Welcome to the weekly letter (#22) from TheIntersection team. Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: More cyber security breaches

- Data: Apollo on surging volumes

- Analysis: Tokenization - redefining City culture

- Opinion: Guernsey structures the next trillion

- Our weekly events round-up

And it's all free! Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

News in Brief

Robinhood Launches "Robinhood Chain": At its keynote at a London event, Robinhood officially launched its public mainnet Layer 2 blockchain built on Arbitrum. Dubbed Robinhood Chain, the network blends retail finance with a dedicated DeFi suite, partnering with Uniswap to offer 24/7 tokenized asset trading.

Summer.fi Hit for $6 Million: On the security front, yield optimization protocol Summer.fi (formerly Oasis.app) fell victim to a flash loan attack. The exploiter manipulated the protocol's share accounting logic via the totalAssets() function, briefly sending a vault's displayed APY to an absurd 2,080,000% before draining $6 million in DAI.

The Summer.fi exploit capped off a sobering milestone. Total DeFi sector losses from cyberattacks and exploits have now breached $840 million. Analysts reckon that hackers are moving away from simple smart contract bugs and are instead deploying advanced social engineering, RPC poisoning, and governance-takeover strategies to drain protocols.

The "Open USD" Alliance Launches: A massive coalition of more than 140 finance, tech, and crypto heavyweights (including Visa, Mastercard, Stripe, BlackRock, Google, and Shopify) announced Open USD (OUSD). The initiative aims to allow enterprises to mint and redeem stablecoins without volume limits or fees.

DTCC Moves to Live Production: The Depository Trust & Clearing Corporation (DTCC) confirmed it is facilitating initial, limited production trades for its new tokenization service this month (July 2026), ahead of a full commercial launch in October.

The FCA published its final crypto rulebook: On 30 June the FCA published its final policy statements for the UK cryptoasset regime, covering stablecoin capital, backing assets, redemption, interest, global liquidity pools, DeFi and market abuse.

The headline concession: the capital requirement (the K-SII factor) was cut from 2% to 1% of issuance, with a permanent minimum capital floor of £350k for stablecoin issuers. The authorisation gateway opens 30 September 2026, firms can apply until 28 February 2027, and the mandatory regime comes into force on 25 October 2027. Sterling stablecoins stay with the FCA while systemic issuers fall to the Bank of England, and notably the FCA will consult later this year on DeFi guidance and on operational resilience for firms using DLT.

Quick-fire data points

Surging Aggregates push past $43bn: Recent reports from bank Bernstein and data house KuCoin indicate the total tokenised RWA market capitalisation has climbed past $43 billion and is pushing toward $51 billion depending on the tracked asset index—a big increase from early 2024. Major asset managers continue to dominate. Franklin Templeton’s BENJI fund is now active across nine blockchains, and Circle's USYC tokenised Treasury product has scaled to approximately $3 billion in assets under management (AUM), rivalling BlackRock's BUIDL fund for top market share in on-chain treasuries.

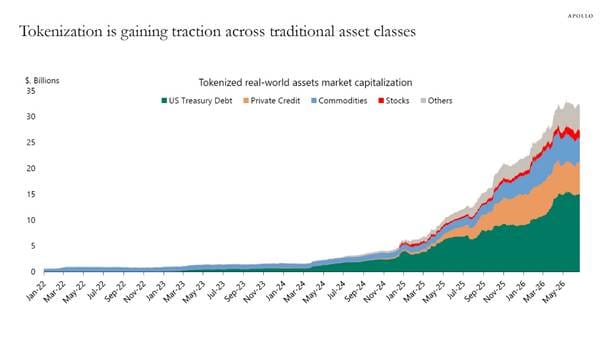

Total value hits $32 billion according to Apollo. According to Apollo’s Torsten Slok, tokenised real-world asset market has grown to nearly $32 billion, highlighting increasing institutional adoption of blockchain-based asset infrastructure. US Treasuries (47%) and private credit (19%) account for approximately 66% of the market, emerging as the dominant use cases for asset tokenisation. Listen to Slok's colleague Christine Moy talk about how tokenisation is shaping the future of investing and private markets on this podcast here, and read her paper here.

Stablecoins shattering records in June: According to Visa’s stablecoin analytics dashboard, adjusted stablecoin transaction volume hit an all-time record of $1.79 trillion in June, a 63% jump from May. While Tether (USDT) remains the largest by market cap, Circle’s USDC captured the lion's share of activity, accounting for roughly 67% ($1.21 trillion) of the monthly transaction volume. For the first time, Coinbase's Layer 2 network, Base, became the most-used network for stablecoin transactions, with $565 billion, just barely edging out the Ethereum mainnet ($562 billion).

The wrapper phase still dominates. A widely discussed Pantera report finds around 78% of tokenized assets are still in a “wrapper” phase (effectively blockchain receipts for assets that operate primarily off‑chain) suggesting most projects have yet to harness composability, instant settlement or programmable cash flows. Stablecoins still dominate the broader tokenization universe, making up over 90% of total market value in Pantera’s dataset, which reinforces that RWAs are meaningful but still small relative to tokenized money.

Solana pulls ahead. Solana's tokenised RWA ecosystem hit a fresh all-time high of $3.41 billion, while overall stablecoin supply actually dropped to $312 billion in Q2, with transaction counts and organic transfer volume also declining.

Tokenization: redefining City culture

by Damien Black

If tokenisation digitises everything, what happens to the culture of finance? The Square Mile in London and Wall Street in New York have become legendary hubs of fiscal activity – the Intersection asks if the shift towards DeFi might diminish their status.

Everyone above a certain age remembers what happened to Fleet Street. Once the hub of print journalism in the UK, the ancient London road that runs parallel to the Thames lost its centre of gravity when the trade digitized in the 1990s. Of course, newspapers themselves didn’t disappear overnight (it would take social media a generation later to deal the death blow), but the culture changed as the industry became more diffuse. Nowadays, Fleet Street might be taken as a byword for nostalgia – gone are the halcyon days when career journalists worked, drank and debated on a single street.

I’ve been wondering if the same thing could happen to the Square Mile and Wall Street if tokenisation continues apace – if trading happens onchain, you don’t need to be physically near an exchange. Middlemen and clearing houses are already under threat. Custodians and market makers can now be remote, with tokens trading 24/7 online. Does this threaten the culture of doing business that has developed in key cities like London and New York?

‘We’re upgrading the culture’

Mitchell Williams worked on Wall Street for twenty years before joining Streamex, a company that specializes in tokenization.

"Having spent over two decades on Wall Street analyzing the financial impact of change, I can say the comparison to Fleet Street is remarkably apt,” he tells me. “Tokenization and on-chain trading are dismantling the structural necessity of traditional hubs like the Square Mile or Wall Street. When assets trade 24/7 online – like our GLDY token at Streamex – and middlemen operate remotely, the gravitational pull of legacy infrastructure disappears.”

This has certainly ruffled feathers among some of his former colleagues, who genuinely fear a loss of culture and nurture “an undeniable nostalgia for the chaotic density of traditional finance”. Williams and his cohort in the digital asset space, on the other hand, are rather more upbeat. “We view this not as a loss, but as an evolution. We aren’t abandoning culture – we are upgrading it.”

Though DeFi eliminates the need to be physically tethered to an exchange, he tells me, the human beings at the heart of tokenized trading still rely on face-to-face teamwork to get things done. “Instead of being forced into high-stress, high-cost epicentres, talent is migrating,” he says. “Firms are unlocking value by building local density in regions offering a superior quality of life and lower cost of living.”

He cites his own new employer, Streamex, based in Winter Park, Florida, as an example. Located near Orlando, it is a far cry from New York’s concrete jungle, boasting what he describes as “canopy-draped green spaces”. It has top-notch schools, and from what Williams says, the nightlife seems to revolve more around fine dining (think Michelin-starred restaurants) than boozy pub crawls. Streamex shares this idyllic space with the likes of BNY Mellon and Robinhood. “New micro-hubs are thriving in places like Winter Park,” says Williams. “We are replacing the gruelling Wall Street grind with first-class infrastructure, proving financial culture doesn’t need a famous street sign to flourish.”

Wall Street’s deal with the devil no longer appeals

Sounds lovely, but come on – bankers migrating from Wall Street to Winter Park? Seriously? “The evidence of top-tier talent migrating to Florida is overwhelming,” Williams insists. “You only have to look at institutions like Citadel leading the charge in Miami to see the macro shift. On a more granular level, the surging home prices and the fierce competition for private school admissions across Florida’s most desirable enclaves are direct metrics of this relocation pressure. Wall Street isn’t just taking notice, they are watching the migration happen in real time.”

Gone are the days when leaving Manhattan meant career suicide, and changing jobs simply meant walking across Wall Street to work in a different building. “The true baseline for comparison is net quality of life,” adds Williams. “I would wager the typical New York transplant is immensely grateful for a minimal commute and a low-stress environment – when nostalgia for that old dynamism hits, a two-hour flight to NYC is an easy fix.”

Lifestyle values and innovation, he tells me, are the new go-tos for finance professionals and not the “traditional prestige or legacy badges of Wall Street elitism”. TradFi’s old-school “brutal bargain” of absorbing the pain of a burnout work culture to get rich is losing its appeal. “Today, top talent has options to build highly meaningful and financially rewarding careers without accepting the trade-offs of Wall Street,” says Williams. “It simply means fewer people are willing to take them up on that bargain.”

I once visited a Wall Street bar and noticed a bunch of ties hanging up behind the counter. When I asked my partner what this signified she told me it was a sort of tradition – stressed-out Wall Street pros would hit the bar straight after work, taking off their ties, get loaded and leave them behind. It was a sort of informal tradition. Any similar defining quirks to be found at Winter Park?

“I think the defining ‘quirk’ of Winter Park is simply happier professionals,” says Williams. “When you eliminate soul-crushing commutes and the anxiety of exorbitant property values, you fundamentally restore a person’s quality of life. The culture we are building in DeFi is less about late-night, aggressive bar-hopping and more centred around high-quality coffee meetups and phenomenal dining. The celebrations look different here because the baseline stress level is much lower.”

‘Culture doesn’t die when geography stops mattering’

Eric Wade is another professional who made the jump from TradFi to DeFi. Formerly an executive at Merrill Lynch, he is now editor of Crypto Capital at Stansberry Research, the flagship firm for MarketWise. As well as covering tokenization, he also mines Bitcoin. From shuffling papers at Lynch to covering the cutting edge of digital money, he’s been on the whole ride.

He agrees with me that fears of a culture change in London and New York are real and that the Fleet Street analogy is on point. Well, up to a point. “Tokenization dissolves the reason to stand next to an exchange, and the culture built on that proximity thins out the way Fleet Street did. But diminished is the wrong word. Culture doesn’t die when geography stops mattering. It relocates, and it usually comes back bigger. The only people who should be frightened are the ones whose single asset was their address.”

Wade cites the demise of the trading pits in Wall Street when everything moved onto digital terminals a few decades ago. “When trading moves on-chain, the reason to be within a mile of an exchange evaporates,” he says. “The open-outcry pit was the loudest, most physical finance culture ever built, all coloured jackets and hand signals and shouting, and electronic trading decimated it, but the culture didn’t die. It moved to screens, then to terminals, and lately to a group chat.”

So not killed off then, more like… modified.

Tokenization is good news for London

“Fleet Street is the sharper parallel, and it cuts the opposite way from the fear,” says Wade. “When the presses left, the concentration ended. But journalism went global, 24/7, and handed a printing press to anyone with a device. Granted, you can argue that’s both good and bad, right?” Tokenization, he argues, does the same thing to finance: it takes a culture that used to live on a single square mile “and lets it live not anywhere but everywhere”. “Cities, then, have an opportunity to attract minds who could be anywhere they want to be,” he concludes. This is not hypothetical, he insists – and it’s actually good news for London.

Wade points to London company Quant Network, chosen in September 2025 by six of Britain’s largest banks including Barclays, HSBC, Lloyds, and NatWest to build a trial infrastructure for tokenized sterling deposits in the UK across bond settlements, property transactions, and online payments. In June it rolled out a system, Fusion Rollup, that unifies 74 blockchains for institutions. As a result of this project Quant’s token is up more than sixtyfold from its 2018 value ($68.13 at the time of writing) and its holder base has nearly doubled (to more than 167,000) since 2022, says Wade. But the price, he insists, is the least interesting thing about it. “The interesting thing is that the plumbing of tokenized British money is being built in London, by Londoners,” says Wade. “How fascinating would it be if a decentralized-by-default technology created a geographic resurgence?”

It’s a tantalising prospect – a second Square Mile built around DeFi and tokenization, based on clear regulation and affordable energy (London might have a ways to go before it qualifies on the latter metric, though I didn’t have the heart to point that out to him). “It’s a real storm,” concedes Wade when I ask him if the DeFi fears on Wall Street and the Square Mile are nothing more than a storm in a teacup. “But it’s a relocation, not a demolition. The trading floor fades, the protocol layer rises to take its place, and the new financial centre turns out to be wherever the rules are clear and the electricity is cheap. I know, because I already live in it. I trade tokenized markets from the Nevada desert at hours when the City is asleep, on the same power I mine Bitcoin with. The Square Mile can be on that map, or a museum on it. That choice, not tokenization, is what decides whether its culture diminishes.”

Structuring the next trillion: Guernsey's framework for tokenised funds

by Liam Murphy

Guernsey's funds regime, regulatory engagement and forthcoming digital finance reforms position the island to support the next generation of tokenised fund products. As digital finance reshapes the financial services industry, interest in tokenised funds products continues to grow. For sponsors, the attraction is clear: tokenisation has the potential to improve operational efficiency, enhance transparency and support new models of investor access and transferability. For any sponsor evaluating where to domicile tokenised funds structures, regulatory readiness is critical. Guernsey is well placed in this respect. The Guernsey Financial Services Commission (GFSC) has already confirmed that certain fund tokenisation structures can operate within the existing funds framework, and its Digital Finance Initiative points towards a broader and more flexible regime for tokenised funds, digital custody and related infrastructure. This article explores how Guernsey’s legal and regulatory framework, combined with forthcoming digital finance reforms and access to European professional investors, supports the development of commercially viable tokenised funds.

Guernsey's engaged and collaborative regulator

The GFSC's Innovation Sandbox and Concierge service is a structured pre-application pathway that allows sponsors and their advisers to raise specific regulatory questions (for example, on custody arrangements, wallet-level customer due diligence or smart-contract transfer mechanics) and receive substantive guidance before a decision to launch or seek full regulation is required. For digital finance structures, where the regulatory treatment of a specific mechanism is often genuinely novel, pre-application dialogue of this kind removes substantial friction from the structuring process. The GFSC has also demonstrated a willingness to consider pilot waivers where specific rules designed for traditional instruments are in tension with the technology being deployed. This willingness to engage and collaborate with market participants, combined with authorisation timelines measured in days rather than weeks, is of real value to sponsors. It's also a relevant data point to be borne in mind when choosing between jurisdictions with otherwise comparable legal frameworks. Guernsey's regulatory environment and fund architecture The GFSC's policy statement on fund tokenisation confirmed Guernsey's openness to innovation, noting that a token representing an interest in a collective investment scheme should not amount to a virtual asset for the purposes of the Lending, Credit and Finance (Bailiwick of Guernsey) Law, 2022. This means that a token should, therefore, sit outside Guernsey's VASP legislation, with regulation applying solely to the underlying fund product within Guernsey's existing protection of investors regime, allowing for fund structures to benefit from regulatory clarity. Guernsey's fund vehicle architecture has long offered speed to market, and this remains a priority for the GFSC. Recent updates to Guernsey's Private Investment Fund (PIF) regime, now in its third iteration following a decade of industry-led refinement, permits certain types of funds to be registered within one business day. Qualifying Private Investment Fund (QPIFs) geared for sophisticated qualifying investors provide an appropriately regulated product with proportionate regulation calibrated to that investor base. Further alignment with tokenisation is achieved by the 2025 removal of the cap on numbers of investors that may be admitted to a QPIF, permitting potentially unlimited token holders to invest in a product.

Read more about the GFSC's updated PIF framework in our earlier briefing: Guernsey Private Investment Funds: 2025 updates.

The PIF's regulatory simplicity, combined with the jurisdiction's innovative legal structuring options provide an efficient chassis for the tokenisation of fund products in a variety of configurations to reflect a wide range of commercial requirements. Complex mechanics of digital issuance (segregated series, ring-fenced cells, multiple classes of token representing discrete pools of assets) can be reflected cleanly at the vehicle level, for example by using protected cell or incorporated cell companies to segregate token classes and / or asset pools rather than relying on purely contractual arrangements. This structural flexibility can deliver a full range of on-chain products allowing sponsors to create a full range of effective legally robust bespoke structures. Guernsey’s regulatory framework is not limited to institutional grade investors: we retain the full spectrum of authorised and registered closed-ended and open-ended fund structures, offering sponsors the flexibility to match structure to investor base, liquidity profile and distribution strategy.

Incoming updates

The GFSC's Digital Finance Consultation Paper, which closed to responses on 6 March 2026, proposes a broader regulatory framework covering fund tokenisation, stablecoins, digital asset custody and a streamlined approach to retail VASPs. This points to a positive future in this space for Guernsey. The Commission proposes that a tokenised security, bond, derivative or other "Category 2 controlled investment" will remain regulated under Guernsey's investment law in the same way as the underlying asset. It also indicates an intention to permit tokenisation of Guernsey funds on public blockchains rather than limiting them to private chains, subject to appropriate controls such as, for example, smart-contract-level transfer restrictions for eligible, CDD-cleared investors.

In our view, the scope of the consultation is, in places, wider than parallel developments elsewhere and intended to deliver a fully considered regulatory regime. We anticipate that the new framework will support fund tokenisation, digital asset custody and stablecoin issuance within a coherent, regulatory framework. Following the closure of the consultation, the GFSC's recently published feedback paper shows an early sign of the direction of travel. The paper announces changes to the jurisdiction's anti-money laundering handbook intended to support the effective use of technology by the market, demonstrating Guernsey's comprehensive approach to facilitating digital finance.

Access to investors

Guernsey funds access the European professional investor market through the national private placement regimes (NPPR) in any target member state. This matters for sponsors whose investor base includes European institutional capital, such as pension funds, insurers and family offices structured through EU fund vehicles. It is a feature of the Guernsey offering that many competitor offshore jurisdictions cannot replicate: for a tokenised fund intended to be marketed into Europe, this could be critical. When taken together with the Bailiwick's regulatory and legal infrastructure, the depth of our fund administration and legal community and the concentration of specialist digital finance practitioners across the island's advisory firms, the case for Guernsey as a tokenised fund structure domicile is compelling.

What's next?

The regulatory and legal infrastructure to support commercially effective tokenisation of funds in Guernsey is already largely in place. We eagerly await the GFSC's further updates on responses to the Digital Finance Consultation, expected soon, and are confident this initiative will deliver further regulatory clarity for market participants and build on the positive direction of travel for digital finance in Guernsey. Sponsors and their advisers evaluating where to domicile tokenised private capital structures should be engaging with Guernsey-based counsel and fund administrators now, ahead of the next wave of authorisations.

Events on our radar

- TOKEN2049 Singapore, 7–8 October 2026, Singapore - tickets HERE

- WebX Asia (Tokyo), 13–14 July 2026, Tokyo, Japan - tickets HERE

- Blockchain Futurist Conference (Toronto), 21–22 July 2026, Toronto, Canada - tickets HERE

- European Blockchain Convention 12, Europe’s Deal Floor for Digital Assets. BARCELONA · 16-17 SEPTEMBER 2026 - tickets HERE

- Digital Assets Forum New York, New York 13 November 2026 - tickets HERE