlackRock's $2.3bn UAE Experiment

- Analysis: Stablecoins: just how stable are they?

- Our weekly events round-up

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

News in Brief

OFA Group Lands $7.5 Million Contract for Florida Real Estate: Nasdaq-listed OFA Group announced a $7.5 million tokenisation agreement to bring a $500 million residential real estate redevelopment project in Vero Beach, Florida, onto the blockchain. The infrastructure will be handled through its proprietary Hearth RWA platform.

Datavault AI Reports Explosive Growth: In its Q1 business update, Datavault AI (NASDAQ: DVLT) revealed it signed approximately $750 million in tokenisation contracts in the first quarter alone and expects to recognise nearly $100 million in fees this year. The company reiterated a $200 million revenue target for the year, underscoring aggressive institutional demand for data and asset monetisation infrastructure.

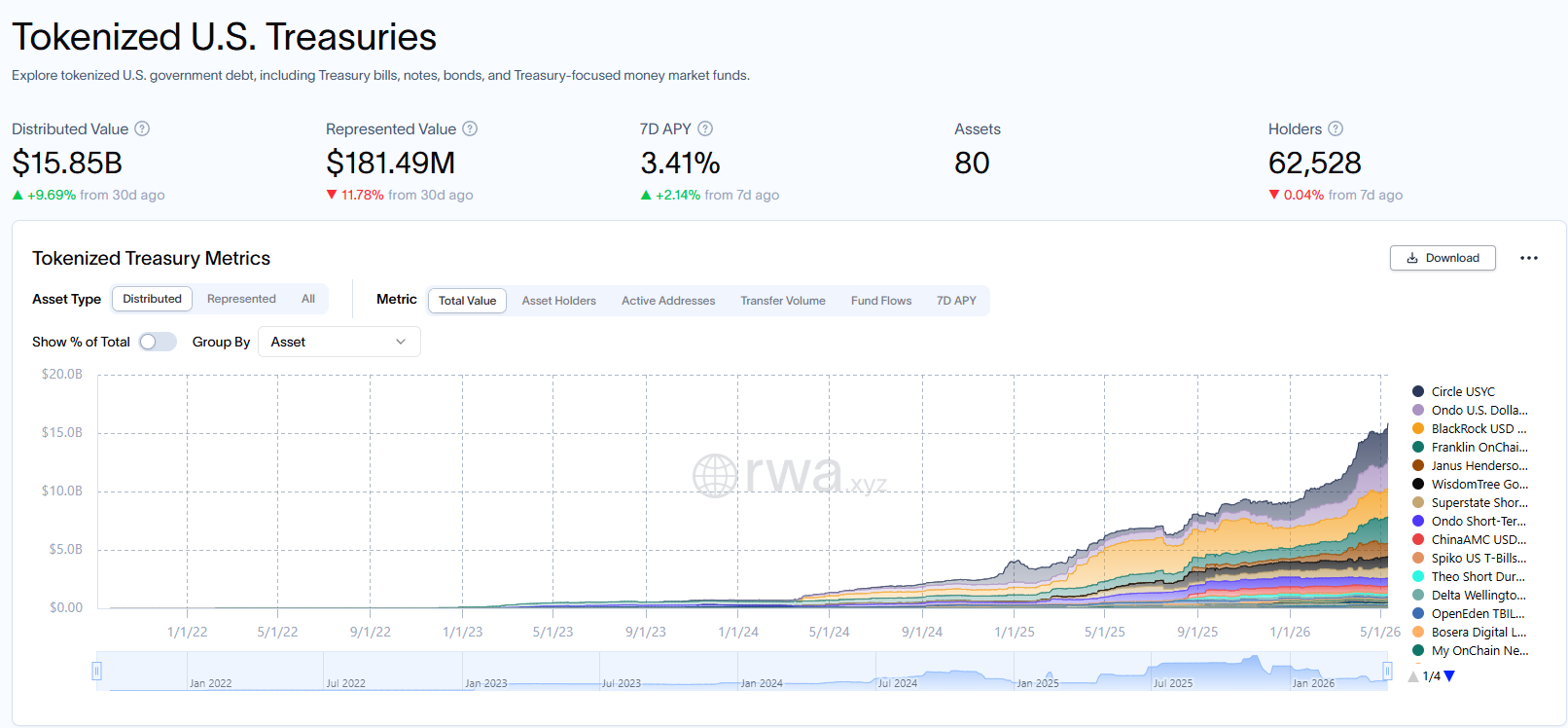

Market trends - U.S. Treasuries Still Dominate: According to market data from RWA.xyz, tokenized U.S. Treasuries remain the undisputed heavyweight of the ecosystem, commanding nearly $13 billion of on-chain value. BlackRock’s BUIDL fund alone accounts for roughly $1.7 billion in this segment. This week also saw several newly registered on-chain allocations from asset managers, including Benji (Franklin Templeton) and Fidelity International, for their digital liquidity products.

Deep Dive: BoE Pivots on Stablecoin Rules to Boost UK Competitiveness

The Top Line: The Bank of England (BoE) is preparing to water down its planned restrictions on sterling-denominated stablecoins following intense pressure from the digital assets industry.

The Details

This week, The Banker magazine reported that, in an interview with the Financial Times, BoE Deputy Governor Sarah Breeden admitted that the central bank’s initial proposals may have been “overly conservative” and confirmed that it is reviewing alternative approaches to managing risk.

This week, the BoE and the FCA also published a news release outlining a shared vision to accelerate and support the responsible adoption of tokenisation and distributed ledger technology (DLT) in UK wholesale financial markets. Key highlights from the announcement include:

- Joint Call for Input: The FCA and BoE have opened a joint call for input titled "The future of tokenisation".

- Infrastructure Upgrades & Central Bank Action: Near 24/7 Settlement: The BoE has initiated a consultation on extending the operating hours of CHAPS and Real-Time Gross Settlement (RTGS) toward a staged near 24/7 model (including weekends).

- Synchronisation Service: The Bank plans to launch a live synchronisation service targeted for 2028.

- Tokenised Collateral: The BoE is working to permit tokenised equivalents of already eligible assets to be utilised as collateral in both its central bank operations and at central counterparties. This will also align with HM Treasury's pilot of a digital gilt instrument (DIGIT).

- The Prudential Regulation Authority (PRA) issued "Dear CEO" letters providing updated expectations regarding risk management, compliance, the prudential treatment of tokenised assets, and innovations involving stablecoins, deposits, and e-money.

- Current Sandbox Projects: Regulators continue to actively collaborate with 16 firms executing live asset issuances and settlements in the Digital Securities Sandbox (DSS).

Digital asset providers have warmly welcomed the regulatory pivot. George Morris, digital assets partner at law firm Simmons & Simmons, warned that US dollar-backed giants like Tether ($USDT) and Circle’s $USDC currently command the vast majority of global liquidity. Industry experts argue that without a more flexible, proportionate framework, the UK risks falling further behind international jurisdictions like the US and the EU in the race to become a leading digital finance hub.

Worth Reading - Eurostablecoins anyone?

European macroeconomist Spyros Andreopoulos, in his regular Thin Ice Macroeconomics letter, digs into the case, for and against a European stablecoin.

With global geopolitics shifting, Europe is pushing hard for strategic autonomy, according to Andreopoulos. ECB President Christine Lagarde is championing the upcoming Digital Euro as the ultimate shield for monetary sovereignty. The issue, according to Andreopoulos, is that the Digital Euro comes with strict holding limits, potentially as low as €500, and corporate restrictions that completely kill its ability to act as a proper store of value or a fluid cross-border payment tool. Meanwhile, US dollar stablecoins are booming and could hit $2 trillion by 2028, threatening to trigger a wave of digital dollarisation that leaves the euro in the dust internationally.

Andreopoulos argues that Europe shouldn't fight private euro stablecoins; they are exactly what's needed to defend the euro’s global status. While Lagarde worries about financial stability and banks getting sidelined, these are mostly regulatory puzzles that can be solved with smart guardrails. Ultimately, it doesn’t have to be an all-or-nothing battle. A hybrid system in which the Digital Euro acts as a trusted anchor and private stablecoins drive international trade and innovation is the perfect recipe to keep Europe competitive.

"Ultimately, it’s not clear to me why Europe can’t have both public (the digital euro) and private digital money (stablecoins and tokenised deposits). When it comes to defending the international position of the euro, both have a role to play. US legislation has settled the question of public versus private digital money entirely in favour of private money by prohibiting central bank digital currency. The EU, by contrast, should create the technological and regulatory framework for a hybrid system."

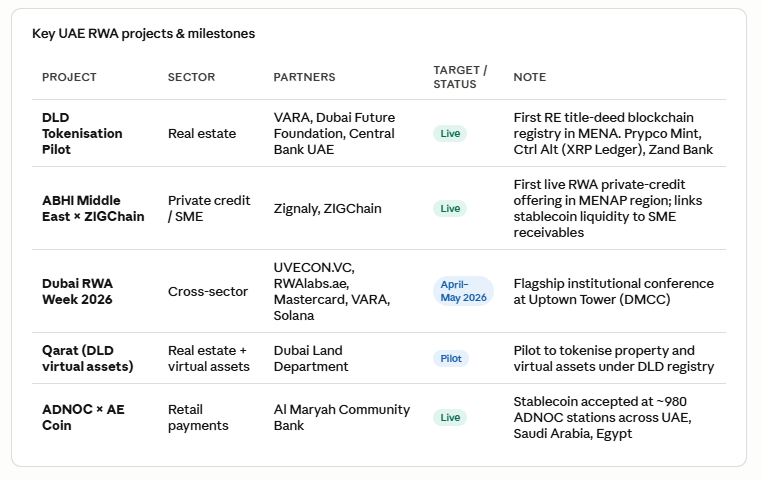

Real-world asset tokens and stablecoins in the Gulf

Looking at RWA tokens, globally, they grew to over $24 billion in total value by February 2026, with 266% growth over 2025. The UAE's role in that story centres on real estate. The Dubai Land Department projected that tokenised real estate could account for 7% of the city's total property transactions, reaching 60 billion dirhams ($16 billion) by 2033. The DLD's pilot is the first property registration authority in the Middle East to use blockchain for title deeds. Across the wider UAE market, the RWA tokenisation segment is projected to grow at a 32.5% CAGR through 2030, with real estate leading with a 42% sector share, followed by commodities at 25% and art and collectables at 15%.

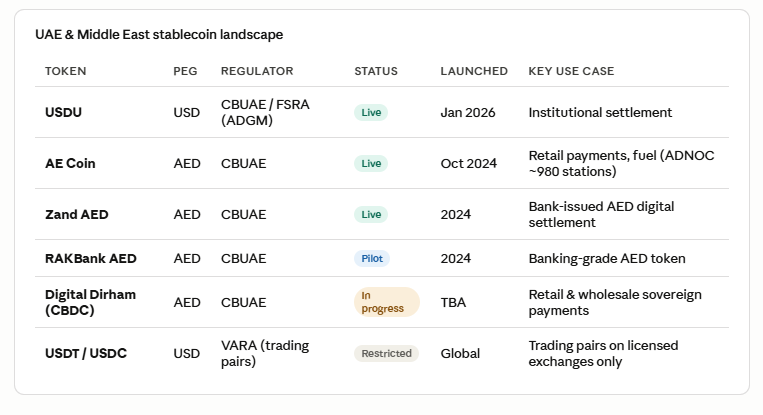

The stablecoin story in the UAE is arguably moving faster than anywhere else. The local USDU launched on January 29, 2026, as the UAE's first Foreign Payment Token registered by the CBUAE, backed 1:1 by reserves at Emirates NBD, Mashreq, and Mbank, with monthly independent attestations. On the AED side, AE Coin became the first fully licensed AED-pegged stablecoin in October 2024, and in December 2025, ADNOC Distribution signed a deal to accept AE Coin across nearly 980 service stations in the UAE, Saudi Arabia, and Egypt, which is one of the largest retail deployments of a regulated payment token anywhere in the world.

The regulatory architecture is what makes the UAE stand out. The CBUAE is now the sole regulator for Payment Token issuance, local retail payments are limited to dirham-backed tokens, and algorithmic and privacy-centric tokens are banned outright. VARA covers Dubai onshore, FSRA governs ADGM, and there's now a unified VASP register across both. It's not the loosest regime, but it's probably the clearest one.

BlackRock's $2.3bn UAE Experiment

By Anna Fedorova

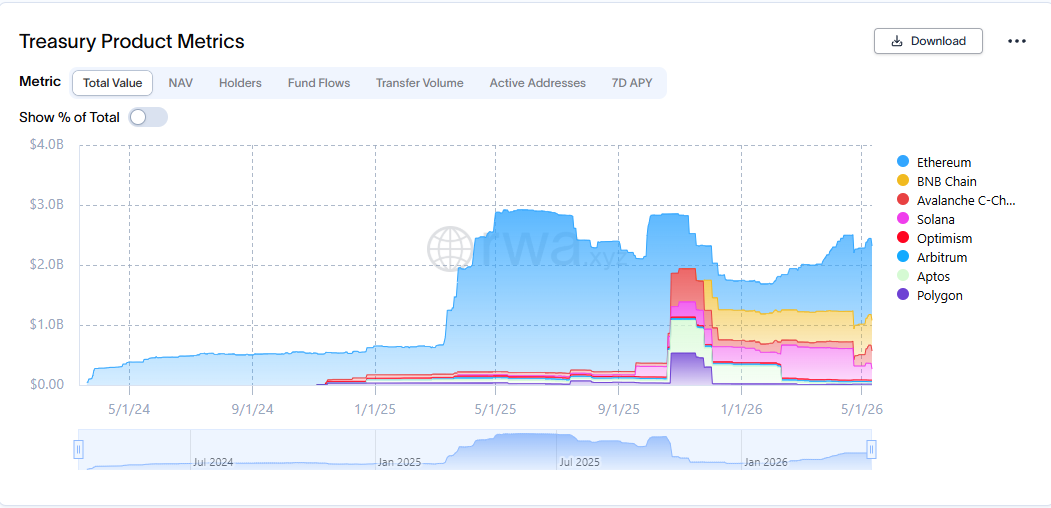

Recently, BlackRock made yet another move in its bid to dominate the decentralised finance (DeFi) space. Through a cutting-edge partnership with Standard Chartered and the major crypto exchange OKX, BlackRock has transformed its $2.3bn BlackRock USD Institutional Digital Liquidity (BUIDL) fund – a vehicle that allows investors to hold tokenised treasuries – into a productive asset.

For the first time in the history of decentralized finance (DeFi), professional investors are able to not only use the fund as collateral, but earn a yield on it at the same time. This solves a problem the DeFi space has grappled with for years, a roadblock for institutional investors. Before, stablecoins, other digital assets, and increasingly tokenised assets could be posted as collateral on crypto exchanges – but they would just sit idle until the position was closed. For institutions seeking ever-innovative ways to maximise returns on their capital, this was a missed opportunity. Who better than the world's biggest asset manager to change this? The current annual percentage yield (APY) on the BUIDL fund sits at 3.43%. That’s potentially an extra $34,400 a year for every $1 million worth of BUIDL shares held as collateral on OKX. There’s one catch, though: for now, this is only available to investors in the Middle East. This, in itself, is not a coincidence – more on that later.

BUIDL, in brief

So what exactly is the BlackRock USD Institutional Digital Liquidity fund? Launched in March 2024, BUIDL is BlackRock’s first tokenized money market fund. Investing 100% of its total assets in cash, US Treasury bills, and repurchase agreements, it allows institutional investors to earn yield while holding a token on the blockchain that represents their ownership. BUIDL seeks to offer a stable value of $1 per token and pays daily accrued dividends directly to investors' wallets as new tokens each month. In the two years since its launch, BUIDL has become a key building block in the DeFi ecosystem. Several stablecoins, including Ethena’s USDtb and Frax Finance’s frxUSD – both established names in the DeFi space – use BUIDL as collateral. It was also integrated with Circle in April 2024, allowing instant redemption into the USDC stablecoin – one of the two leaders in the market. And in February, it was integrated into Uniswap – one of the biggest decentralized exchanges. Now, all of these holders will be able to earn yield on their collateral.

In an interview with Cointelegraph following the latest news, Rifad Mahasneh, MENA and CIS CEO at OKX, explained that the user experience was designed to be as seamless as possible. Investors simply buy BUIDL directly on OKX and start earning yield while the asset is in custody with Standard Chartered – and simultaneously able to use this asset for trading purposes on the OKX platform.

On the OKX Learn blog, the exchange explains that “on-exchange, BUIDL can be deposited and used as yield-bearing collateral across trading activities on OKX. As yield continues to accrue, margin becomes productive and balance sheets become more efficient”. Yield on the product accrues daily, but is paid out monthly into the holder’s wallet in the form of new, so the collateral compounds.

So far, so simple. But what OKX and BlackRock have not publicly addressed yet is what happens to pending yield in the event of mid-month liquidation. BUIDL pays dividends monthly, not continuously, so a position closed out before the month-end rebase may forfeit any accrued but undistributed interest on the seized collateral. Neither company has published documentation clarifying whether that yield is rebated to the holder or simply absorbed.

The regulatory bet

Launching this product in the UAE is important strategically. For years, the UAE has arguably been more open to digital asset innovation than almost any other nation on Earth. But, crucially, this openness has been within a clear regulatory framework: music to the ears of any major institution. UAE established a dedicated digital assets regulator – the Virtual Assets Regulatory Authority (VARA) – in 2022, well before any other major nation was anywhere close to such a decisive move. In an interview with Cointelegraph, OKX’s Middle East CEO says this regulatory clarity has given the region an edge that “isn’t going away anytime soon” – one that has attracted complementary partners and supported the buildout of banking infrastructure to support blockchain-led innovations. He says: “UAE has done a great job in becoming a hub – it not only regulates but continues to innovate on this regulation.”

The choice makes sense for a product at the cutting edge of finance, but I suspect BlackRock would have rolled this out in New York if it could have. Perhaps the Western financial centres aren’t quite ready for this level of experimentation. Or, perhaps, BlackRock wants to use the UAE as a testing ground.

A look under the hood

But while on paper, the whole thing looks like an exact replica of how collateral works in the traditional financial world, it’s a bit more complicated than that in practice. Firstly, unlike listed US funds, BUIDL is not registered with the Securities and Exchange Commission (SEC) and not a Rule 2a-7 registered money market fund. As such, it doesn’t have to disclose granular details about its underlying holdings, and all that’s publicly reported is which assets are in the mix.

Secondly, and more importantly, like any other token on a blockchain, BUIDL trades 24/7, in contrast to the underlying assets it provides exposure to, whatever proportion they may be in. That creates a liquidity mismatch outside of normal market trading hours. Of course, this doesn’t mean investors will suddenly be locked out of their assets if they suddenly decide to redeem on the weekend – the sophisticated infrastructure behind the scenes means their redemption request would be processed instantly even if the underlying asset isn’t trading.

But it does introduce an additional layer of complexity. This could affect valuations if the market moves sharply and could theoretically lead to haircuts during times of market stress. OKX says BUIDL is treated as “fungible” with USD and USDC, so there’s no haircut applied to the valuation at the outset. OKX's general margin documentation, however, notes that every collateral asset is subject to a discount rate calibrated to its volatility and liquidity profile – so the precise number applied to BUIDL, and whether it differs in stressed market conditions, is opaque.

The ghost of 10/10

The financial system works until it doesn’t, and crypto infrastructure has a history of struggling when volumes spike too high. The best example of this is 10 October 2025 (referred to in the industry simply as 10/10), when at least $19 billion in leveraged crypto positions were wiped out in 24 hours, leaving market makers reeling for months. Aaron Rafferty, co-founder of WYDE – a non-profit that runs a crypto exchange that directs all fees toward charitable initiatives – warns that the rails BlackRock is building on have not yet been tested with BlackRock-scale flows. “Uniswap has done trillions in volume but has not held anywhere near a trillion in assets (neither has the whole of DeFi),” he notes, pointing out that even that would be merely a tenth of BlackRock’s AUM.

Referencing the 10/10 sell-off, he also notes that one of the problems was that Binance was treating Ethena's USDe as same-tier collateral with USDC. However, unlike USDC – which is one of the two most used stablecoins with a market cap of $77 billion – USDe’s market cap is less than $4 billion. On the fateful day, it flash crashed from $1 to somewhere around $0.65 on Binance due to liquidity issues, causing forced liquidations that exacerbated the market crash. “The failure point isn't the tokenized asset itself, but the venue treating it as interchangeable with cash,” says Rafferty.

OKX’s Mahasneh, however, says the BUIDL product was “designed to minimize risk rather than add layers of risk”. And that may well be true in practice. After all, run by the biggest asset manager in the world and custodied by one of the most established banks on the planet, BUIDL is a very different kettle of fish from a small decentralised stablecoin. But, as they say, to be forewarned is to be forearmed.

What to watch

So is this as revolutionary as headlines would have us believe? For institutional crypto holders, this is a big improvement. But thinking of the 3.43% APY as a free lunch would be a mistake. This is the reward investors receive for taking on the risk of holding a token that trades 24/7 but could, in theory, decouple from the underlying market it tracks. And as 10/10 showed, even a momentary flash crash could be catastrophic for the wider digital asset market.

As OKX investors in the UAE begin to use this new feature, the real sign that this is a big deal would be if BlackRock starts expanding this to other jurisdictions – and which ones approve it first. The hardest to crack markets – London and New York – will be the real vote of confidence.

In the US specifically, it’s worth watching whether BlackRock's new US-domiciled BSTBL and BRSRV – structured to qualify as eligible stablecoin reserve assets under the GENIUS Act – get the same productive-collateral treatment. If it does, usage could skyrocket, but it will only pass the stress test when it can match BlackRock’s multi-trillion-dollar volume without breaking.

Stablecoins: just how stable are they?

By Damien Black and David Stevenson

Continuing our explainer series, stablecoins: are they really the next big thing, or just the next big disaster waiting to happen?? Unsurprisingly, the regulators are showing interest!

Imagine, if you can, a disillusioned small-business owner in Argentina. They have a wonderful product which they sell internationally. They sell in dollars, but their central bank restricts access to hard currency. They’re desperate to work out a workaround which doesn’t involve hugely expensive wire transfers or dodgy currency brokers. Cue cryptocurrencies and especially stablecoins.

Stablecoin cross-border flows are accelerating. The IMF is concerned.

source: Cerutti, Chainalysis, Reuter 2025, IMF

Stablecoins are cryptocurrencies engineered to hold a fixed value — almost always $1 — rather than fluctuating like Bitcoin or Ethereum. The interesting question is how they maintain that peg, and there are actually three quite different mechanisms for doing it.

Fiat-backed (the simple version)

For every stablecoin in circulation, the issuer holds an equivalent amount of real dollars (or dollar-equivalent assets like Treasury bills) in a bank or custodian. It's essentially a digital IOU. You give Tether $1, they give you 1 UST and put your dollar in a reserve account. When you want your dollar back, you return the UST and they redeem it. The peg holds as long as people trust that the reserves are genuinely there — which is why the monthly attestations matter so much.

There are, of course, variations. DAI, for instance, is popular in Argentina and is a decentralised stablecoin pegged to the US dollar, issued by the MakerDAO protocol (now rebranded as Sky). Unlike USDC or USDT, there's no company holding dollars in a bank account behind it — it's generated entirely through smart contracts on the Ethereum blockchain.

Instead of dollars in a bank, it's backed by crypto assets locked in smart contracts on the blockchain. Because crypto is volatile, it's overcollateralised — you might need to lock up $150 worth of Ethereum to mint $100 of DAI. If the collateral falls too far in value, the system automatically liquidates it to protect the peg. There's no company holding reserves — it's all governed by code and the MakerDAO protocol.

More generally, with stablecoins such as Tether and USD Coin, you can effectively trade in dollars without actually owning dollars. Argentina leads Latin America in cryptocurrency value received, with an estimated $91.1 billion in 2024, and ranks 14th globally in the Chainalysis adoption index. Stablecoins such as USDT (Tether) and USDC dominate — on the exchange Bitso, USDT and USDC together accounted for 72% of all purchases. Suddenly, you can access an international currency clearing system by using coins backed up – collateralised – in hard currency. What’s not to like ?

Where Circle (USDC) puts its dollars at a glance. Could this add up to a liquidity problem in the event of a crisis?

source: CryptoRank, CoinLaw

What's not to like ? Alot as it happens, especially if you are a central bank, or an organisation that represents central banks. The IMF was pretty unequivocal in its recent criticisms. Yes, tokenisation has the benefit of speeding up transactions – the coveted T+0 model of instantaneous transfers – but it could also have the unwanted side effect of accelerating a crisis when things get out of control.

Which, as anyone who remembers 2007 will recall, they most certainly can do. The Fund argues that this malaise could easily spread to stablecoins. Increasingly used as settlement assets in transactions, they “may be vulnerable to run dynamics if confidence breaks down” leading it to conclude that “efficiency comes at the cost of resilience”. Goldman Sachs has joined its voice to the IMF in raising concerns, warning that if investors shift en masse from domestic banks to stablecoins, “central banks may lose control over monetary policy and capital flows”.

The IMF isn’t the only major fiscal institution to raise eyebrows at the seemingly headlong dash towards stablecoins and tokenization. The Bank for International Settlements (BIS) warned in June 2025 that stablecoins fail three key “sound money” tests – namely singleness, elasticity and integrity.

Let’s take a look at each of these in turn.

A return to Wild West banking?

The BIS describes the singleness of money as being a property that allows it to be “issued by different banks and accepted by all without hesitation”. “It does this because it is settled at par against a common safe asset (central bank reserves) provided by the central bank, which has a mandate to act in the public interest,” says the BIS. This underpins universal trust in money, allowing transactors to use it with “no questions asked”. However, stablecoins fare poorly on the singleness issue because as digital bearer instruments they lack the settlement function provided by the central bank. “Stablecoin holdings are tagged with the name of the issuer, much like private banknotes circulating in the 19th century Free Banking era in the United States,” the BIS explains. “As such, stablecoins often trade at varying exchange rates, undermining singleness.” This in turn means they are “unable to fulfil the no-questions-asked principle of bank-issued money”.

The importance of trust

Another key property of sound money is elasticity. Essentially this allows banks to issue money that they might not, strictly speaking, have on them at the time. This can cover lending activities such as extending overdrafts and other lines of credit, but the BIS notes it also can refer to “money being provided flexibly to meet the need for large-value payments in the economy, so that obligations are discharged in a timely way without gridlock taking over”. This makes sense. If every transaction had to be pre-funded, then said gridlock would occur in pretty short order, and the economy would become hopelessly snarled up. This ties in again with the key issue of trust, with central banks acting as guarantors of such workarounds to keep the wheels of the economy oiled and moving.

Stablecoins require money up front

“When needed, the central bank can provide intraday settlement liquidity so that transactions can be settled in real time,” says the BIS. “Banks, in turn, can decide how much money (in the form of deposits) they want to provide to the real economy.” Unfortunately, stablecoins aren’t capable of fulfilling this function, “because the issuer’s balance sheet cannot be expanded at will”. For a fiat-backed digital currency token to be issued, real currency has to be first expended – a dollar-denominated stablecoin simply can’t exist without a dollar behind it.

The BIS notes: “Any additional supply of stablecoins thus requires full up-front payment by its holders – a strict cash-in-advance set-up with no room to create leverage when it is required for the functioning of the system. This differs fundamentally from banks, which can elastically expand and contract their balance sheets within regulatory limits.”

The crook’s ‘go-to’ currency

Finally, there is the test of integrity, and because it touches on safeguarding money from illicit use it is perhaps the hottest potato in the basket. “This imperative flows from the recognition that a monetary system that is open to widespread abuse from fraud, financial crime and other illicit activities will not command trust from society or stand the test of time,” says the BIS. Unsurprisingly, the BIS has little good to say about stablecoins in this regard.

"The pseudonymity of public blockchains, where individual users’ identities are hidden behind addresses, can preserve privacy but also facilitates illegal use,” it says. “The absence of know-your-customer (KYC) standards like those of the traditional financial system exacerbates this issue. The bearer nature of stablecoins allows them to circulate without issuer oversight, raising concerns about their use for financial crime, such as money laundering and terrorism financing.” It even goes so far as to describe stablecoins as 'the go-to choice for illicit use to bypass integrity safeguards”

Stablecoins ‘unsound’

The BIS concludes “stablecoins do not stack up well against the three desirable characteristics of sound monetary arrangements and thus cannot be the mainstay of the future monetary system”. If global banking decides to go all-in on stablecoins while forgoing the “tried and tested foundations of trust” that underpin sound money principles, it runs the risk of relearning “the historical lessons about the limitations of unsound money, with real societal costs”. Nevertheless the BIS acknowledges the high demand for stablecoins despite these shortcomings, and hopes that robust policies will ensure legitimate use cases are appropriately regulated.

However, it adds: “Adequate regulation can only go so far in addressing some important structural flaws that are likely to persist, such as the limitations placed by cash-in-advance constraints.”

So why the headlong dash?

Such warnings, stark as they are, only serve to illustrate how much of a presence stablecoins have become in the financial landscape. “The most influential organisations are preparing for a major digital transformation,” says Michael Hunter, writing in the Intersection. “There are a variety of strategies in place and under development. Each involves stablecoin-style payments for the transactions at the wholesale level of finance – across borders and between central banks – taking the blockchain beyond retail-level transactions between individual users.”

The prospective benefits are not to be sneezed at. Faster and cheaper cross-border payments, an end to cumbersome paperwork and atomised regulatory oversight in each transacting country slowing down transactions. “A web of bilateral relations […] loaded with fees, making the system cumbersome and exposing it to geopolitical turbulence,” as Hunter puts it. Being blunt about it, the benefits that stablecoin-driven transactions offer are just too tempting for the warnings from the IMF and BIS to carry much weight. Human beings have a tendency to innovate first and ask questions later.

ECB’s cost-benefit analysis

The European Central Bank (ECB) says that stablecoins present potential risk and reward in equal measure. While expressing concerns that the phenomenon could erode European monetary sovereignty – noting in 2025 that 99% of stablecoin market capitalisation consisted of US dollar-backed currency tokens – the ECB also sees opportunity.

“Euro-based stablecoins, if designed to high standards and effective risk mitigation, could serve legitimate market needs,” says the ECB. “They could also reinforce the international role of the euro.” The ECB believes that the EU’s stable framework and rules-based approach could provide a solid foundation for the kind of trust that the BIS suggests is currently lacking elsewhere (read: the US). “If the Eurosystem and the European Union can build on this advantage – through robust regulation, infrastructure investment and digital currency innovation – the euro could emerge from this period of change as a stronger currency,” it concludes.

Staying safe has its perils too

On the other hand, if the eurozone remains cautious and stays out of the game, allowing the US to shore up its dollarized stablecoin hegemony, the ECB worries it could lose control of monetary policy. “Should US dollar stablecoins become widely used in the euro area – whether for payments, savings or settlement – the ECB’s control over monetary conditions could be weakened,” says the ECB. “This encroachment, though gradual, could echo patterns observed in dollarised economies, especially if users seek perceived safety or yield advantages that are not available in euro-denominated instruments.”

So far the ECB seems to be making good on its pledge to keep abreast of the stablecoin boom. Earlier this year, the Intersection reported that it had launched “twin initiatives” – Pontes and Appia – on the tokenisation of international payments. “The ECB says it will head toward an innovative and integrated payments and securities ecosystem in Europe that also facilitates safe and efficient operations at the global level,” writes Hunter.

But there’s one last issue to contend with – because they can’t issue credit, stablecoins are not subject to Basel III. Bear in mind that this regulation was created after the 2008 crisis to ensure banks had sufficient capital buffers to survive a debtor's default on a loan. If you remember that turbulent period of financial history with a shudder, this is a crucial detail you cannot afford to ignore.

Sure, stablecoins might not carry credit risk, but they do present liquidity risk – 100% dollar backing does not necessarily mean the issuer has all the ‘real’ dollars sitting in its account at any given time. This is because stablecoin issuers like Circle and Tether tend to invest the dollars you’ve given them in things like short-term US Treasury bonds to turn a profit. Stablecoins failed the elasticity test. So what happens if there’s a run and everyone asks for their fiat dollars back at once?

Events on our radar

DigiAssets Connect Zurich, 16-17 June - Custody, banking, and institutional infrastructure – tickets HERE

European Blockchain Convention 12, Europe’s Deal Floor for Digital Assets. BARCELONA · 16-17 SEPTEMBER 2026 - tickets HERE