Welcome to the weekly letter from TheIntersection team. Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: Money market funds emerge as the first true winner of tokenisation

- Data: Calastone surveys asset manager token adoption

- Analysis: Equity exposure to the DeFi ecosystem

- Analysis: Moody's Sounds the alert

- Our weekly events round-up

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

News in Brief

JPMorgan moves tokenised money market fund onto public blockchain rails. JPMorgan Chase filed to launch the JPMorgan OnChain Liquidity-Token Money Market Fund (JLTXX), with fund shares designed to reside in public digital wallets rather than solely within the bank’s private Kinexys infrastructure. Why it matters: The move signals a major shift by Wall Street’s largest bank toward public blockchain-based financial infrastructure, reinforcing growing institutional confidence in permissionless networks for regulated financial products.

BlackRock, OKX and Standard Chartered integrate tokenised collateral workflows. OKX launched a joint framework with BlackRock and Standard Chartered that incorporates BlackRock’s BUIDL token into institutional collateral management processes, with Standard Chartered acting as custodian. Why it matters: The arrangement marks one of the first instances of a Globally Systemically Important Bank (G-SIB) supporting tokenised collateral workflows, advancing the integration of blockchain-based assets into mainstream financial operations.

US lawmakers accelerate focus on tokenised securities regulation

The U.S. House Financial Services Committee held dedicated hearings on tokenisation, with bipartisan agreement emerging that existing securities regulations are not well-suited to tokenised assets and require modernisation. Why it matters: Policymakers increasingly view regulatory reform as necessary to prevent tokenised bond issuance and other digital asset activity from migrating overseas, particularly as firms compete for a potential multi-trillion-dollar tokenisation opportunity.

Deep Dive — Money market funds emerge as the first true winner of tokenisation

The Top Line

Money market funds (MMFs) are becoming the dominant entry point for institutional tokenisation. A Calastone-led industry survey cited by FintechNews SG shows that tokenised MMFs are already viewed as the most practical near-term use case, combining traditional cash-management utility with blockchain-native settlement and stablecoin integration.

Unlike more complex asset classes such as equities or real estate, MMFs already behave like “digital cash” inside institutional portfolios. They are liquid, low-risk, yield-bearing instruments used by asset managers, corporates, and trading desks as short-term cash equivalents. By issuing MMFs as tokenised instruments on blockchain networks, asset managers can enable:

- Wallet-based fund ownership instead of legacy account structures

- Near-instant settlement and transfer of fund shares

- 24/7 liquidity outside traditional banking hours

- Direct subscription and redemption using stablecoins

- Improved transparency of holdings and flows

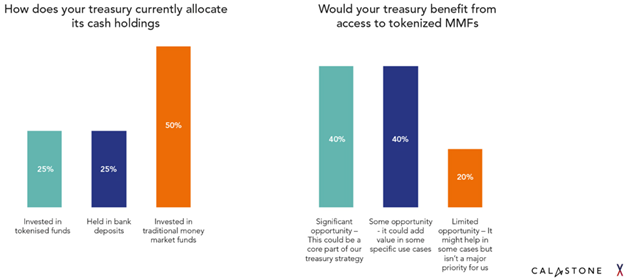

According to the Calastone survey, 80% of DeFi platforms believe tokenised MMFs improve treasury management, while 75% say they are critical for client retention. This reflects a structural gap in digital asset markets: while stablecoins provide transactional liquidity, they do not generate yield. Tokenised MMFs fill that gap by acting as a yield-bearing reserve asset that can still operate within blockchain-based workflows.

Bernstein on token market trends plus Calastone on fund manager adoption

Looking at the market in aggregate investment bank Bernstein estimates the tokenised RWA market at about 51 billion USD, up roughly 42% year‑to‑date. Within the broader market, tokenised private credit is currently the largest category, accounting for roughly 44% of total tokenised RWA value, i.e., yield plays. But money market funds are also having traction - Circle’s USYC tokenised Treasury product has surged past $3 billion in Assets Under Management (AUM), overtaking BlackRock’s fund BUIDL fund, which reached $2.5 billion in asset value. The BlackRock fund has expanded its distribution across a multi-chain footprint (including Ethereum, Solana, Polygon, Avalanche, Arbitrum, Optimism, Aptos, and BNB Chain). Franklin Templeton’s BENJI token (FOBXX fund) held steady right behind them at $2.47 billion in AUM.

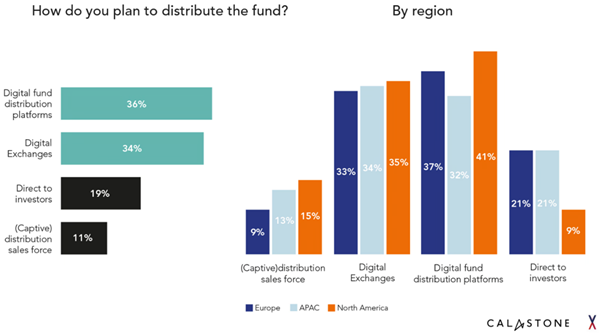

Fund platform business Calastone, in a recent report, projects that Tokenised fund AUM will reach $235bn by 2029, up from $4bn in 2024. Other aggressive forecasts (like PwC) target up to $715 billion by 2030. In terms of asset classes, money market funds and private assets are the leading use cases for tokenisation.

The survey also reveals that 80% of DeFi platforms believe tokenised MMFs could improve treasury management, with APAC firms leading the way. The study argues that globally, nearly three-quarters (73%) of global asset managers have now initiated at least one tokenisation project. The proportion of asset managers actively distributing tokenised funds is projected to more than double from 13% to 28% by 2030. For decentralised finance (DeFi) players, tokenised MMFs are viewed as beneficial for treasury management, with eight out of ten platforms surveyed by Calastone endorsing their utility, and three-quarters considering them critical for client retention.

The main hurdle? Interoperability remains the biggest regional headache. In Asia-Pacific (APAC), 57% of asset managers view cross-chain connectivity as a primary bottleneck, compared to just 28% in Europe and North America. Source

How to build equity exposure to the DeFi ecosystem

by John Gray

These stocks offer indirect exposure to DeFi’s growth, giving retail investors a chance to buy into its potential.

Investing in crypto is easy. You can buy it directly. You can buy an ETF that tracks it. Or you can buy shares in a company that has positioned itself as a ‘digital asset treasury’ (DAT). DeFi is less straightforward. As the name suggests, stablecoins do not accrue value, and you can only earn yield on them if you deploy them into financial activity, such as lending or DeFi protocols. This is a complex exercise — more complex, at least, than simply holding bitcoin [BTC] until the next price spike — and consequently most such activity is carried out by specialised firms.

In light of this, the question becomes: as a canny investor convinced that DeFi is the next big thing, how do you make money out of it? Counterintuitive as it may seem, the answer is: by buying equities. As the DeFi sector grows, the share prices of companies that facilitate on-chain financial activity should increase in value, helping investors derive some TradFi upside from the DeFi revolution. That, at least, is the idea. It can be useful to think of the DeFi ecosystem in terms of a four-layer stack. We’ll look at each in layer turn, as well as a company that offers exposure to it.

Layer 1: Settlement and money

This layer underpins the entire crypto financial system. It consists of assets used primarily for transferring value, storing liquidity and acting as collateral across networks, rather than for speculative appreciation. Stablecoins function as digital cash equivalents, while reserve assets such as BTC form part of the broader monetary base supporting on-chain activity.

The most prominent company in this layer is Circle [CRCL], which went public in a high-profile IPO in June 2025. It is best known for issuing USDC, a leading dollar–backed stablecoin, and building the core infrastructure for digital dollar payments and on-chain settlement.

The firm reported its Q1 results on 11 May.

USDC circulation stood at around $77bn, up 28% year-on-year and broadly flat quarter-on-quarter, despite a 45% decline in broader digital asset markets since October 2025. Within that, $13.7bn is held on Circle’s own platform infrastructure. On-chain transaction volumes surged to $21.5trn, a 263% increase year-on-year, with some third-party estimates placing total activity closer to $30trn when including Solana-linked [SOL] flows.

In terms of market position, according to Visa USDC now accounts for around 63% of stablecoin transaction volume, and roughly 80% of on-chain dollar-denominated digital currency transactions. These figures position Circle at the heart of this layer of the DeFi stack. On the call, CEO Jeremy Allaire spoke interestingly on the convergence of AI and DeFi, which he said would be “the largest platform shift in the history of the Internet”.

Layer 2: Access and distribution

Layer 2 acts as the gateway between traditional capital markets and on-chain financial systems. It includes platforms that onboard users, route liquidity, and provide entry points into crypto and DeFi. Rather than generating DeFi economics directly, these firms monetise flow, capturing fees as capital moves into and out of decentralised markets. Within this layer, Coinbase [COIN] stands out.

One of the dominant crypto exchanges in the US, it operates as a regulated on-ramp into digital assets, offering trading, custody, staking, and institutional infrastructure across both retail and professional markets. Over time, it has evolved from a pure exchange into a broader crypto financial platform, increasingly embedded in the distribution layer of on-chain markets and DeFi activity.

Coinbase reported Q1 earnings on May 7.

On the surface, the numbers weren’t great. The firm logged a net loss of $394.1m while revenue of $1.41bn was down 31% year-over-year. Both transaction revenue and subscription and services revenue missed analyst expectations, the latter falling 14% to $584m — an uncomfortable sign for a business that has spent years arguing its non-trading revenues would provide a buffer against crypto’s notorious cyclicality.

Underneath that, however, something more interesting was happening. Coinbase's global crypto trading market share hit a record 8.6% in the quarter — up from 2.7% just two years ago — even as total industry volumes fell sharply during the recent crypto downturn. The derivatives business grew 169% year-over-year. The exchange is winning market share precisely when the market is most brutal, which is indicative of either competitive strength or weaker rivals exiting the field (or, most likely, both).

Layer 3: Market structure

The closest thing crypto has to Wall Street, layer 3 provides liquidity, trading, financing and institutional intermediation across crypto and on-chain financial markets. It lies between end-user access platforms and underlying protocols. Rather than building or distributing DeFi directly, firms in this layer monetise volatility and flows across the entire digital asset ecosystem. A major player in this layer is Galaxy Digital [GLXY]. It positions itself as a diversified digital-asset financial services firm, operating across trading, asset management, investment banking, and principal investing. This gives it broad exposure to liquidity provision and institutional capital flows across the crypto ecosystem.

It logged a net loss of $216m, yet more fallout of the crypto winter, though analysts expected it to be worse. Again, despite the loss, Galaxy’s operating segments held up better than the headline figure suggests, while digital asset trading volumes remained flat quarter over quarter. Several other developments were worth noting. Following quarter-end, Galaxy Digital was selected by BlackRock as an approved validator to support staking for the iShares Staked Ethereum Trust ETF, which is BlackRock’s first crypto ETP designed to generate rewards.

Analysts also flagged Galaxy Digital’s pivot into data centre infrastructure as an exciting strategic shift from pure crypto markets. In the quarter, Galaxy delivered the first data hall at its Helios data centre campus to AI/cloud company CoreWeave [CRWV], marking the transition from construction into revenue-generating operations. The company is targeting delivery of most of the 133MW of critical IT capacity by the end of Q2 2026.

Layer 4: Programmable reserve strategies

Layer 4 consists of companies building large treasury positions in programmable digital assets such as ETH and SOL. On the surface, these firms could appear to be a subset of DATs. However, assets like ETH and SOL are not simply held passively; they can be actively deployed to perform core DeFi functions.

DeFi Development Corp [DFDV] is a good example of this. It concentrates its treasury in SOL and deploys it into staking, validator operations and on-chain yield strategies. This links shareholder value not just to SOL price movements, but also to network activity and DeFi-linked income streams within the SOL ecosystem.

DeFi Development Corp reported Q1 earnings on May 13.

In his letter accompanying the earnings report, CEO Joseph Onorati was careful to differentiate DFDV’s approach from that of Strategy [MSTR], the godfather of DATs, highlighting that “Solana’s ecosystem offers tools unavailable to a Bitcoin treasury company”, and that the company essentially comprised a portfolio of SOL-centred asymmetric bets. In terms of the numbers, the firm reported revenue of $4.49m, ahead of analyst expectations of $3.5m. However, it posted a significantly wider-than-expected GAAP loss, related to the fact SOL fell more than 30% during the quarter.

Despite the volatility, the company continued increasing its core treasury metric — SOL per share (SPS) — which rose 108% year-on-year. Total SOL holdings reached roughly 2.3 million tokens, placing DFDV among the largest publicly traded Solana treasury companies. DFDV reaffirmed its target of 0.075 SPS by June 2026, implying roughly 12% growth from current levels, while maintaining its longer-term goal of reaching 1.0 SPS by the end of 2028. Management also forecast improving quarterly performance, guiding to a near-break-even Q2 2026 result and targeting profitability by Q4 2026.

Bottom line?

DeFi exposure in public markets is indirect and fragmented, expressed through stablecoin infrastructure, exchange-based distribution, market intermediaries and programmable asset treasuries. Investors are effectively buying into the financial plumbing of on-chain systems.

This is, of course, an indirect substitute for true DeFi participation. With significant exposure to broader crypto cycles and execution risk, outcomes will depend as much on market structure and competition as on DeFi adoption itself.

Still, ‘true’ participation in DeFi’s economic activity remains the preserve of specialised companies. For most retail investors, buying shares in such companies is the best way to get a stake in the sector’s expansion.

Moodys sounds tokens alert

By Damien Black

The shift towards tokenisation is viewed as “inevitable” in the US financial sector, with smaller banks more likely to lose out than bigger players, warns ratings agency Moody's.

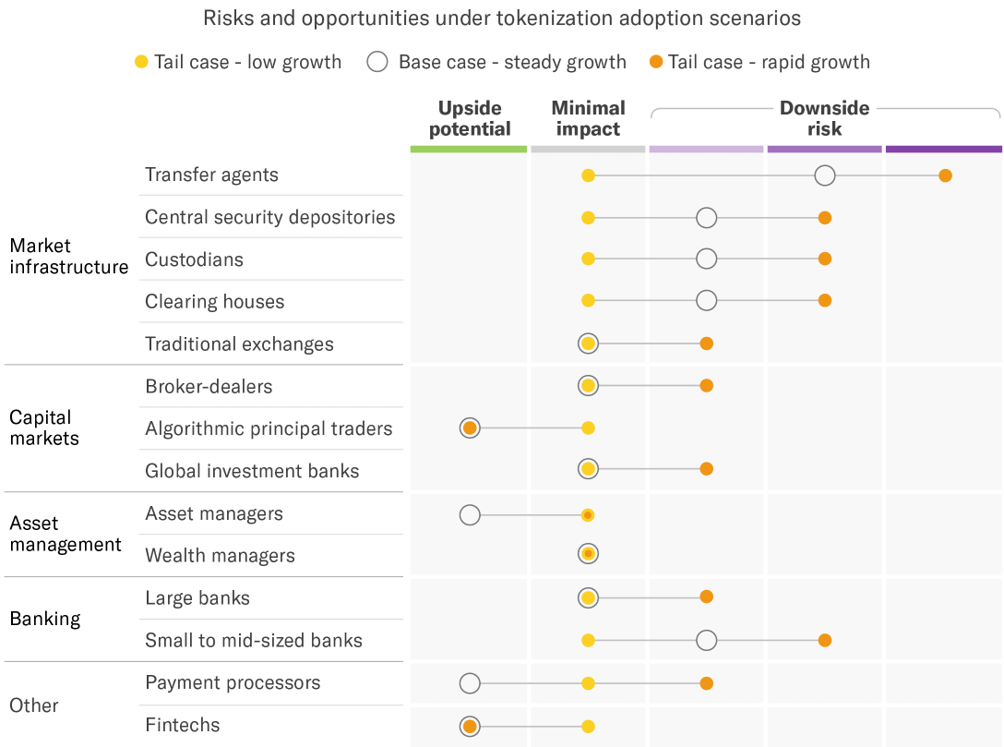

You know a tech-driven phenomenon is making waves when a credit ratings agency founded more than a century ago publishes three reports in a row about it. That’s what Moodys did on May 11-13, and its opinions will be greeted gleefully by fintechs and asset managers, fingered as the “clearest likely beneficiaries” of tokenization. On the other hand, small- to medium-sized banks and legacy money transfer and post-trade operators are classified by the agency as among the “most exposed categories”.

Graphic: Transfer agents, security depositories, custodians, clearing houses and small-to-medium sized banks bear the brunt of tokenization risk, says Moodys

Smaller banks could lose out

“US financial markets envision an inevitable shift to tokenized assets and digital money,” said Moodys in one of three reports shared with the Intersection. It added: “Conversations with major US banks and financial market intermediaries [...] reveal a forming consensus that there will be a ‘slow, then fast’ transition to a more digitalised financial system in which tokenisation increases in volume.”

Moodys believes firms will initially run “hybrid models” that blend traditional and tokenized transactions, extend trading hours, and shorten settlement cycles – the coveted T+0 model. This will be done “without yet achieving fully real-time markets or completely tokenized asset life cycles”. “However, the overall hierarchy of the financial system will largely stay the same despite changes in operating models across certain subsectors,” said Moodys.

Transfer agents, central securities depositories, custodians, clearing houses and exchanges will likely continue to play a central role in the evolving financial market. So no one’s out of a job just yet – although Moody's warns that those jobs “could gradually shift toward risk management, exception management and compliance”. However, those working at smaller banks could soon find themselves in choppy waters.

“If the velocity of money increases, banking system deposit balances could decline and prove less sticky,” said Moody's. “Banks that lack the resources to provide competitive digital asset services as demand increases risk losing client relevance in an expanding market.” Likewise, legacy transfer service operators that worked on in-house systems and manual processing could struggle, as tokenization renders them increasingly obsolete. So what about the big boys?

Well, Moody's sees a more mixed picture for global systemically important banks (G-SIBs) such as Citigroup, State Street, and Bank of America. Bigger banks will benefit from vast resources that enable them “to combine issuance, custody, settlement, liquidity and compliant on/off ramps into a single, trusted, regulated platform that is familiar to institutional investors”. In other words, if there is a stablecoin storm coming, bigger financial institutions will be better equipped to weather it – if Moody’s predictions are anything to go by.

Stablecoins growing but still small

Moodys notes that stablecoin growth has been “rapid but uneven”. Overall, these have ballooned from around a $5 billion market cap value in 2019 to topping $300 billion this year. This largely reflects the performance of the dominant form of stablecoin – the fiat-backed version of the digital currency. “These stablecoins typically hold reserves in low-risk assets, such as cash or short-term government securities, and account for the vast majority of total circulating supply,” said Moodys. If fiat-backed stablecoins are the heart of the currency, dollar-pegged ones are its soul. Moodys notes that, as things stand, 99% of fiat stablecoins are wedded to the greenback. Hardly surprising when you consider the GENIUS Act of 2025, designed, you might say, to make dollar-pegged stablecoins feel right at home in America.

That said, dollar stablecoins had to weather some lousy storms to get here. The collapse of TerraUSD in 2022 sent shockwaves through the digital market, as did Circle’s woes the following year when regional banking stress caused its flagship USD Coin (USDC) to trade below its signature $1 value. But before we get too carried away, Moodys reminds us that stablecoins are still just a school of fish in a very big sea. They remain “a small share of transactions”, and comprise just 1% of total US treasuries – although at $30 trillion, that’s not to be sniffed at. Indeed, stablecoins already make up one-twentieth ($6.5 trillion) of US T-bills, the go-to asset class for issuers' reserves.

Stablecoins carry ‘tech risks’

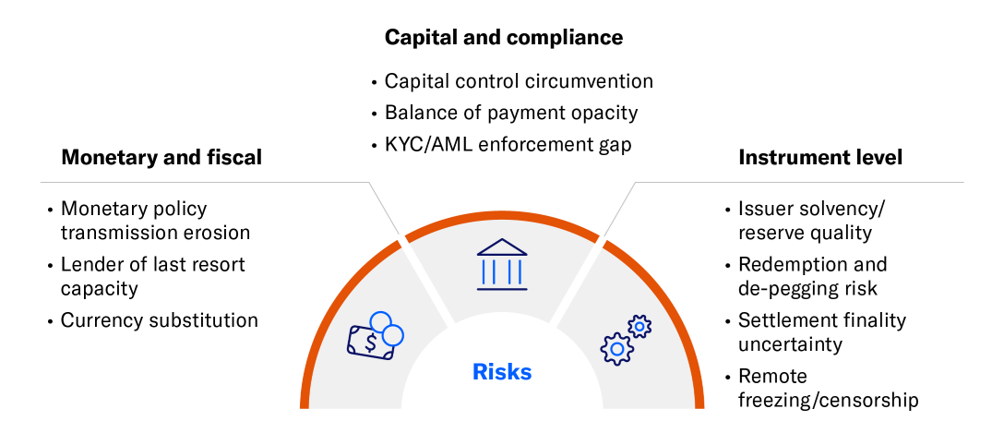

Unfortunately, stablecoins remain far from risk-free. On the surface, they might seem familiar, offering the same as banks and money market funds, only with shinier technology to enable faster transactions. But take a look under the hood, Moody's cautions, and a different picture begins to emerge.

Graphic: Stablecoin holders are exposed to operational and technological risks, says Moodys

“Most stablecoins operate on public, permissionless blockchains, settle peer-to-peer between pseudonymous wallets, are typically not directly redeemable by issuers to retail holders, and circulate freely across borders outside the regulatory boundaries that govern comparable instruments,” it said. “These structural features shape how risks could emerge and spread.”

The most obvious threat to an investor’s wallet comes from the asset backing a stablecoin, in the form of credit risk – that an issuer of a security defaults – and market risk, that an asset loses value before it can be sold to meet redemptions. “Both risks diminish when reserves sit in cash and very short-dated government paper,” said Moody's, “and increase as issuers move into longer-dated debt or lower-quality assets such as commercial paper or obligations with low credit quality.”

But stablecoins also come with their own baked-in concerns, what Moodys calls “technology risk” – namely, a reliance on blockchain and digital smart contracts to keep on top of things like asset ownership and transfers. “Coding errors, network congestion, validator failures or cyberattacks can all disrupt timely settlement,” said Moody's.

Liquidity risk is also a factor. If an issuer is unable to convert assets to cash quickly enough to honour redemption requests on demand, they could find themselves out of pocket. “If reserves include securities with maturities longer than the redemption obligation, or assets that lack a deep and liquid secondary market, the issuer may face delays or losses in liquidating them,” said Moody's.

Tokenized deposits ‘natural evolution’

Perhaps this prevailing mood of caution explains why tokenized money and financial assets, while very much “live” in the US, remain “narrowly used”. However, if there is a wind of change about to blow here, Moody's predicts it will be driven by tokenised deposits, which it says banks view as a “natural evolution” even as they remain wary of stablecoins. “Because most consumers and corporations have shown little interest to date in tokenised money, many market participants do not believe payments alone will drive greater adoption of digital money,” said Moody's.

By contrast, it believes demand will grow if tokenized financial assets take off, requiring on-chain settlement to enable T+0 transactions that are instantaneous. But until that shift occurs, stablecoins will remain largely the preserve of those engaged in cryptocurrency trading and – to a lesser extent – cross-border retail transactions. “Banks view tokenised deposits as a natural evolution, in step with an eventual increase in tokenisation of real-world assets, but generally eye stablecoins warily,” said Moody's.

Indeed, banks appear to view tokenized deposits as a safer bet than stablecoins, with many choosing to favour their own in-house issuances so they can get into the game without abandoning familiar territory. “The strategy of most banks is to prioritize their own bank-issued tokenized deposits within the regulated banking sphere, while staying ready for stablecoins,” said Moodys.

It adds that tokenised deposits are also more attractive to stablecoins because they “leverage the existing interbank clearing and central bank settlement framework”. Essentially, established financial institutions don’t like the idea of non-bank actors like fintechs crowding the space and sidestepping the tried-and-tested guardrails. “Many banks view privately issued stablecoins as a potential threat that could allow non-banks or tech firms to bypass incumbent banks in payments and other services and potentially operate under different compliance, regulatory and legal frameworks depending on the applicable regime,” said Moodys.

Emerging markets beware...

Stablecoin risks become compounded in emerging markets. Digital dollar uptake might be good for the US – but it’s not necessarily good for other jurisdictions. This could well be precisely what the US wants of course, with Moodys noting that growing uptake of dollarized stablecoins “could extend the reach of the dollar into economies where it is not the official currency”.

“The risks above apply to any stablecoin holder, but their consequences fall unevenly across jurisdictions,” it said. “A majority of stablecoin holdings sit outside the US, with emerging markets accounting for the bulk of those non-US holdings.” Though it says hard data by region is difficult to come by, Moodys believes that dollar stablecoins are largely held in these jurisdictions alongside local currencies.

“The most consequential risk is the erosion of monetary sovereignty,” it said. “A central bank steers the economy primarily by changing policy rates, which affect the rates banks charge on local-currency loans and pay on local-currency deposits. If domestic users hold their savings, set prices and settle transactions in dollar-pegged stablecoins instead of local currency, this transmission mechanism weakens.” Rising uptake of dollar-stablecoins could also lead to greater fiscal opacity in such regions. “Cross-border flows of value that bypass the domestic banking system are harder to capture in the balance of payments,” said Moody's. “So when a domestic firm pays an offshore supplier with a stablecoin, the transaction may not appear in the current account, leading to understated deficits and obscured capital outflows.”

Furthermore, dollarized stablecoins could weaken fiscal revenues by facilitating tax evasion. “Tax authorities would face greater difficulty observing transactions that settle on blockchains rather than on regulated payment rails, opening new avenues for evasion,” said Moody's.

Triple As for Fidelity’s token fund

The concerns noted across its three reports didn’t stop Moody's issuing another bulletin on May 13, announcing it had awarded the coveted “Triple A” rating to Fidelity International’s tokenised liquidity fund. “The assignment of the Aaa-mf assessment reflects our view that the fund will have a very strong ability to meet its objectives of capital preservation and high liquidity,” Moody's announced.

It stresses that Fidelity would hold “a significant portion” of its assets in readily transferable “overnight” deposits. “As a result, we anticipate the fund will have very low exposure to market risk,” added Moody's. “We expect that modest shareholder concentration risk [...] will diminish as the fund grows in size and its shareholder base diversifies.”

As Moody's notes, “the stablecoin market is not monolithic – it spans several different instruments with different risks”. Tokenization might be a new game, but it will have its winners and losers just like the old game. And, right now, it seems the winners look more likely to be found among big banks and developed countries.

Events on our radar

DigiAssets Connect Zurich, 16-17 June - Custody, banking, and institutional infrastructure – tickets HERE

European Blockchain Convention 12, Europe’s Deal Floor for Digital Assets. BARCELONA · 16-17 SEPTEMBER 2026 - tickets HERE