Welcome to the eleventh letter from TheIntersection team. We hope you are enjoying this weekly letter. Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: The success of Securitize

- Data: Gold tokens falter in March

- Analysis: CLARITY and DeFi - a primer

- Our weekly events round-up

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

News in Brief

Tokenisation could unlock SME financing. Tokenising assets like invoices and receivables could help small businesses access faster, more flexible funding, according to the World Economic Forum. By turning these assets into tradable digital tokens, firms can improve cash flow and reduce reliance on traditional bank lending. Why it matters: Tokenisation could help close the global SME financing gap by bringing liquidity to businesses that have historically struggled to access credit.

BlackRock brings tokenised Treasuries into DeFi. BlackRock’s BUIDL fund — now valued at over $2bn — has launched on Uniswap via Securitize, allowing whitelisted institutional investors to trade tokenised U.S. Treasuries directly on-chain with self-custody. The fund has also expanded across multiple blockchains, including Ethereum, Solana and BNB Chain. Why it matters: This is a major step in TradFi–DeFi convergence, showing how regulated yield products are starting to plug directly into decentralised liquidity.

Hong Kong positions itself as a tokenisation hub. The upcoming “RWA & Payments 2026” summit highlights Hong Kong’s ambition to become a leading centre for tokenisation, with a focus on stablecoins, RWAs and blockchain-based payments. The event is backed by major players including Mask Network and AWS. Why it matters: Jurisdictions with clear regulatory frameworks are competing to attract tokenisation infrastructure and capital.

Real-world commodities move on-chain. SMX has launched its Digital Material Passport Platform, enabling the tracking and tokenisation of physical commodities such as steel, rubber and plastics. The system is designed to provide audit-grade data for supply chains and allow materials to be used as digital collateral. Why it matters: Tokenisation is expanding beyond financial assets into industrial and supply-chain use cases — broadening the scope of RWAs.

Deep Dive — How Securitize turned tokenisation into a $4bn business

The Top Line

Securitize shows that tokenisation only scales when it looks less like crypto — and more like traditional market infrastructure.

The Details

For years, tokenisation sat in a holding pattern: widely discussed, rarely deployed at scale. Most projects stopped at pilots or announcements that failed to meaningfully change how markets functioned. Securitize is one of the few platforms to break out of that cycle. According to a recent case study, it has grown into a $4bn+ tokenised asset platform by focusing on institutional use cases, regulatory compliance and real capital flows — not experimentation.

The key difference is positioning. Rather than trying to reinvent finance, Securitize built infrastructure that fits inside it. The platform operates as a regulated issuance and trading venue for digital securities, aligning closely with frameworks like SEC and MiFID requirements across jurisdictions. That “regulation-first” approach turns out to be a feature, not a constraint. Institutions require clear rules around ownership, transferability and custody — and platforms that embed those rules directly into their systems are the ones gaining traction.

The asset mix reinforces that point. Despite the hype around tokenised equities, the majority of demand on Securitize comes from low-risk, yield-bearing instruments, particularly U.S. Treasury-backed products, which account for a significant share of activity. In other words, adoption is being driven by familiar financial products, not novel ones.

There is also a clear business model. The platform has moved beyond one-off issuance fees to build recurring revenue streams tied to administration, compliance and lifecycle management of tokenised assets. Revenues reached over $55m in the first nine months of 2025, with projections pointing toward ~$110m annually. That matters because it shows tokenisation is not just technically viable — it is commercially viable.

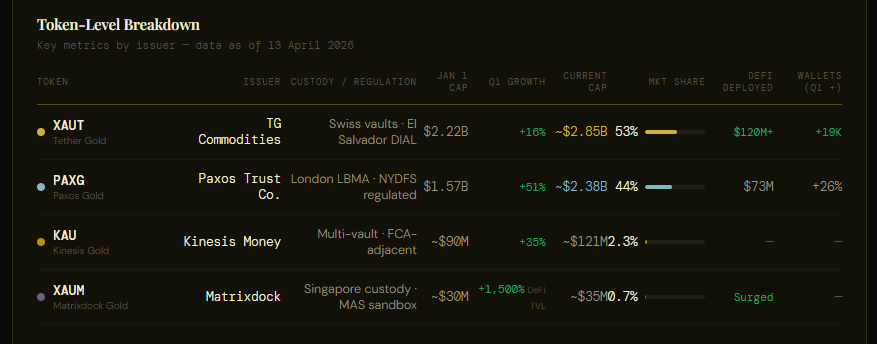

Gold tokens falter in March

The big picture. Tokenised gold ended Q1 2026 at $5.6 billion in market cap, adding $1.3 billion in new value over the quarter — a 30% gain — and the sector grew five times faster than physical gold over the same period. Cex The market cap today stands at $5.37 billion. CoinGecko

The duopoly and its divergence. PAXG had the stronger quarter by market cap, posting a 51% increase and adding more than $800 million in value, while XAUT grew 16%. PAXG entered the year as the smaller of the two and closed Q1 just $200 million behind, down from a gap closer to $650 million. But XAUT's DeFi-deployed value surged 127%, while PAXG's pulled back slightly — PAXG attracting capital that sits, XAUT attracting capital that moves. Cex. In January alone, PAXG saw $248 million in inflows and the tokenised gold market cap surged to $5.8 billion, with trading volumes hitting $178 billion. ChainUp Then in early March, the combined market cap crossed $6 billion as daily trading volumes for both XAUT and PAXG each exceeded $1 billion, driven by the US-Iran conflict and the closure of the Strait of Hormuz — the largest single on-chain movement being a $151 million XAUT delivery from Tether to Abraxas Capital Management. Tokenizer

Market cap correction. The total sector hit $6B+ on 2-3 March during the Iran crisis surge, but has since retreated to $5.37B — a roughly 10-11% decline. The driver is largely the gold price itself, which pulled back from its $5,400+ spike to around $4,556 by early April as geopolitical risk premiums faded.

Whale profit-taking. On-chain data shows whales taking profits, selling around $40M in PAXG and XAUT within 48 hours on 9 March, signalling potential short-term rotation out of tokenised gold and into risk assets. CoinMarketCap That was followed by OKX redemptions in late March — around $15.7M in PAXG and roughly $13.5M in XAUT redeemed by Cumberland Cryptonewsnavigator — a further sign of institutional profit-realisation after the March crisis spike.

Volume growth slowing, but from a high base. The CEX.io Q1 report, published last week, flagged a structural shift worth watching: tokenised gold recorded $82 billion in trading volume in Q1 2026, a 1,300% year-on-year increase, but the growth gap is starting to narrow. Tokenised gold showed its slowest growth over the past year and slipped from the second-largest to the third-largest gold trading instrument by volume in Q1, as traditional instruments saw renewed activity driven by the same macro volatility. Cex This isn't a red flag so much as a normalisation effect as the sector matures toward ETF scale.

New access points. PAXG was listed on Robinhood on 4 February Messari — expanding retail reach into the US mass market — and Bybit is running a PAXGUSDT futures campaign through to 30 April 2026. Messari Also from mid-March, Antalpha netted a $100M gain on a Tether Gold position Cryptonewsnavigator, which drew significant attention to XAUT as an institutional trading vehicle rather than purely a passive store-of-value.

Will CLARITY kill DeFi in the US?

The CLARITY Act is hanging by a thread. Will it ever become law? If it does what would it mean for DeFi?

by John Gray

The Digital Asset Market Clarity Act of 2025, known as the CLARITY Act, could be the most far-reaching piece of legislation on digital assets ever passed in the US, potentially ushering in a new phase in DeFi’s evolution. The bill was first passed by the House of Representatives in July last year, by a bipartisan vote of 294 to 134, and was duly referred to the Senate Committee on Banking, Housing, and Urban Affairs. However, progress quickly stalled amid disputes over key provisions, especially regarding stablecoin yields, and the Act got stuck in legislative limbo.

It’s still there. There’s no set deadline. But if it doesn’t get past the Committee before May, it likely won’t become law before the midterm elections in November. This could result in a ‘back to the drawing board’ situation.

As US Senator Bernie Moreno put it, “If the bill does not reach the full Senate floor by May, digital asset legislation may not receive serious consideration again for years.”

The stakes could not be higher when it comes to DeFi.

“With stablecoins gaining a regulatory foothold, the next frontier is the financial infrastructure they power: tokenized assets, decentralized exchanges and new means of capital formation,” US Treasury Secretary Scott Bessent wrote in an op-ed for the Wall Street Journal on 9 April. “Whether that ecosystem — and its associated jobs and tax revenue — will develop domestically or abroad depends on the durability of U.S. rules.”

CLARITY is the key to that ecosystem flourishing in the US.

Let’s look at what CLARITY is trying to do, why progress has stalled, and what the consequences could be for DeFi if it passes.

What’s wrong with the system as it stands?

When it comes to crypto, the Securities and Exchange Commission (SEC) has traditionally relied on reactive enforcement rather than proactive rule-making. It has leaned on longstanding precedents, primarily SEC v. W.J. Howey Co., which struggle to capture the nuance of modern digital finance. This has led to confusion and outright contradiction.

For example, in the 2023 case, SEC v. Ripple Labs Inc., a federal trial court held that programmatic sales on public exchanges did not constitute securities transactions. However, in SEC v. Terraform Labs Pte. Ltd., another judge in the same district rejected that interpretation.

In short, these are not the conditions under which cryptocurrency, and DeFi more broadly, will be able to mature beyond a volatile, Wild West-ish sort of place, with the SEC playing the sheriff, into the transparent, accessible and dependable ecosystem that it is so ready to become.

What would CLARITY change?

The CLARITY Act is intended to cut through the Gordian knot of outdated precedent and regulatory confusion.

Importantly, it is not really intended to regulate on-chain finance per se.

Speaking on a panel titled ‘What Does the CLARITY Act Mean for DeFi?’ at the Blockworks’ Digital Asset Summit (DAS) on March 26, Greg Xethalis of Multicoin Capital emphasised that CLARITY doesn’t create a regulatory framework for crypto. Rather, it “principally creates a federal regulatory framework for the centralised institutions around crypto.”[1]

It would give such institutions something to rely on, enabling them to interact with DeFi more freely. Key to this is bringing crypto regulation up to the federal level. The Act, as it was approved by the House of Representatives, targeted several broad areas.

First, it would define categories of digital assets in statute, rather than leaving that interpretation to agencies or courts.

Second, it would explicitly assign regulatory authority. The Commodity Futures Trading Commission (CFTC) would have primary oversight of digital commodity markets — including spot trading of assets like bitcoin [BTC] and ether [ETH] — thereby providing a statutory home for many tokens traded on exchanges. The SEC, meanwhile, would continue to oversee tokens that meet clearly defined investment contract criteria, particularly in initial fundraising contexts.

Third, it would establish registration requirements and compliance pathways for exchanges, brokers, and other intermediaries, reducing legal ambiguity.

Fourth, it would allow some tokens to transition from SEC oversight to CFTC oversight as networks mature and decentralize, reflecting how blockchains evolve over time.

Fifth, it would constrain on‑chain protocol yield models and liquidity mechanisms, limiting how certain DeFi activities generate returns in the US context.

Obviously, there’s more – a lot more – to CLARITY, but these are the overarching categories of reform; together, they comprise a statutory rulebook which would admit no ambiguity.

Why the hold-up?

Almost as soon as it went to the Senate, there were signs that the Act’s passage would not be as smooth as some had hoped. In October, Politico reported that the debate around the Act had become acrimonious. A spokesperson for Senate Banking Chair Tim Scott, Jeff Naft, said that the Democrats’ proposal for how to regulate DeFi “was not a legislative offer,” and that “the document was not written in legislative text, included multiple incoherent policy ideas, and was not a good-faith effort to engage on market structure.”

For his part, a spokesperson for Ruben Gallego, the top Democrat on the Senate Banking subcommittee on digital assets, said that “Democrats have shown up ready to work but our Republican counterparts are crashing out.” Elements of the wider sector also have also been vocal. Crypto firms, fronted by Coinbase, want permission for yield-bearing stablecoins plus explicit DeFi safe harbours. In the words of Summer Mersinger, Blockchain Association CEO, “the disappointing proposal outlined by Senate Democrats would effectively ban decentralized finance, wallet development and other applications in the US — an outcome that’s neither workable nor consistent with American innovation.”

Mersinger’s comment encapsulates this key sticking point. Critics argue that the CLARITY Act’s proposed restrictions on stablecoin yield reflect the banking industry’s insistence that crypto platforms which pay yield or interest on stablecoins would deprive them of their core business. The question isn’t whether DeFi needs clarity, but whether the CLARITY Act delivers it in a way that preserves innovation. The bill’s yield restrictions and compliance requirements could channel activity into banks and regulated intermediaries, reshaping DeFi in their favour rather than protecting decentralised innovation.

What’s the current status?

Towards the end of March, it looked like Senators Tillis and Alsobrooks had reached a compromise: banning passive yield on stablecoin balances but permitting activity-based rewards for payments and platform use. Indeed, Senator Cynthia Lummis confirmed at the Chamber of Digital Commerce Blockchain Summit that DeFi provisions had been finalised, and that committee markup would take place in late April, followed by afloor vote in mid-2026.

The problem is that time is extremely limited. The Senate returns from Easter recess on April 13. A single mis-step, one further week of quibbling, and there may well be no chance of CLARITY being passed this or even next year. The consequences of such a failure could be grim for the US crypto space, as Scott Bessent highlighted. Major players may find that the EU’s Markets in Crypto-Assets Regulation framework is a more propitious sphere in which to operate. Equally, Singapore and the UAE boast DeFi regimes which are considered progressive interms of regulatory clarity and institutional friendliness.

So would CLARITY be good or bad for DeFi?

There’s no denying that a lot of people are very excited about CLARITY. If it were passed, it would enable financial institutions to experiment with DeFi without constantly looking over their shoulders, and, as Xethalis put it at DAS, “build some cool shit”. On a similar note, speaking on the same panel, Summer Mersinger underlined that the Act would “accelerate creativity”, letting crypto-native developers “build with certainty”. Nonetheless, the ramifications of the Act as it stands could be negative for the space. It would impose immediate constraints on DeFi’s core mechanics. Restrictions on stablecoin yield would undermine a primary incentive for liquidity provision, reducing total value locked and compressing returns across lending and staking protocols. Front-end operators and developers could face new compliance obligations, accelerating the shift toward geo-fencing US users or migrating activity offshore.

Safe harbour provisions may not sufficiently protect decentralised protocols, increasing legal risk for developers and governance participants. At the same time, tighter integration with the regulated financial system could favour custodial platforms and bank-affiliated intermediaries, crowding out fully crypto-native firms. In practice, critics say, DeFi in the US would become more permissioned, less composable and increasingly intermediated. The sector would preserve some innovation, but on terms that align more closely with traditional financial infrastructure than with the sector’s original design principles. In a word, we’d be looking at the DeFi-cation of TradFi, and the simultaneous TradFi-cation of DeFi.

Check in with The InterSection soon for another update on this seismically important issue.

[1] There’s a video of this very illuminating panel: https://www.youtube.com/watch?v=-x7tbw06uvc

Events on our radar

Bitcoin 2026 – Las Vegas, 27-29 April - premier Bitcoin ecosystem event – tickets HERE

DigiAssets Connect Zurich, 16-17 June - Custody, banking, and institutional infrastructure – tickets HERE