Welcome to the weekly letter from TheIntersection team. Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: Securitize Clears SEC Hurdle for NYSE Listing

- Data: Investors rotate out of crypto into equities amidst IPO craze

- Analysis: Blockbuster summer debate over stablecoins heats up at central banks

- Opinion: What's the point of programmable DeFi?

- Our weekly events round-up

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

News in Brief

Securitize Clears SEC Hurdle for NYSE Listing. Securitize, the market-leader in RWA tokenisation infrastructure, is one step closer to becoming a publicly traded company. The platform cleared a major SEC hurdle for its upcoming SPAC merger. Shareholders are scheduled to vote on June 29. If approved, the company will list on the New York Stock Exchange under the ticker "SECZ". Why It Matters: Securitize currently boasts $4 billion in assets under management (AUM) and partners with giants like BlackRock, Apollo, and Hamilton Lane. A public listing on the NYSE represents a monumental bridge between traditional finance (TradFi) and on-chain assets.

.

Citi Forecasts RWA Market to Hit $5.5 Trillion by 2030. In its newly released "Tokenization 2030: Wall Street On-Chain" report, Citi outlined an incredibly bullish future for the sector. While the current global market for tokenized securities sits around $17 billion, Citi notes that accelerating adoption could drive the market to $5.5 trillion (and potentially up to $8.2 trillion) by the end of the decade. Why it matters: Citi expects that up to 10% of the U.S. Treasury bill market will be tokenized by 2030, driven heavily by stablecoin issuers looking for yields.

SEC Approves Rule for Tokenized Equities on NASDAQ. The SEC has approved a key NASDAQ rule change allowing tokenized Russell 1000 securities and major ETFs to trade directly on the exchange. These tokenized shares will be fully fungible with traditional shares and sit on the exact same order book, laying the groundwork for 24/5 equity trading.

Investors rotate out of crypto into equities amidst IPO craze

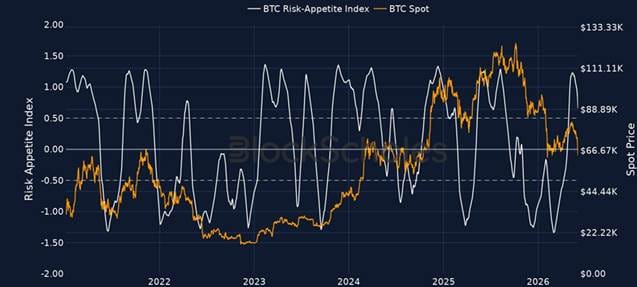

According to Thahbib Rahman, Research Analyst at Block Scholes, an institutional crypto derivatives data and analytics firm, risk sentiment across crypto majors has continued to weaken over the past week (June 5th)th. The recent leg lower in BTC and ETH has coincided with Michael Saylor’s Strategy Inc. selling $2.5M of its $52B BTC hoard, breaking the CEO’s "Sell a kidney if you must, but keep the Bitcoin" mantra, as well as the longest outflow streak from spot Bitcoin ETFs since launch. While it is tempting to view BTC’s drop towards the low $60K region as reflective of risk sentiment across the entire crypto market, this is not exactly true. Speculative froth has built up in other areas of the market where risk appetite remains high.

Chart — Block Scholes’ in-house BTC Risk Appetite Index. Values above 0.5 indicate a transition into a more bullish momentum regime, while values below -0.5 indicate a transition towards bearish spot price momentum

Equity-perps are the buzz

There is some evidence of a potential capital rotation, or at the very least, speculative froth, in perpetual futures contracts tracking real-world assets, as well as pre-IPO perps, at the same time we see weakening in BTC and ETH sentiment. Focusing on Hyperliquid, the decentralised venue that has now become synonymous with price discovery outside of market hours, volumes in BTC and ETH perps are pinned near multi-quarter lows ($2B for BTC and $0.6-0.7B for ETH, respectively), while pre-IPO equity perp volumes have roughly 25x’d over the same period of time. More broadly, crypto-native speculators have found a particular interest in real-world asset perp contracts that provide 24-7 access to macro-assets.

Chart — HL daily notional (7d rolling, log) including the three top non-crypto perps from the xyz HIP-3 dex: XYZ100 (green), SP500 (blue) and CL/WTI (orange). All three individually rival or exceed ETH on HL; cumulatively they're now larger than ETH. The pre-IPO complex (yellow) is the spike on top of a much bigger structural rotation.

The three highest-volume perp contracts on the platform are XYZ100, a Nasdaq-100/ QQQ equivalent, SP500, an S&P 500 equivalent and CL, which tracks WTI crude oil prices. Together, those three perps have seen $1.3B per day in combined volume and $27.1B of notional volume over the last 30 days — equivalent to 112% of Hyperliquid’s ETH perp volume and ~38% of its BTC perp volume.

The rotation is not measured in matched dollars; instead, it is more reflective of a rotation in the attention that had previously been used to backstop bids in the majors, now finding itself in a different corner of the market. When price weakens while turnover is already compressed, as we see with BTC and ETH, it is a sign that no committed buying is stepping in to absorb supply.

A more niche market interest

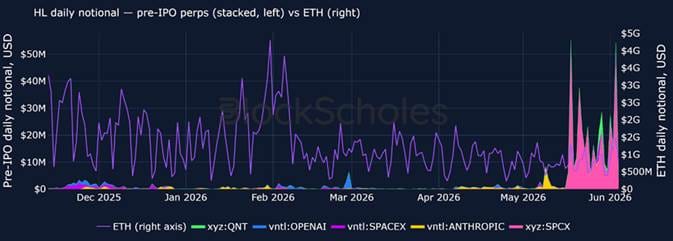

Crypto-native punters are also finding the pre-IPO segment of the market of particular interest. These perp contracts provide economic exposure to privately listed companies, with the ratio of pre-IPO perp volume to ETH notional perp volume rising from a negligible ~0.1% to a peak of 3.0%. Volume has jumped from a sub-$5M/day baseline to upwards of $50M/day, led by perp contracts tracking SpaceX.

Chart — Pre-IPO perps stacked (left axis) vs ETH (right axis): the pre-IPO stack erupts to ~$50M/day into early June, even as ETH notional (purple) stays subdued — the attention spike sits squarely in the new instruments.

The overall picture

The sell-off in BTC and ETH below key support levels does not reflect the entire crypto market. Risk-appetite remains considerably high in tokens such as Hyperliquid’s HYPE token, the only major asset where our Risk Appetite Index is ticking higher, as well as in real-world asset perp contracts and pre-IPO markets. Traders are utilising venues which provide access to BTC, ETH as well as a basket of other assets under a single roof, which is appearing to, at least partly, take interest away from our traditional majors.

About Block Scholes

Block Scholes is an institutional-grade crypto derivatives research, analytics, data and oracle provider. Its data is available on the Bloomberg Terminal, where it provides BTC and ETH crypto options volatility surfaces and related analytics to institutional users. https://www.blockscholes.com/

Asset-backed to the future: Blockbuster summer debate over stablecoins heats up at central banks

Bailey and Lagarde among the star names speaking on the future of regulation for a $300bn asset class, as a US ban on a Fed-backed digital dollar looms

By Michael Hunter

An intense debate among some of the biggest names at global central banks has broken into the open this summer over the future of stablecoin regulation. It is likely to define much of the next phase of international development of the cutting-edge financial tech. And the stakes are high for policymakers, much of the banking industry and investors alike. According to the European Central Bank (ECB), between $300bn and $320bn has already been pumped into stablecoin instruments globally.

The 2026 summer debate has heated up as stablecoins gain traction with retail investors and move more deeply into the mainstream and the global financial system, via some of the world's most influential banks and brokerages. Discussions have been broad.

They have been held at a range of venues, from Federal Reserve policymakers at set-piece conferences on the Dalmatian shores of the Adriatic and the president of the ECB at a historic castle in Catalonia, to a “fireside chat” deep within the bluff, Portland Stone walls of the Bank of England between its longstanding governor and one of the most respected economic commentators in the word.

All of these influential voices, and more, will be heard in this story. It is an account of the latest thinking at major regulators, and the faultlines between them, on the opportunities and threats posed by the rise of stablecoins, one of the hottest topics in finance. The themes include systemic risk during any run on the assets and the need for international consensus on their regulation amid rapid innovation. Taken in combination, these ideas will define the next steps for this latest form of digital finance, which is typically backed by reserves of more traditional assets and uses the blockchain to verify legitimacy and ownership.

The debate also plays into stablecoin’s longer-term future as a fully established means of exchange, one of the key characteristics of money itself, and the obstacles to them achieving that status.

Broader reach for the dollar – and the Fed

In the immediate term, Fed policymakers have indicated that the growth of non-state stablecoins means nations outside the US will be influenced by interest rate decisions it takes. Christopher Waller, a Fed governor, told the 32nd Dubrovnik Economics Conference in late May, that using dollar-backed stablecoins internationally meant that:

“You are going to import US monetary costs, so it’s broadening the reach of US monetary policy in countries that use more stablecoins.” Currently, stablecoins are predominantly rooted in the United States. The vast majority of the market capitalisation of the global supply is pegged to the dollar, largely via the two dominant stablecoins, Tether’s USDT and Circle Internet Financial’s USD Coin (USDC). The ECB estimates that between 97 per cent and 99 per cent of the aggregate value of stablecoins is linked to the dollar. That gives politicians and regulators in the world’s biggest economy, including President Donald Trump, a louder voice in the debate over how the instruments are overseen.

Their counterparts elsewhere seem keener to be heard over the risks they perceive and what should happen next. Although they are simultaneously keen to innovate themselves, adding another plotline by setting up the prospect of rival digital coins with direct government backing as alternatives to the dominant digital dollar-backed ones currently run in the private sector.

New Fed chair backs private sector stablecoins

Waller, a Trump appointee to the Fed’s board, also backed stablecoin for use as a means of exchange: “I’ve always just looked at stablecoins as a payment instrument; there’s nothing evil about it, nothing dangerous about it.” The Fed’s approach since Trump’s return to power has been to back financial innovation, with a broader openness to integrating new technology into day-to-day payment infrastructure. It's new chair – Kevin Warsh, another Trump appointee who succeeded Jerome Powell as the world’s most influential central banker in late May – personifies the White House's thinking on digital money. He is a keen supporter of private sector stablecoins and is set against government-backed alternatives, known as Central Bank Digital currencies, or CBDCs. They are under consideration elsewhere, especially in Europe. But if a looming piece of legislation currently under discussion in Washington, the “Digital Asset Clarity Act”, makes it into law as written, a Fed-backed digital dollar will be banned.

The US passed its pioneering digital money legislation in 2025. The “Genius Act”, short for Guiding and Establishing National Innovation for US Stablecoins, opened the way for stablecoins to enter the mainstream, regulated financial infrastructure, so they can be used as a means of payment. In effect, the Genesis Act allowed the private sector to step in to digitise money as stablecoins. Warsh believes the innovation has proved successful and that digital assets is now part of the financial mainstream, and should be adopted more widely.

Actual arrangements for the specific rules concerning capital requirements, liquidity and oversight are still being drawn up. But the Genesis Act established what it refers to as “permitted payment stablecoin issuers”, or PPSIs.

US Treasuries and stablecoins

This area brings a vital part of the summer debate into view: Stablecoins as a means of deepening demand for US assets, currently predominantly the dollar, but also, potentially, for US government debt, all via the private sector.

Stablecoins backed by Treasuries are seen by some close to the Trump administration as a useful new source of demand for US government debt. Any such development would bring Treasuries, the cornerstone assets of the financial system, into this new wave of financial technology. Warsh and the Trump administration’s opposition to a direct role for government in digital money means any such move is likely to be led by the private sector. Elsewhere, policymakers are more unnerved by potential dangers of leaving such backing to firms.

In London, some top-level officials see a route to potential systemic risk, especially the current lack of an international regulatory framework for stablecoins, which remains ahead of any move into the crucial Treasuries market.

Fireside chat

It came up at the BOE’s fireside chat, between Andrew Bailey, its governor, and Martin Wolf, the chief economics commentator of the Financial Times, held in May as part of annual Bank of England Agenda for Research conference. Bailey himself raised the question of “why is the US administration pushing stablecoins?” before offering an answer:

“They are a home for US Treasuries as the backing assets … the expansion of dollar stablecoins around the world has the benefit as seen through the lens of the administration as a growing home for US Treasuries.”

Wolf questioned the stability of a system in which “everybody becomes increasingly a creditor of … a power that is seen as irresponsibly led, to put it mildly”. In reply, Bailey pointed to the importance of the BOE’s determination to “strongly support and underpin … the revival of multilateral institutions” of global finance. It was a reference to the World Bank and the International Monetary Fund, the international institutions that are required to help define and support multilateral rules, as well as to the Basel Committee on Banking Supervision.

Speaking truth to power

Such bodies have been undermined by a lack of international consensus and growing political tension, especially between the US and China and Russia. That has led to what Bailey called “a fracture that is very apparent on the G20”, one of the main convening mechanisms for the heads of government for the 20 biggest national economies. It was the G20 meeting in London in 2009 that established the coordinated international response to the financial crisis, which pulled the system back from the brink. Should any such action be needed in the future during a run on digital assets, it would probably be the main forum for it. The United Kingdom is due to chair the G20 in 2027, taking over from the US.

Bailey said, “We’re going to have to preserve it and seek to rebuild it. Part of that is to give the IMF the confidence to speak truth to power. “We have to have an institution that A, has the quality of analysis and assessment and B, the ability to speak it an convey it. If that decays, we are in a very bad situation … without having that [multilateral institutional] structure, we are in a much more dangerous place … we are at a critical time in that respect.

“The IMF needs to refocus. It sounds Trumpian. But it needs to refocus on its core mission”.

Bailey also chairs the Financial Stability Board (FSB), which monitors and makes recommendations on the global financial system and was established in direct response to the crisis. He added later that there was a need for international agreement on the rules governing financial supervision and oversight.

“The point I’ve made to the US banks, it seems like forever, but it’s probably a year or two, is that Basel is a prudential standard. But it is also the thing that sets the playing field apart. You don’t have a playing field unless you have this. So you want this. It is in your interest that there is Basel.

“The FSB’s role is [that] we need the same thing in stablecoin. If we want stablecoins to be part of the architecture of payments globally, and we want to improve cross-border payments, then we need them. But they are only going to work if we have international standards.”

Wrestling with Trump – and the meaning of money

“And that is going to be a coming wrestle with the administration, who see this as a scope to spread [stablecoins] around the world. But it’s marking out the playing field.” Wolf asked Bailey if he “shared the view” that stablecoins are a potential cause of a significant threat to financial stability. The governor replied: “Yes, if they develop the function of money and they don’t have the property of money, which is assured nominal value, then yes.”

Another major BOE figure, Megan Greene, a member of the rate-setting Monetary Policy Committee, cast doubt on the longer-term prospects of stablecoins more generally. At the same Dubrovnik conference at which Waller spoke, Greene said “I suspect we might wonder why we were talking about stablecoins.” She raised the prospect of a rival to the assets from tokenised deposits at banks, digital versions of holdings at traditional financial institutions which could take on the same role as stablecoins without the same extent of risk.

“I think tokenised deposits are probably going to take over from stablecoins and five years from now”. In the meantime, Greene pointed to some of the dangers linked to stablecoins from the perspective of traditional finance. That includes their potential uses for illicit purposes as well as the potential lack of stability depending on how they are backed. And she warned that if stablecoins pull deposits away from banks, their rise could weaken central banks' ability to transmit monetary policy through the system, a distinctly different view from that expressed at the same event by Waller.

Europe’s digital fiat drive

Throughout, the ECB is keeping a careful watch. It is seen as one of the major monetary institutions most well-disposed toward CBDCs. A fully digital euro would have direct backing as an electronic asset from one of the world’s major central banks. It would immediately be a major competitor to existing stablecoins. With direct backing from an issuer of traditional currency, known as fiat money, a digital euro would carry less risk than private-sector forms of digital money, which must buy assets to back them rather than issue them. That would be even safer than the idea of digitised traditional deposits highlighted by the BOE’s Greene. At the Castillo de Bará in Tarragona, Spain in May, Christine Lagarde, the ECB’s president, cast doubt on private sector stablecoins. She told the inaugural Banco de España LatAm Economic Forum of a “fundamental question”:

“Do we actually need stablecoins to obtain the benefits they are said to provide? Or are we mistaking the instrument for the outcome, when what matters is the architecture underpinning which other instruments can safely emerge?”

She concluded:

“Our task is not to replicate instruments developed elsewhere, but to build the foundations and the infrastructure that serve our own objectives, so that we can harness the benefits of innovation without importing the fragilities.”

Bonds on the blockchain

Across the English Channel, the BOE seems to have had similar thoughts, but about UK government bonds rather than currencies. Sarah Breeden – its deputy governor for financial stability and a leading candidate to take over the top job from Bailey when his term expires in March 2028 – spoke of the BOE’s role in helping to set up a digital version of Gilts, or UK government debt, alongside the Treasury and the Financial Conduct Authority in London.

Putting sovereign bonds on the blockchain or a similar distributed ledger technology (DLT) that underpins digital assets could open them up to new buyers. Increased demand may then, in turn, bringing down the yield on the debt, and so the costs to the taxpayer of servicing it. Addressing at the 16th City Week conference at The Royal Garden Hotel in Kensington, Breeden said:

“We are committed to supporting the Government’s pilot issuance of a digital gilt instrument (DIGIT) – the first tokenised sovereign issuance by a G7 country – designed both to enable the Government to explore how this technology can be applied to UK government debt and to catalyse the development of UK-based DLT infrastructure and, in turn, adoption across UK financial markets.”

Breeden also seemed to signal this summer that the BOE could take a less strict approach to stablecoins, after a previous outline of its intentions sparked a backlash among crypto investors. It had planned to insist on tight caps on stablecoin holdings for both individuals and institutions. It also intended to require stablecoin issuers to hold 40 per cent of the assets backing the coins in BOE accounts that would not pay interest. The intention was to limit the risk of a run on stablecoins, helping protect their nominal value during any wave of redemptions, a concern Bailey and Wolf discussed. But stablecoin issuers argued that the regulations would stifle innovation and curb take-up. Breedon told the conference that the BOE was “working to expand the range of settlement assets” being considered “to include not only tokenised deposits, as today, but also regulated stablecoins in sterling and foreign currencies.” The full details of BOE’s latest plans will be revealed “soon”, she said, “shortly after publication of our draft rules for systemic sterling stablecoins”, which is expected later this summer, at around the same time the US unveils its own set of similar rules.

Trans-Atlantic rift

In Washington, where CBDCs are so firmly out of favour, the extent of the trans-Atlantic rift on digital money is being laid bare on the floor of Congress. The mooted ban on a Fed-backed digital dollar in what will become the Digital Asset Clarity Act would mean, in effect, that there would be no government-operated rival to Tether’s USDT or Circle’s USDC.

The stringent provision comes as the BOE eyes digital Gilts, while internal debate over stablecoins continues. And while the ECB pledges further innovation, perhaps toward a fully digital euro, an idea it is exploring in depth and in public. It amounts to a dramatic divergence of vision over the next financial frontier. The outcome of the summer debate over digital assets looks likely to set the tone for how digital money will operate and internationalise at a tense time for global relations.

Very stark regulatory differences in vital areas of the global financial system could prove to be a danger in themselves, if Bailey’s advocacy on the importance of an internationally agreed playing field is overlooked as summer fades and central bankers head into the autumn, and the longer-term future for stablecoin, and digital finance itself.

What is the point of tokens?

By Adam Bawi, Director of BD at Centrifuge

A few weeks ago, I was chatting with one of my traditional asset manager friends about the recent rise in RWAs on-chain, where they hit me with the simple and honest question: "So, Adam, what the fuck is the point?" Over the past few weeks, it got me thinking about this dislocation in perceived value of RWAs on-chain, and how widespread this gap truly is across the market that this industry will be inevitably tapping into. Sure, many media figures will throw buzzwords out and say that "2026 is the year of RWAs" and "tokenisation is the future", but how many of us know how this is achieved? how many of us understand what this looks like in practice?

Putting treasuries on a blockchain and calling it RWA adoption was a nice starting point, but it had no right to call it "real adoption". Most of the RWA volumes and TVL we have seen on-chain to date have been a product of this, with DeFi allocators committing to the tokenised representation of RWAs and letting it sit in their wallets. The uncomfortable admission: you've arguably made it worse on-chain with higher costs (chain-dependent), regulatory overhead, and smart contract risk. Issuance is not innovation - this is merely the 'ground floor' integration level.

We haven't yet had that 'crossing the chasm' moment for RWAs.

Electric Capital published a report last week mapping 501 distinct real-world yield sources. Only 34 have any meaningful on-chain presence above $50M. 93% remain completely untouched by defi. Of $8.5B in RWA-backed stablecoin supply, only $1B (12%) is actually deployed in defi protocols. The other 88% sits idle behind KYC and whitelisting walls.

We’ve spent billions tokenising assets, and most of them are just sitting there. That’s a bank account with extra steps. So - what is the point? The point isn’t issuance. It isn’t “24/7 trading” or “fractional ownership.” The point is what happens after the asset lands on-chain. The point is integration. And it boils down to three things.

1. Programmable Collateral

This is the big one. This is where the entire thesis lives or dies. For years, defi has been running on a fundamentally broken collateral model. ETH backing ETH-denominated loans. Volatile tokens securing volatile positions. The same assets being used as both the collateral and the thing being leveraged. This is not financial innovation - it's a circular firing squad.

When prices rise, collateral strengthens, more leverage enters, and everyone feels like a genius. When prices fall, cascading liquidations. We saw it with Terra/Luna. We saw it with 3AC. We saw it around October 10 last year. Every single one traces back to the same root cause: reflexive collateral. The system's foundation was eating its own tail. This is not a risk management failure. This is an architectural one. You cannot build a stable financial infrastructure on collateral that moves in lockstep with the positions it's securing.

Now imagine collateral that generates real yield, is not directionally tied to ETH or BTC, is backed by cash flows off-chain, and has fundamentally different risk drivers. That's what tokenised RWAs introduce.

A tokenised S&P 500 position earning spot returns while simultaneously collateralising a lending position on Morpho, generating borrowed stablecoins that get redeployed - all in one composable stack. No prime broker. No phone call. No counterparty chain. In tradfi, this same trade touches a custodian, a margin desk, a PB, a transfer agent, and takes days. On-chain, it's one token doing multiple jobs simultaneously.

Or take it a step further - use that same tokenised S&P 500 position as margin collateral on a perp exchange. Your margin isn't dead, USDC is earning nothing. It's an interest-bearing position that generates spot returns while backing your leveraged trades. The collateral is working two jobs at once, and neither one requires the other to stop.

The yield is real (not emissions). The collateral is productive (not dead). The infrastructure is permissionless (not gated).

Using non-reflexive assets as base collateral reduces the feedback loops that cause cascading failures. They don't eliminate risk, nothing does, but they change the reflexivity of the system. And that changes everything about how much leverage the system can safely absorb.

Interest-bearing tokens are the future of collateral. Your S&P 500 exposure earns while it collateralises. Your AAA CLO position generates income while it backs your margin. Dead capital becomes productive capital. Leverage isn't the problem. Weak collateral is. And RWAs are one path toward fixing that foundation - but only if they're actually integrated into the infrastructure, not left sitting idle in a wallet.

2. Market Creation

This is the one that makes traditional finance people sit up when they finally get it. Tokenising an asset doesn't just put an existing product on new rails. It spawns entirely new markets and strategies around it that were structurally impossible before.

Take deSPXA - a tokenised & decentralised S&P 500 spot asset. S&P 500 perpetual futures recently started trading on Hyperliquid. Deploy the spot token onchain and you've just invented a basis trade that didn't exist 12 months ago: long spot, short perp, collect funding. Cash-and-carry on crypto rails. This is a trading strategy that attracts a participant class - basis traders - who have zero interest in the underlying asset itself. They don't care about the S&P 500. They care about the spread. And that spread only exists because the spot RWA lives onchain alongside the derivative.

Or consider secondary market pricing. A tokenised fund creates a continuous secondary price on a DEX. That creates an arb between the pool price and the fund's NAV. In the ETF world, Authorised Participants close this gap through a formal create/redeem mechanism with contracts, legal agreements, and multi-day settlement. On-chain, any whitelisted participant with capital can arbitrage the spread permissionlessly. The price correction mechanism is native to the infrastructure.

Then there are lending markets for asset classes that have never been borrowable against. Private credit. Litigation finance. Structured products. These are not incremental improvements to existing tradfi markets. They're financial primitives that only exist because the asset is onchain and composable.

These aren't theoretical. Morpho has $6.8 billion in TVL with RWA deposits representing approximately 10% and growing. Aave Labs are building Horizon specifically for permissioned RWA collateral with permissionless stablecoin liquidity. The infrastructure is being built right now. The question for the tradfi friend isn't "why would you put it onchain?" It's "what markets become possible once you do?"

3. Composable Infrastructure

This is the meta point that ties the first two together, and it's the one that the traditional finance world fundamentally doesn't understand because it has no analogue in their architecture. Every tokenised asset that follows an open standard - ERC-20, ERC-4626, whatever comes next - is automatically compatible with every protocol that supports that standard. No integration partnership. No API build. No BD call. No legal review of a bilateral agreement.

Morpho doesn't need to sign a contract with JanusHenderson Investors to create a JAAA lending market. An Aerodrome Finance pool doesn't require a formal market-maker agreement to list a tokenised S&P 500 pair. A vault on any protocol can accept any compliant token as collateral the moment it's deployed.

In tradfi, the same process involves transfer agents, SWIFT messages, multiple settlement cycles, and at least three people who are “currently in a meeting.” On-chain, it’s a single atomic transaction. Every intermediary in that chain doesn’t get disrupted - it gets made structurally unnecessary.

This is why permissionless assets like reUSD hit 96%+ utilisation rates while permissioned RWAs sit at 12%. Composability is not a ‘nice to have’ feature. It is the mechanism that determines whether a tokenised asset actually does anything useful or just collects dust on-chain. The infrastructure that enables programmable collateral, that enables new market creation, that enables all of the above - it exists because of open standards and permissionless composability. Everything else is a consequence.

But only if the plumbing is right

I want to be clear about something. Everything I've written above breaks if the infrastructure is lazy. Everyone likes the "extra yield" part. Fewer want to talk about duration alignment, collateral quality, oracle integrity, and liquidation design. That's the line between productive leverage and fragility.

Conservative LTVs. Proper oracle design. Duration alignment. Realistic liquidity assumptions. These aren’t optional. As I write this, Resolv Labs' USR stablecoin just lost its peg after an attacker minted $80 million in unbacked tokens using $200k. The minting contract had no max mint limits, no oracle checks, and a critical admin role secured by a single private key instead of a multisig. Within hours, the damage had cascaded into Morpho vaults, where USR was accepted as collateral - traders bought the crashed token at a discount and borrowed USDC against it at the hardcoded $1 valuation, draining stablecoin liquidity from lending pools that had nothing to do with Resolv.

This is not meant as a shot at the Resolv team - they're genuine builders and this industry needs more of them, not fewer. But it's a brutal reminder that the gap between "functioning protocol" and "battle-tested infrastructure" is measured in exactly these kinds of details. A single key with no guardrails. No max mint check. These are not sophisticated attack vectors. They're basic engineering oversights that become catastrophic when real capital is on the line.

And the concentration risk across the sector is just as real. BlackRock's BUIDL has 98% of its supply controlled by its top 10 holders - and those holders are mostly other protocols. When the largest "institutional" RWA product is effectively a few protocol treasuries stacked on top of each other, you haven't built broad-based adoption. You've built a Jenga tower.

If RWA loops are going to mature into real financial infrastructure, the plumbing has to be as robust as the upside is attractive. Otherwise, we just recreate tradfi fragility on-chain, which would be the most expensive way to learn nothing.

So - what is the point? The point isn't "put treasuries on blockchain”.

The point is that on-chain infrastructure makes assets programmable, composable, and structurally useful in ways that tradfi's siloed architecture physically cannot replicate. "Programmable" and "composable" sound like buzzwords. They're not. They're an engineering reality. And it's a reality that 88% of tokenised assets haven't figured out yet. The question isn't whether this happens. The question is whether the people building it are honest about what actually matters - and whether they have the discipline to build the infrastructure properly, or whether they're just going to keep issuing tokens and calling it innovation.

We haven't crossed the chasm yet. But at least now you know what's on the other side. This is what we're building toward at Centrifuge.

This article originally appeared on LinkedIn HERE.

Events on our radar

DigiAssets Connect Zurich, 16-17 June - Custody, banking, and institutional infrastructure – tickets HERE

European Blockchain Convention 12, Europe’s Deal Floor for Digital Assets. BARCELONA · 16-17 SEPTEMBER 2026 - tickets HERE