Welcome to the weekly letter from TheIntersection team. Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: SEC pauses tokenised stock plans

- Data: Tokenised Equities Hit All-Time High

- Analysis: State Street’s cautious crypto venture

- Opinion: Tokenisation Was Always Five Years Away. Then April Happened.

- Our weekly events round-up

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

SEC pauses tokenised stock plans amid market concerns

The U.S. Securities and Exchange Commission has reportedly delayed plans to introduce a broad exemption framework for tokenised stock trading, slowing what many saw as the next major step toward blockchain-based equity markets. The proposal would have allowed crypto platforms to offer tokenised versions of publicly traded shares through an “innovation exemption” structure. According to reports, regulators pulled back after concerns from exchanges, market structure experts and former officials around investor protections, shareholder rights and the potential fragmentation of equity markets. One of the most contentious issues involved “third-party tokens” — digital representations of shares that could potentially trade without direct involvement from the underlying company. The delay does not appear to signal opposition to tokenisation itself. Nasdaq and the NYSE are both still pursuing tokenised market infrastructure initiatives, and the SEC has previously approved limited tokenised equity pilots tied to traditional settlement systems.

Why it matters: The debate is shifting from whether tokenised equities will exist to how they fit into existing market structure. The technology is largely ready — but regulators are still working through questions around custody, shareholder rights, market fragmentation and oversight before allowing tokenised stocks to scale in public markets.

News in Brief

OCC approvals create a regulated custody layer for tokenised markets

A growing wave of approvals from the Office of the Comptroller of the Currency in the US is helping establish a federally regulated custody framework for digital assets, covering major custodians and tokenisation infrastructure providers.

Why it matters: Institutions have long cited custody and regulatory clarity as barriers to adoption. The emergence of an OCC-backed infrastructure stack could accelerate large-scale issuance of tokenised products.

DTCC moves tokenisation into live market infrastructure

Tokenisation is no longer sitting on the edge of capital markets. With the Depository Trust & Clearing Corporation preparing to launch limited live trades in July, blockchain infrastructure is starting to plug directly into the core settlement layer of U.S. finance.

The Details :

DTCC plans to begin limited production trading of tokenised securities through its new DTC Tokenization Service in July 2026, ahead of a broader launch expected later in the year. DTCC sits at the centre of the U.S. financial system, processing and safeguarding more than $114tn in securities. Rather than creating a separate blockchain market, the organisation is trying to digitise the existing one.

Under the framework approved by the SEC in late 2025, eligible securities — including Russell 1000 equities, ETFs and U.S. Treasuries — can be issued in tokenised form while retaining the same ownership rights and investor protections as traditional assets held through DTC custody. DTCC is developing the platform alongside an industry working group of more than 50 firms, including banks, exchanges, custodians and crypto infrastructure providers. Participants reportedly include firms such as BlackRock, JPMorgan Chase, Nasdaq, Kraken and Ripple.

Tokenised Equities Hit All-Time High

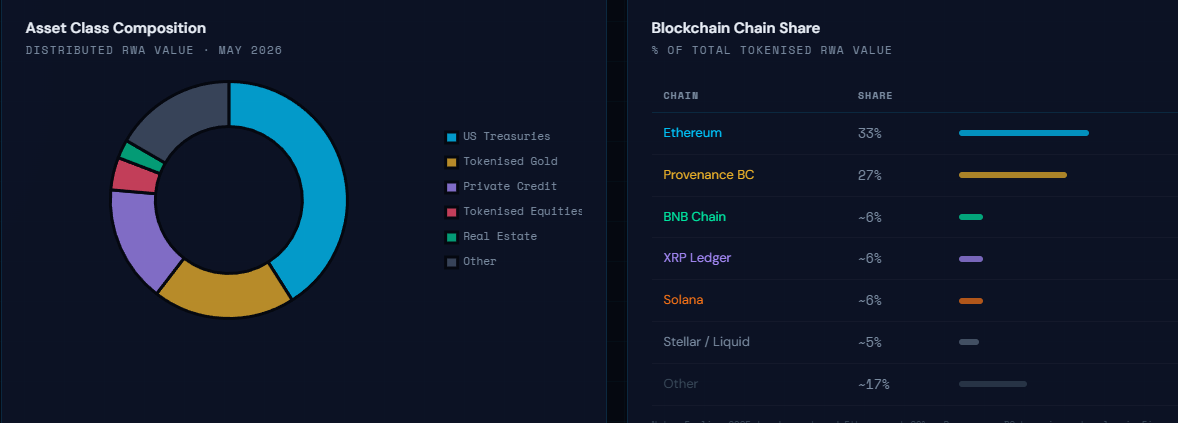

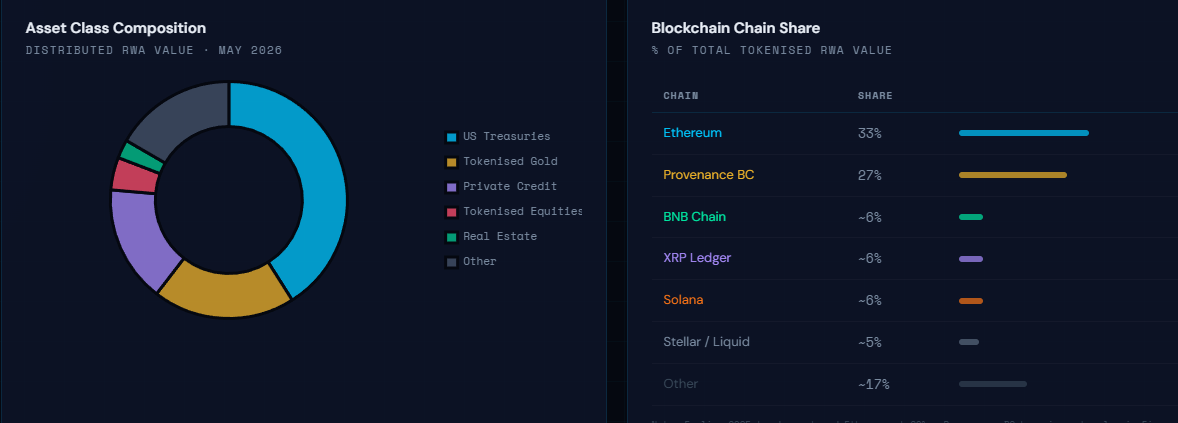

Distributed tokenised RWA value has reached $31.4 billion, up from around $6 billion at the start of 2025. From a broader market perspective, total tokenised RWA value has risen byapproximately 44% since the start of 2026.

Asset class composition. Tokenised US Treasuries remain the dominant category at $12.88 billion. BlackRock's BUIDL fund holds approximately $1.7 billion in on-chain assets as of May 2026, making it the world's largest tokenised Treasury product. Ondo Finance's total tokenised assets under management crossed $2.4 billion in 2026, making it the largest DeFi-native issuer of tokenised government securities.

Equities breakthrough. Tokenised equities hit their highest single-day trading volume on record, reaching $3.57 billion — driven largely by Binance and Hyperliquid, with contributions from Kraken's xStocks, Ondo, and Bitget. Tokenised stocks grew from $375.4 million on May 3, 2025, to about $1.21 billion on May 3, 2026.

Chain shift. Ethereum holds roughly 33% of market share while Provenance Blockchain commands around 27%, anchored by Figure Lending — with BNB Chain, XRP Ledger, and Solana each around 6%. This is a material change from the earlier 60%+ Ethereum dominance figure

State Street’s cautious crypto venture

By Damien Black

State Street is moving ever deeper into tokenization, and will now support ‘digital native’ funds alongside its established TradFi investments. The move is significant – the $5.6 trillion asset manager was once seen as a tech laggard. Well, not any more.

In fact, State Street boasted on 28 April that it would be an “early adopter” of the tokenized fund service, available on its newly minted Digital Asset Platform (DAP). “This allows State Street to support the full lifecycle of tokenized fund issuance, administration and custody,” it said, “while allowing digital and traditional fund structures to operate together under consistent governance, risk management, and a single client interface.” The new DAP fund service will be available in Luxembourg by the end of the year. The jurisdiction was selected as the launch platform because of its digital-friendly policy framework. It hasn’t released hard dollar figures for DAP move at the time of writing, but State Street says it already provides “fund administration” services for around $22 billion in digital assets overall.

DeFi and TradFi under one umbrella

State Street hopes the move will allow it to manage DeFi and TradFi assets within a single unified framework. Angus Fletcher, its global head of digital asset solutions, said: “Investment Services is focused on delivering a production-ready servicing capability, with State Street Investment Management’s planned use of the service providing early validation of how tokenization can be applied within existing fund operating models.” Kim Hochfeld, global head of cash and digital assets at State Street Investment Management, added: “Being an early adopter of tokenization allows us to upgrade our operating model and deliver an innovative client experience while preserving the investment discipline, risk controls, and investor protections that are fundamental to State Street Investment Management.” In other words, State Street believes it can maintain its longstanding reputation for caution and prudence while embracing the new technology and all its benefits.

In the game – but still cautious

Even so, State Street is taking a gamble here. As noted above it has $5.6 trillion assets under management (AUM) – this balloons to a staggering $54.6 trillion for assets under custody. But then with the likes of BlackRock jumping into tokens with its $2.2 billion Uniswap crypto deal[1] , it’s hard to see realistically how State Street could have stayed out of the game. And true to form, State Street has been keeping a close eye on how regulation of tokenization is shaping up. In March the asset giant published a report that noted this year would “likely bring continued focus on how bank capital, liquidity, and exposure limits treat tokenized assets versus their traditional equivalents – with material implications for whether regulated institutions can participate at scale.”

State Street’s focus is on what it calls “operational glue” – the framework set in place around tokenized assets to protect them from things like cyberattacks or being used for money laundering. “As tokenization and digital cash experiments mature, the differentiator becomes the control environment: governance, cyber resilience, AML tooling, and reliable interoperability across rails,” it said.

Token rules – a work in progress

State Street’s take on the 2025 ‘gold rush’ into tokenization essentially appears to be one of work in progress. “Many regulators made the landscape more buildable — without pretending it is finished,” it observed. “For clients and market participants, that shift matters. Clarity lowers operational risk, supports investment in durable infrastructure, and enables more credible hybrid models that bring traditional finance safeguards to tokenized workflows.”

State Street appears most concerned with reconciling this obvious need for safeguards with the kind of innovation that made tokenization possible in the first place. “The 2026 question is whether jurisdictions can keep translating frameworks into consistently supervised regimes — and whether global standards can converge enough to reduce fragmentation without suppressing innovation,” it added.

What do the punters want?

Another report commissioned by State Street and published in October noted that around half of entities surveyed had less than 1% digital asset exposure. However, in spite of that conservative outlook, it noted the “road to tokenization looks promising”. This is because six in ten respondents said they intended to bump their digital exposure to north of 2% in 2026, “signalling a shift toward diversified digital asset strategies”. Perhaps most notably, State Street found that the majority of surveyed companies believed tokenization would in effect become the new normal well within the next decade, with DeFi “a mainstream practice and interoperable with traditional investment operations” within three to nine years. State Street’s cautious but steady foray into tokenization, then, seems but a reflection of what its vast client base expects and wants to see.

Startups... or upstarts?

Another report published by State Street in the past year highlights a key area of importance for the asset manager – that of trust. What the asset giant essentially means by that is credibility. Shiny new tech is all well and good, but to be a reliable source of profit, it must be placed in the proverbial safe pair of hands.

In State Street’s view, banks – which bring decades, if not centuries, of experience in looking after other people’s money to the table – must be the primary guarantors of the trust that will insulate DeFi fromfraud and cybercrime. For the asset giant, the spectre of FTX, which ‘lost’ $10 billion in digital assets before spectacularly folding in 2022, looms large and serves as a cautionary note.

“As a leading [cryptocurrency] exchange, FTX held billions in client assets, but as we learned through its bankruptcy, those funds were commingled and misused (via Alameda Research) with relatively limited oversight,” said State Street. This lack of oversight allowed FTX to play silly buggers with customers’ money to its heart’s content, “with no independent custodian or audit to prevent it”.

The lesson has not been lost on State Street. “The future of institutional digital asset custody is about bringing the best of traditional custody into the digital realm,” it said. “This means exchanges and FinTech upstarts must either elevate their custody practices to meet regulatory standards or cede that role to those who already have the institutional trust.” Yes, you read that right – State Street isn’t talking about startups; the tech bro boys are “upstarts”… Clever word play? Perhaps. But it’s indicative of where the asset veteran stands on the issue of the intersection of DeFi and TradFi.

The more things change...

And in case you’re still wondering where precisely that is, State Street makes it clear enough. Crypto cowboys out, old-school watchdogs in.“Bank-led custody offers a path forward — client assets held with proper segregation, overseen by regulators, backed by capital and insurance, and managed by professionals with deep risk expertise,” State Street said. “Such custodians can drastically reduce the risks of theft, insolvency or malfeasance plaguing the crypto industry.” So be in no doubt. State Street might have joined the tokenization bandwagon, but it won’t be abandoning its prudent outlook any time soon. Once again, this points to what seems to be the inevitable evolution of DeFi – the more it gets co-opted by TradFi giants like State Street and BlackRock, the more it looks like the thing it was intended to replace and supplant in the first place.

Plus ça change.

Tokenization Was Always Five Years Away. Then April Happened.

By Allan Lane, CEO Algo-Chain

Fund tokenization has been five years away for about a decade. Then, on 30 April 2026, it quietly stopped being a future technology and became a regulated one. The FCA's Policy Statement PS26/7 took effect with immediate force, formally bringing tokenized funds inside the UK's existing regulatory perimeter. The regulator's message was unambiguous: tokenization is no longer a parallel experiment - it's the operating model UK asset management is moving toward.

While some still see tokenization as just another wrapper, we see it as a fundamental leap forward in how wealth management operates. PS26/7 confirms the industry's Blueprint model, allowing on-chain records to serve as the primary books for unit deals, and introduces an optional Direct-to-Fund (D2F) dealing model that lets investors transact directly with the fund itself. Together, these changes move us away from fragmented legacy systems and toward a more streamlined, transparent structure.

FCA Consultation Paper - Progressing Fund Tokenisation

The Power of the Programmable Register

Tokenization doesn't change what you own - your strategic asset allocation and ETF selection remain the core of your value proposition. Instead, it revolutionizes how you own it. By moving from manual, disconnected records to a digital, programmable register, the industry unlocks several key advantages:

- Real - Time Certainty: The end of the T+2 waiting game. Tokenization enables near-instantaneous reconciliation and, where the right rails are in place, atomic settlement, providing a definitive source of truth at any second of the day, not at the end of the next business cycle.

- Operational Excellence: Automated smart contracts handle the heavy lifting of dealing instructions, ownership transfer, and corporate actions. Manual reconciliation between platform, transfer agent, and custodian - a process that, in 2026, still depends on people emailing each other spreadsheets - collapses into a single shared register.

- Institutional-Grade Governance: Every transaction is etched into a secure, immutable ledger. The audit trail is materially superior to traditional spreadsheets, CSV exports, or fragmented platform records. The FCA explicitly contemplates on-chain records as primary books, provided firms maintain appropriate resilience plans.

Inside the Dealing Workflow: What T+0 Actually Means

To see why this matters in practice, it helps to look at how a fund deal works today versus how it can work on a tokenized register. Under the traditional model, dealing runs on a single daily window. Orders submitted before a fixed cut-off - typically noon - receive that day's price, with the NAV struck after market close. The units and the cash then take another two business days to change hands. During that T+2 gap, multiple parties - platform, transfer agent, depositary, custodian - each maintain their own version of the trade on their own systems and reconcile after the fact. The reason this still takes two days, in 2026, isn't a technical limitation. It's institutional muscle memory.

A tokenized fund running on the Blueprint model can compress that cycle dramatically. The most consequential change is atomic settlement: where digital cash is available on the same rails, the unit token and the cash token swap in a single, indivisible transaction. There is no settlement window, no failed trade exposure, and no reconciliation lag. The register updates the moment the deal executes. Three practical consequences are worth flagging:

- Dealing windows become more flexible. A fund that today strikes a NAV once a day could, in time, support multiple intraday strike points without a proportional increase in operational load because the work that used to require manual reconciliation is now executed by smart contracts.

- Liquidity management gets sharper. Fund managers gain real-time visibility into subscription and redemption flows rather than waiting for end-of-day aggregates. Cash buffers held purely to absorb settlement-timing risk can shrink, reducing cash drag on performance.

- Stress resilience improves. During events like the 2022 LDI episode, where forced gilt sales amplified a downward price spiral, faster settlement and tokenized MMF units that can serve as collateral materially reduce the friction that turns liquidity events into systemic ones. The FCA cites this dynamic explicitly in its policy paper.

It's worth being clear-eyed about the transition. True T+0 requires a credible on-chain cash leg, whether for tokenized commercial bank deposits, regulated stablecoins, or eventually wholesale central bank digital cash. The FCA has left the door open via its waiver regime, but the full benefit arrives in stages. The Direct-to-Fund model is a separate reform: it streamlines who an investor deals with (the fund itself, not an intermediary chain) and works for both conventional and tokenized funds. The two changes reinforce each other but solve different problems.

A Framework Built for the Next Cycle

Most firms have spent the last decade perfecting portfolio construction. Rather fewer have spent it perfecting the plumbing that delivers it. That gap is about to matter more than it used to. The next competitive edge in wealth management won't come from finding a niche ETF or shaving another basis point off a passive sleeve. It will come from operational agility: the ability to implement, monitor, and adjust portfolios with the same precision used to design them.

Tokenization bridges the gap between disciplined portfolio design and institutional-grade control. It allows model portfolios to be treated as truly integrated systems where allocation, implementation, and monitoring happen in perfect sync rather than as instructions handed off to a chain of intermediaries, each running their own ledger and reconciling after the fact.

The FCA's longer-term roadmap - moving from tokenized funds to tokenized assets and, eventually, tokenized cash flows - points toward what it now describes as composable finance: modular, DLT-based investment processes that can be assembled and reconfigured without rebuilding the plumbing each time. The phrase is awkward; the idea is not. And it isn't a 2030 thesis either, it's a direction of travel the regulator has already committed to refining through further consultation on DLT in wholesale markets later this year.

From Theory to Adoption

This is no longer hypothetical. Baillie Gifford launched the first tokenized UK OEIC in mid-2025. Federated Hermes tokenized European money market funds, including the first UK-domiciled TMMF, later the same year. Aviva began a fund tokenization project with Ripple in early 2026. The Investment Association's IF3 Lab has become the focal point for industry-led work on tokenized fund and asset infrastructure. Each of these moves signals the same thing: the firms positioning themselves for the next decade are doing the integration work now, not waiting for a starting gun that has already sounded.

Our Tokenisation Readiness Framework

We're not pretending to have a tokenized model portfolio ready to ship tomorrow. Like the rest of the industry, we are preparing and the honest position is that the firms doing this seriously will publish their thinking before they publish their product. What we are committing to publicly is the framework our preparation follows: three pillars we believe will define the operating model the tokenized era demands.

· Unified Truth. Seamless synchronization between platform records and the digital register, with a clear hierarchy of authority so there is never ambiguity about which version of reality is canonical.

· Efficient Execution. Automated, transparent dealing workflows that eliminate the black box of traditional settlement, including readiness for the D2F model where appropriate, and the ability to run alongside conventional unit dealing during the transition.

· Proactive Oversight. A governance model where operational, technology, and counterparty risk are managed with the same rigor as market risk, supported by the resilience planning the FCA now expects of firms running on-chain registers.

Building toward these pillars now, rather than retrofitting them later, is the discipline we believe will distinguish the firms that lead the next cycle from those that scramble to catch up.

What This Means for Your Portfolio

Step back from the plumbing for a moment. The truth is that most of this happens out of sight - and frankly, that's the point. The dream of any back-office reform is that the front office never has to think about it. You don't see the register, the smart contract, or the settlement instruction, any more than you see the SWIFT message that moves a bank transfer today. But you do see the consequences.

When you redeem from a tokenized holding, the cash arrives faster and with less risk of administrative delay. When your portfolio is rebalanced, the trades execute and settle on a tighter, more predictable timetable - which means the portfolio you actually own tracks more closely to the portfolio that was designed for you. When markets are under stress, your fund manager works from cleaner, real-time information about flows, rather than from estimates that are hours or days old.

Over time, the savings from reduced reconciliation work, fewer failed trades, and lower cash buffers don't stay locked inside the operations function. They flow through to the things that matter to a long-term investor: tighter tracking, lower frictional cost, and a clearer line of sight between what your statement says and what you own.

None of this changes the investment thesis behind your portfolio. The asset allocation, the manager selection, the long-term plan - those are unchanged. What changes is the confidence with which that plan is executed on your behalf.

The Dividing Line

The industry is dividing between those clinging to inherited, manual infrastructure and those embracing the efficiency of the digital age. Tokenization is the catalyst, providing the transparency and speed that modern investors - and increasingly, modern regulators - expect. The firms that will lead the next cycle aren't those waiting for the technology to mature, and they aren't those rushing to claim it before they've built it properly. The technology has matured. The regulatory framework has arrived. What remains is the operational discipline to use both - and that's the work we're doing now.

Allan Lane, www.algo-chain.com

Events on our radar

DigiAssets Connect Zurich, 16-17 June - Custody, banking, and institutional infrastructure – tickets HERE

European Blockchain Convention 12, Europe’s Deal Floor for Digital Assets. BARCELONA · 16-17 SEPTEMBER 2026 - tickets HERE