By Damien Black

The shift towards tokenisation is viewed as “inevitable” in the US financial sector, with smaller banks more likely to lose out than bigger players, warns ratings agency Moody's.

You know a tech-driven phenomenon is making waves when a credit-ratings agency founded more than a century ago publishes three reports in a row on it. That’s what Moodys did on May 11-13, and its opinions will be greeted gleefully by fintechs and asset managers, fingered as the “clearest likely beneficiaries” of tokenisation. On the other hand, small- to medium-sized banks and legacy money transfer and post-trade operators are classified by the agency as among the “most exposed categories”.

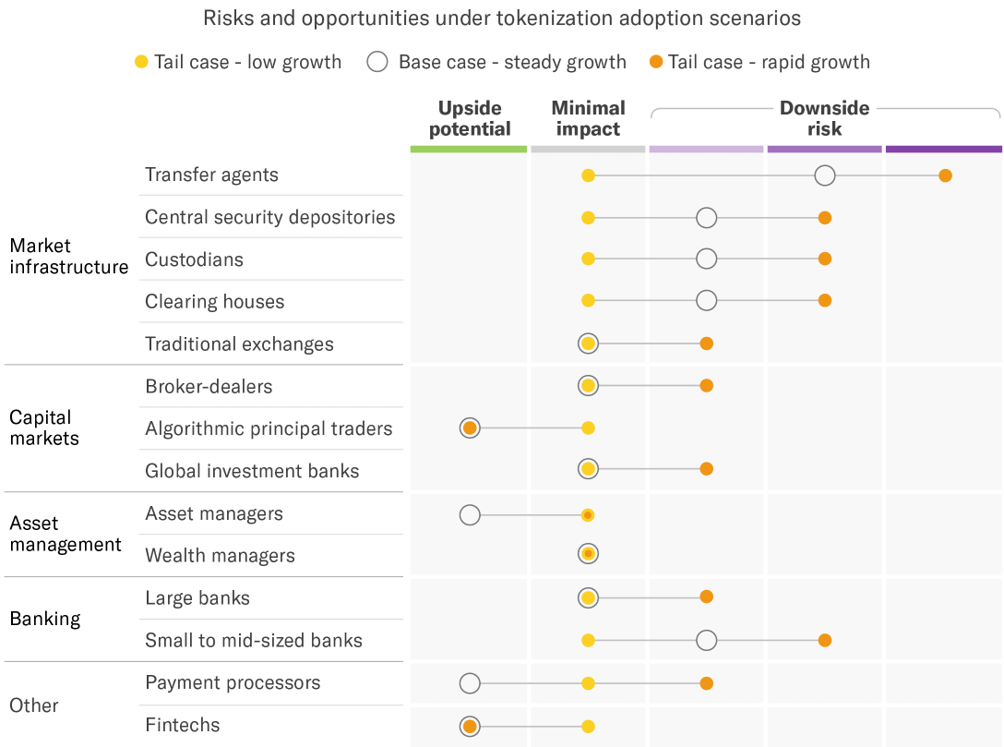

Graphic: Transfer agents, security depositories, custodians, clearing houses and small-to-medium sized banks bear the brunt of tokenization risk, says Moodys

Smaller banks could lose out

“US financial markets envision an inevitable shift to tokenized assets and digital money,” said Moodys in one of three reports shared with the Intersection. It added: “Conversations with major US banks and financial market intermediaries [...] reveal a forming consensus that there will be a ‘slow, then fast’ transition to a more digitalised financial system in which tokenisation increases in volume.”

Moodys believes firms will initially run “hybrid models” that blend traditional and tokenized transactions, extend trading hours, and shorten settlement cycles – the coveted T+0 model. This will be done “without yet achieving fully real-time markets or completely tokenized asset life cycles”. “However, the overall hierarchy of the financial system will largely stay the same despite changes in operating models across certain subsectors,” said Moodys.

Transfer agents, central securities depositories, custodians, clearing houses and exchanges will likely continue to play a central role in the evolving financial market. So no one’s out of a job just yet – although Moody's warns that those jobs “could gradually shift toward risk management, exception management and compliance”. However, those working at smaller banks could soon find themselves in choppy waters.

“If the velocity of money increases, banking system deposit balances could decline and prove less sticky,” said Moody's. “Banks that lack the resources to provide competitive digital asset services as demand increases risk losing client relevance in an expanding market.” Likewise, legacy transfer service operators that worked on in-house systems and manual processing could struggle, as tokenization renders them increasingly obsolete. So what about the big boys?

Well, Moody's sees a more mixed picture for global systemically important banks (G-SIBs) such as Citigroup, State Street, and Bank of America. Bigger banks will benefit from vast resources that enable them “to combine issuance, custody, settlement, liquidity and compliant on/off ramps into a single, trusted, regulated platform that is familiar to institutional investors”. In other words, if there is a stablecoin storm coming, bigger financial institutions will be better equipped to weather it – if Moody’s predictions are anything to go by.

Stablecoins growing but still small

Moodys notes that stablecoin growth has been “rapid but uneven”. Overall, these have ballooned from around a $5 billion market cap value in 2019 to topping $300 billion this year. This largely reflects the performance of the dominant form of stablecoin – the fiat-backed version of the digital currency. “These stablecoins typically hold reserves in low-risk assets, such as cash or short-term government securities, and account for the vast majority of total circulating supply,” said Moodys. If fiat-backed stablecoins are the heart of the currency, dollar-pegged ones are its soul. Moodys notes that, as things stand, 99% of fiat stablecoins are wedded to the greenback. Hardly surprising when you consider the GENIUS Act of 2025, designed, you might say, to make dollar-pegged stablecoins feel right at home in America.

That said, dollar stablecoins had to weather some lousy storms to get here. The collapse of TerraUSD in 2022 sent shockwaves through the digital market, as did Circle’s woes the following year when regional banking stress caused its flagship USD Coin (USDC) to trade below its signature $1 value. But before we get too carried away, Moodys reminds us that stablecoins are still just a school of fish in a very big sea. They remain “a small share of transactions”, and comprise just 1% of total US treasuries – although at $30 trillion, that’s not to be sniffed at. Indeed, stablecoins already make up one-twentieth ($6.5 trillion) of US T-bills, the go-to asset class for issuers' reserves.

Stablecoins carry ‘tech risks’

Unfortunately, stablecoins remain far from risk-free. On the surface, they might seem familiar, offering the same as banks and money market funds, only with shinier technology to enable faster transactions. But take a look under the hood, Moody's cautions, and a different picture begins to emerge.

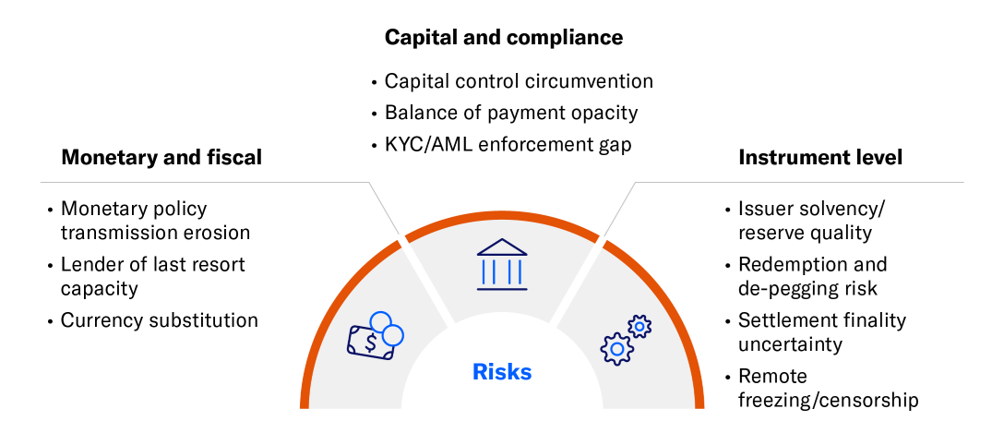

Graphic: Stablecoin holders are exposed to operational and technological risks, says Moodys

“Most stablecoins operate on public, permissionless blockchains, settle peer-to-peer between pseudonymous wallets, are typically not directly redeemable by issuers to retail holders, and circulate freely across borders outside the regulatory boundaries that govern comparable instruments,” it said. “These structural features shape how risks could emerge and spread.”

The most obvious threat to an investor’s wallet comes from the asset backing a stablecoin, in the form of credit risk – that an issuer of a security defaults – and market risk, that an asset loses value before it can be sold to meet redemptions. “Both risks diminish when reserves sit in cash and very short-dated government paper,” said Moody's, “and increase as issuers move into longer-dated debt or lower-quality assets such as commercial paper or obligations with low credit quality.”

But stablecoins also come with their own baked-in concerns, what Moodys calls “technology risk” – namely, a reliance on blockchain and digital smart contracts to keep on top of things like asset ownership and transfers. “Coding errors, network congestion, validator failures or cyberattacks can all disrupt timely settlement,” said Moody's.

Liquidity risk is also a factor. If an issuer is unable to convert assets to cash quickly enough to honour redemption requests on demand, they could find themselves out of pocket. “If reserves include securities with maturities longer than the redemption obligation, or assets that lack a deep and liquid secondary market, the issuer may face delays or losses in liquidating them,” said Moody's.

Tokenized deposits ‘natural evolution’

Perhaps this prevailing mood of caution explains why tokenized money and financial assets, while very much “live” in the US, remain “narrowly used”. However, if there is a wind of change about to blow here, Moody's predicts it will be driven by tokenised deposits, which it says banks view as a “natural evolution” even as they remain wary of stablecoins. “Because most consumers and corporations have shown little interest to date in tokenised money, many market participants do not believe payments alone will drive greater adoption of digital money,” said Moody's.

By contrast, it believes demand will grow if tokenized financial assets take off, requiring on-chain settlement to enable T+0 transactions that are instantaneous. But until that shift occurs, stablecoins will remain largely the preserve of those engaged in cryptocurrency trading and – to a lesser extent – cross-border retail transactions. “Banks view tokenised deposits as a natural evolution, in step with an eventual increase in tokenisation of real-world assets, but generally eye stablecoins warily,” said Moody's.

Indeed, banks appear to view tokenized deposits as a safer bet than stablecoins, with many choosing to favour their own in-house issuances so they can get into the game without abandoning familiar territory. “The strategy of most banks is to prioritize their own bank-issued tokenized deposits within the regulated banking sphere, while staying ready for stablecoins,” said Moodys.

It adds that tokenised deposits are also more attractive to stablecoins because they “leverage the existing interbank clearing and central bank settlement framework”. Essentially, established financial institutions don’t like the idea of non-bank actors like fintechs crowding the space and sidestepping the tried-and-tested guardrails. “Many banks view privately issued stablecoins as a potential threat that could allow non-banks or tech firms to bypass incumbent banks in payments and other services and potentially operate under different compliance, regulatory and legal frameworks depending on the applicable regime,” said Moodys.

Emerging markets beware...

Stablecoin risks become compounded in emerging markets. Digital dollar uptake might be good for the US – but it’s not necessarily good for other jurisdictions. This could well be precisely what the US wants of course, with Moodys noting that growing uptake of dollarized stablecoins “could extend the reach of the dollar into economies where it is not the official currency”.

“The risks above apply to any stablecoin holder, but their consequences fall unevenly across jurisdictions,” it said. “A majority of stablecoin holdings sit outside the US, with emerging markets accounting for the bulk of those non-US holdings.” Though it says hard data by region is difficult to come by, Moodys believes that dollar stablecoins are largely held in these jurisdictions alongside local currencies.

“The most consequential risk is the erosion of monetary sovereignty,” it said. “A central bank steers the economy primarily by changing policy rates, which affect the rates banks charge on local-currency loans and pay on local-currency deposits. If domestic users hold their savings, set prices and settle transactions in dollar-pegged stablecoins instead of local currency, this transmission mechanism weakens.” Rising uptake of dollar-stablecoins could also lead to greater fiscal opacity in such regions. “Cross-border flows of value that bypass the domestic banking system are harder to capture in the balance of payments,” said Moody's. “So when a domestic firm pays an offshore supplier with a stablecoin, the transaction may not appear in the current account, leading to understated deficits and obscured capital outflows.”

Furthermore, dollarized stablecoins could weaken fiscal revenues by facilitating tax evasion. “Tax authorities would face greater difficulty observing transactions that settle on blockchains rather than on regulated payment rails, opening new avenues for evasion,” said Moody's.

Triple As for Fidelity’s token fund

The concerns noted across its three reports didn’t stop Moody's issuing another bulletin on May 13, announcing it had awarded the coveted “Triple A” rating to Fidelity International’s tokenised liquidity fund. “The assignment of the Aaa-mf assessment reflects our view that the fund will have a very strong ability to meet its objectives of capital preservation and high liquidity,” Moody's announced.

It stresses that Fidelity would hold “a significant portion” of its assets in readily transferable “overnight” deposits. “As a result, we anticipate the fund will have very low exposure to market risk,” added Moody's. “We expect that modest shareholder concentration risk [...] will diminish as the fund grows in size and its shareholder base diversifies.”

As Moody's notes, “the stablecoin market is not monolithic – it spans several different instruments with different risks”. Tokenization might be a new game, but it will have its winners and losers just like the old game. And, right now, it seems the winners look more likely to be found among big banks and developed countries.