Welcome to the fifth letter from TheIntersection team. We hope you are enjoying this weekly letter. Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: BlackRock + WisdomTree launch tokens

- Data: McKinsey deep dive into stablecoins

- Analysis: Tokenised gilts

- Opinion: Tokenisation eats the physical world

- Our weekly events round-up

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

News in Brief

BlackRock Steps Into DeFi as Tokenised Markets Accelerate

BlackRock has taken a notable step toward decentralised finance by making its tokenised U.S. Treasury fund BUIDL tradable on Uniswap, according to CoinDesk. The move connects one of the world’s largest asset managers directly to DeFi liquidity infrastructure. Why it matters: Bringing a regulated yield product into a DeFi venue signals growing convergence between traditional finance and decentralised liquidity.

1. RWA market growth continues, led by Treasuries and credit: On-chain real-world assets have climbed to roughly $24.8bn, with strong wallet growth driven largely by retail adoption on Solana, while Ethereum continues to dominate institutional value flows. Why it matters: The split between institutional liquidity (Ethereum) and retail adoption (Solana) is becoming a defining feature of tokenised markets.

2. Exchanges push toward 24/7 tokenised trading infrastructure: The New York Stock Exchange (ICE) is exploring a blockchain-based platform for 24/7 trading of tokenised equities and ETFs with on-chain settlement. Why it matters: The focus is shifting from token issuance to continuous trading and faster settlement.

3. Tokenisation expands into specialised real-world assets: Recent deals include a tradable tokenised aviation asset on Ethereum and regulated ship-backed financing in Singapore. Why it matters: Tokenisation is extending beyond financial assets into transport and infrastructure sectors.

4. Blockchain competition intensifies amid regulatory change: Data shows increased competition among Ethereum, Solana and XRP Ledger in RWA tokenisation metrics, while global regulatory frameworks continue evolving. Why it matters: Chain competition and regulatory clarity will shape where institutional capital ultimately settles.

Deep Dive — WisdomTree Pushes Tokenised Funds Toward 24/7 Markets

WisdomTree plans to introduce 24/7 trading and instant settlement for tokenised shares of money market funds, bringing blockchain settlement closer to mainstream fund infrastructure. The Details: Following regulatory approvals, WisdomTree will enable continuous trading for its WisdomTree Treasury Money Market Digital Fund (WTGXX). See the official WisdomTree press release for full details. The initiative allows near-instant settlement using stablecoin rails, reducing settlement delays and improving liquidity management for institutional investors. Trading will initially occur through WisdomTree Securities, with additional broker-dealers potentially joining subject to regulatory approval. The platform also enables continuous dividend accrual using blockchain timestamps, aligning income allocation with actual holding periods. Further Reading

Stablecoin usage growing fast, says McKinsey

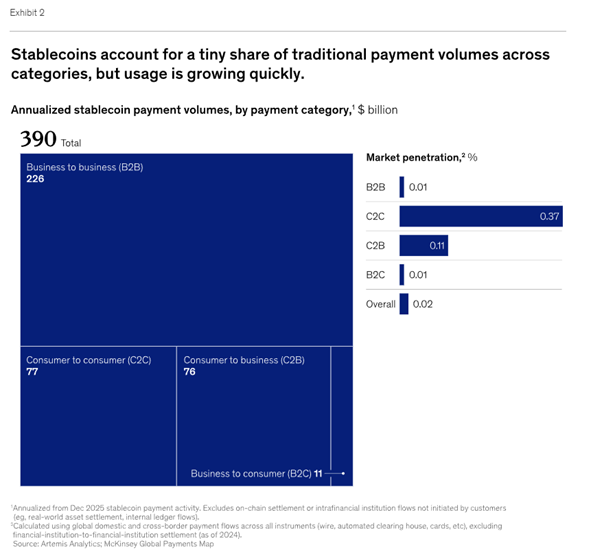

According to a recent paper by management consulting firm McKinsey, the true volume of stablecoin payments is about $390 billion in 2025, more than double from 2024 levels. While stablecoins’ share of total on-chain activity and total payment volume remains relatively small, it reflects real and growing usage in specific contexts (Exhibit 2).

The McKinsey analysis yielded three observations that stand out:

- Value propositions. Stablecoins are gaining traction where they offer advantages in specific use cases, including settlement, improved liquidity management, and reduced friction. For example, international peer-to-peer transfers can be executed nearly instantly and at lower cost compared with some traditional remittance corridors. At the same time, stablecoin-linked cards are expanding practical usability by enabling holders to spend stablecoins directly with merchants globally, without first converting funds through exchanges or banks. We estimate that stablecoin-linked card spending has grown to $4.5 billion in 2025, up 673 percent from 2024.7

- B2B leads growth. B2B payments dominate, accounting for about $226 billion, or roughly 60 percent of global stablecoin payment volume. B2B payments have increased 733 percent year over year, indicating rapid uptake in 2025.

- Asia-originated activity. Activity is uneven across regions and cross-border payment corridors, suggesting that scale will depend on local market structure and constraints. Stablecoin payments sent from Asia represent the largest source of volume, accounting for about $245 billion in payments, or 60 per cent of the total. North America is next, accounting for $95 billion, followed by Europe at $50 billion. Latin America and Africa each accounts for less than $1 billion. Activity today is driven almost entirely by payments sent from Singapore, Hong Kong, and Japan.

Digital gilt: Tokenised, but tamed

by Anna Fedorova

The UK Treasury’s choice of HSBC to facilitate the tokenisation of gilts as part of its Digital Gilt Instrument (DIGIT) pilot is predictable and debatable in equal measure. A 160-year-old bank to lead a strategy whose aim it is to position the UK as a G7 leader in the use of blockchain technology? The choice itself is worth exploring as much as the wider strategy.

The Orion platform, which won the tender process, is HSBC’s proprietary, permissioned digital asset infrastructure specifically designed to issue and settle bonds within the traditional financial framework. It boasts extensive experience working with governments and institutional initiatives, notably a successful green bond issuance in Hong Kong.

The DIGIT project aims to issue short-dated sovereign bonds in tokenised form for the first time within the UK’s Digital Securities Sandbox (DSS). With this move, the Treasury is very much testing the waters – the new bonds will be managed outside of the government’s main debt management programme.

While the tokenised US treasuries market is already $10.84 billion, none of these bonds are issued natively on a blockchain by the US government.

Source: RWA.xyz | Tokenized U.S. Treasuries

Yet its goals are lofty: to be the first G7 country to ever tokenise its sovereign bonds. To be clear, we’ve seen several experiments with corporate bond tokenisation – including Germany’s Siemens, which issued a €60 million digital bond on a public blockchain in 2023.

But, to date, no other nation has issued a digital government bond, so it’s a big deal. Especially at a time when some other nations, notably the United States, are moving rapidly to incorporate digital assets into their financial policies. If successful, this could be a major power signal.

The rules of the game

And that’s exactly why the choice of provider is so critical. It’s not just about how competent or successful they are, but also about how it positions Britain in the global digital asset race.

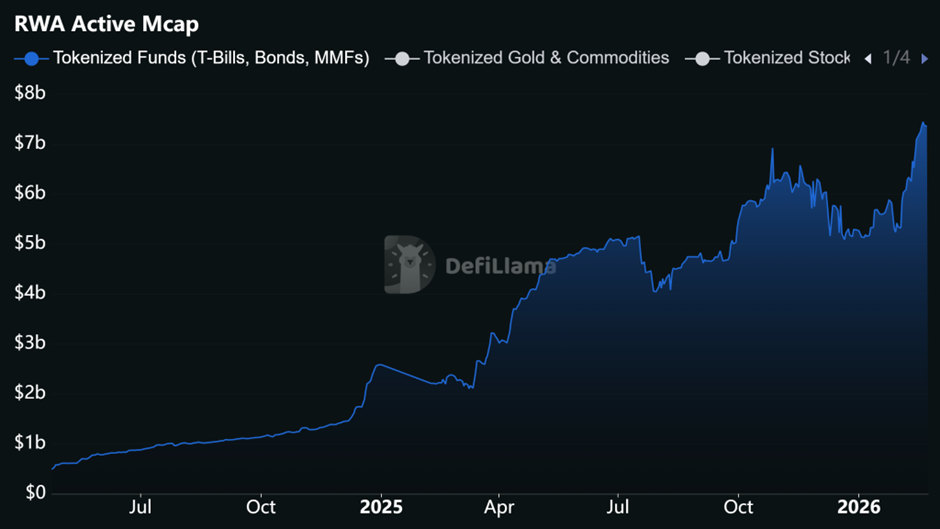

Tokenised funds with exposure to T-bills, bonds and MMFs have grown continuously, with active on-chain market cap now sitting at $7.35 billion

Source: Real World Assets - DefiLlama

HSBC Orion is a cautious choice. Conservative, even. An incumbent with proven acumen, not a novel experiment. Private, permissioned, and operated by one of the world's biggest banks, Orion is an invite-only club that’s fully integrated into the broader institutional settlement process.

Through this platform, HSBC has already facilitated some $3.5 billion worth of “digitally native” bond issuance for entities ranging from the European Investment Bank (EIB) to the Hong Kong government. This proven pedigree, and HSBC’s leading position in the UK’s existing financial infrastructure, remove much of the risk associated with the digital asset sector.

The message is loud and clear: the UK intends to adopt distributed ledger technology (DLT) by integrating it into the existing financial system rather than experimenting outside it.

That is a sober choice – especially at a time when global perception of digital assets is subdued due to the widespread sell-off across Bitcoin and other cryptocurrencies. During times of heightened market risk, optics matter. HSBC may not be a shiny new digital start-up, but perhaps the choice is boring by design.

The move is all the more meaningful in the post-Brexit context, amid concerns over the loss of competitiveness for UK businesses. In particular, financial services exports to the EU have shrunk markedly since Brexit, with the market share of UK financial services in major EU countries falling across the board.

On top of this, recent reporting by the Financial Times suggests that nearly 6,000 entrepreneurs, the majority from the technology sector, have left the UK for pastures new due to sweeping tax changes. Against this backdrop, digital assets become an even more important avenue to re-establish global leadership.

Permissioned versus permissionless

When it comes to government-led blockchain initiatives, there are broadly two distinct tracks forming. On the one hand, the UK seems to be following in Hong Kong’s footsteps by choosing a permissioned blockchain operated by a financial services incumbent. Using the tried-and-tested provider who successfully executed Hong Kong’s digital green bond issuance last year fits this mould.

On the other hand, there is the more experimental style adopted by nations like Singapore. As part of its Project Guardian, which was announced back in May 2022, Singapore and its partner banks – DBS Bank, JPMorgan and SBI Digital Asset Holdings – turned to permissionless blockchains Polygon and Aave.

As early as November 2022, Singapore was already experimenting with cross-currency transactions involving tokenised Japanese yen and Singapore dollar deposits on these open blockchains. At the time, Mr Sopnendu Mohanty, the Monetary Authority of Singapore (MAS) chief fintech officer, said that “digital assets and decentralised finance have the potential to transform capital markets”, but with “appropriate guardrails in place”.

Of course, a permissionless blockchain comes with its own set of concerns – including counterparty, security and data privacy risks. Singapore’s strategy to minimise these is quite clever. It controls access to the sandbox at the onboarding level, so only approved counterparties who have passed KYC and AML checks can participate. It works for now, though this approach is yet to be tested at scale.

Shaping innovation

In contrast, the UK’s digital gilt project seems less about experimenting and more about integrating blockchain technology in a controlled, permissioned environment from the outset. This cautious strategy could, paradoxically, enable the UK to integrate digital assets into its financial ecosystem more quickly by circumventing the regulatory roadblocks associated with experimental technology.

Not only that, but infrastructure developed by a 160-year-old bank will likely inspire far more confidence from an equally well-established financial institution than a bootstrapped crypto project that hasn’t even been around for a decade. It’s the best of both worlds: the speed and efficiency of digital technology alongside institutional-level compliance and trust.

However, there are downsides. With a banking giant like HSBC leading this project, there could be less room for the UK fintech sector to showcase the value it can add to the UK’s DLT initiatives. Less input from crypto-native firms also means potentially missing out on hard-won experience at the bleeding edge of blockchain innovation.

For example, the tightly controlled environment means that composability outside the Orion platform, or access to wider liquidity beyond institutional circles, will likely be limited. In decentralised finance (DeFi), a tokenised gilt could theoretically be used as collateral across the ecosystem, interact with other tokenised assets, or be reused in repo-like structures. In this model, though, the likelihood is it remains within the sandbox.

In addition, permissionless blockchains are often built on open-source code. As a result, innovations and integrations happen faster. HSBC’s Orion is built for pilots like these, but the key question is: how will this scale as digital issuance grows? What if a trillion pounds were to move on-chain?

Is T+0 wishful thinking?

Regardless of the blockchain choice, the main benefit of blockchain technology remains: T+0 settlement. In theory, this could mean instant international transactions. No more 24-hour-plus waits, no more need for interim credit exposure, lower counterparty risk. At least, that’s the theory.

In reality, though, the typical settlement for UK gilts today is T+1. And, indeed, according to last year’s implementation plan from The Accelerated Settlement Taskforce Technical Group, not even T+1 settlement is universal across the UK securities market at present. The document cautioned that “the move to T+0 or Atomic Settlement should not take place until after the move to T+1”.

In a similar vein, the US Securities Industry and Financial Markets Association (SIMFA) has previously warned of the risks of transitioning to T+0 settlement too soon. These include major changes across the operations of market participants such as prime brokers and clearing houses, reduced time for compliance testing, and disruption to global settlement and FX conversions.

The point is that for T+0 settlement to be truly beneficial, the entire financial ecosystem must upgrade. That means repo markets, which are closely linked to the UK sovereign bond market, as well as FX markets, central bank clearing houses and custodial chains.

Regardless of DIGIT’s success, if it remains on a separate settlement rail to the rest of the bond market, the benefits will remain theoretical. In fact, paradoxically, it could add more complexity and introduce more fragmentation into the system – at least for the time being. So the real test isn’t about settling intra-day trades. That’s just the proof of concept. The real test will be when the UK tries to integrate digital bonds into the existing financial market.

A part of the system

In practice, the success of the pilot will depend on several factors. Once the issuance details are announced, subscription levels and investor breakdown will tell us a lot about the real interest in this project. Solid trading volumes and tight bid-offer spreads with other short-dated gilts would be a positive sign.

But this will also depend on how easy it is for institutions to hold DIGIT via standard custodial chains such as Euroclear and Clearstream. Is there a clear path toward integrating digital bonds with CREST and traditional settlement infrastructure? Or will they exist in a complete silo? Any form of friction could reduce uptake. What matters more than any of this, though, is whether the new digital bond will be eligible for use in repo markets on the same terms as other similar gilts. And, if it is accepted by the London Clearing House, other clearing venues, and the Bank of England, how will this work in practice?

Given that the Treasury has said this bond will sit entirely outside other gilt management operations, that may not be the case. And it’s this practical use within the wider market that really matters when it comes to securities. Once again, the real roadblock could be interoperability. And for the UK, which has evidently chosen to integrate digital assets within its existing financial framework rather than build out novel infrastructure, interoperability is even more pertinent. Without this, the pilot risks remaining just that.

Layer Cake

by John Jameson

While you are being sold the benefits of crypto’s decentralised frontend narrative, the System of the World is being reengineered. But, behind the scenes, the backend is forcing physical assets into a mechanism of centralised control.

It’s the little things. A statement here, a press release there, the geeks focusing on the tech and their brave new world. But all the while it is getting smaller, the sides compacting in. Monopolies are eating the world. A 1980s banquet that has not lost its appetite. The events you see in the news, the movies and TV shows you consume, the novels you read, the podcasts you listen to, and the social media feeds that curate it all. They influence your opinions about everything.

But monopolisation of the media and popular culture isn’t an isolated case. Over the last 30 years, around the same time politicians began rebranding themselves as leaders, real power shifted from elected politicians to unelected experts. Quangos in the UK, regulatory agencies in the US, now draft and enforce the rules that govern your life, with little democratic oversight.

Politicians pass bills that are vague frameworks. In the UK, they pass through the Commons and the Lords. In the US, through Congress and the Senate. Royal Assent or a presidential signature turns them into a blank cheque with unlimited delegated power inside. That cheque gets handed to technocrats. They fill in the details. Pollution limits, drug approvals, broadcast standards, and these are laid before Parliament or published in the Federal Register. Not for approval. Just for notification. They become law automatically unless someone moves to block them. And almost no one ever does.

But the technocrats didn't seize control. They acquired it, quietly, over decades. Elected politicians realised they were too constrained by voter pressure, always spending too much, always promising too much. So they changed tactics. They began to build more politically efficient systems that removed them from the results of their policies. This new style of politics released a free market ideology. Deregulated businesses, tax cuts, and relaxed antitrust legislation. They called it Reagonomics. Companies merged and acquired. And another domain began to consolidate around the accumulation of wealth and power.

Today, the US stock market is not controlled by the handful of companies that dominate the index weightings. That’s the narrative the media wants you to believe. It's controlled instead by just three that collectively control trillions of dollars of assets, and this means, through their circular ownership via ETFs, they influence a market cap that is around the GDP of the entire United States of America.

BlackRock, Vanguard, and State Street, the Three, have an invisible touch that controls nearly 80% of all passively indexed money inside the US. Passive investing is now the dominant form of equity investment, and this means, when you are betting against the direction of the US stock market, you are, in fact, betting against the collective power of three mega-corporations.

Monopolisation is all around you, affecting every aspect of your life. Subtle for now, invisible to most. But with programmable money and tokenised real-world assets, monopolisation will shift from affecting to effecting every aspect of your life. Directly, inescapably, everywhere. Everything is connected. Around the same time the new political strategy began to open markets, TCP/IP was formalised as the internetwork standard. PCs were connected to mainframes. The first browser. Lycos. Amazon. Google. Then came the centralisation of businesses. And then social media. The centralisation of ideas.

And from the centralisation of ideas, came the CEO King. Then along came crypto and Web3.

Its decentralised narrative was being nam-shubbed around the YouTuberSphere, and somewhere in the admittedly demyelinated pathways of my mind, I remembered something Rushdie said in Midnight’s Children. To understand just one life, you have to swallow the world. BlackRock et al have swallowed the stock market. Their ETFs herding a market of stocks into what is effectively a centralised monopoly. My number one tool for finding ideas isn’t a chart. A price history can never give you a reason, though it can be useful as a trigger. And it’s not fundamentals either. Wall Street valuations run on earnings and discounted cash flows. That’s like blaming the effect on the effect. The tool I use more than any other is the counterfactual. I use them to find background conditions. No idea is stupid. Anything goes; nothing is off-limits.

What if you wanted to build a global network, one capable of recording every tagged metadata interaction ever created, how would you do it and what about the cost. To design, test, scale, and secure the architecture, and to persuade the public to use it, would cost hundreds of billions of dollars.

What if, instead of spending that money, you anonymously released an open-source protocol and a simple algorithm, and let the free market, with light-touch regulation, do the rest? Bitcoin. What if non-fungible tokens, NFTs, were an R&D test project, a proof of concept to determine whether digital ownership could be scaled using a decentralised network, a blockchain? Most counterfactuals will take you nowhere, but occasionally, every once in a while, they uncover gold.

What if crypto and its decentralised platforms swallow the world? The Genesis Act was passed into US law on July 18th, 2025, and creates the federal framework for payment stablecoins. The Clarity Act passed the House of Representatives in 2024 and is expected to be finalised in 2026. It defines a clear distinction between stablecoins and securities. It states that a stablecoin backed 100% by cash and US T-bills is not a security.

These two acts unlock institutional adoption and enable a new form of liquidity. This matters because for the first time deep US dollar liquidity will be generated from the atomisation of demand. From billions of small US dollar transactions aggregated into permanent demand. Demand that is backed and controlled 100% by the United States. Today, the total market capitalisation of the stablecoin market is around $300 billion.

What if over the next decade, the stablecoin market is expanded to $6 trillion? Given the global demand for US dollars, I think that’s possible. But if that happens it will centralise control of the bond market into the hands of a few companies. Like BlackRock and the monopolising of the stock market.

But everything needs a reason to exist. Stablecoins do not issue credit. And that means Basel III does not apply to them. They are tokenised claims backed one-to-one by US T-bills. Because they tokenise existing dollars rather than create new ones, they are non-inflationary and do not expand the banking system’s balance sheet. That right there is reason enough.

What the geeks forget when playing with their shiny new tokenisation technology, is while theirs is a brave new world on the front end, an old school centralised control system will control the backend. A company creates a legal wrapper, an LLC, an SPV, or a trust. And that vehicle buys the real-world asset, whatever it may be.

Financial assets like sovereign and corporate debt, private loans, public stocks, and private company shares, real physical assets like residential and commercial real estate, farmland, gold, and silver. The tokenisation of hard financial assets and real physical assets is already happening. Next will be royalties, music, film, and book, intellectual property, licensing rights and trademarks, carbon credits, emission allowances and offsets, and infrastructure usage licences. Real World Asset tokenisation will eat the world. It will centralise everything. Tangibles first. Then intangibles.

But the centralised wrapper entity owns the asset. The legal rights defined in contracts. A token represents fractional equity in that entity or debt claim, or revenue stream. And as tokenisation eats the world, you will be pushed further down the layer cake, abstracted away from the physical asset programmatically enforced from inside a smart contract running on a blockchain.

Causal chains running across time, mediating, confounding, colliding. You are probably holding a node of one of those chains as you read this. The oblong in your hand is being miniaturised. Watches, earbuds, eyeglasses. Devices designed to do only one thing. Increase your number of interactions per second with the System of the World. Every click. Every search. Every location. Every purchase. Every pause. Every scroll. Every swipe. The ontological substrate of you, written permanently to servers you will never see. But in an act of pure irony, the more decentralised society becomes, the more it will be controlled.

And as engineers espouse the benefits of this crypto protocol over that, of this token over another, rubbing their hands at the brilliance of the design, how Cardano’s separation of its ADA token from its Plutus-driven smart contracts makes it more computationally efficient than Ethereum, the space behind them nudged in. Just a little. Just beyond their level of perception. Most crypto speculators focus on decentralisation. They are looking in the wrong place.

John Jameson publishes a Substack called Pretty Bang Bang

Events on our radar:

- Digital Assets Forum Abu Dhabi launches on 13 May 2026, bringing together banks, asset managers, regulators, and digital asset leaders to discuss tokenisation, market infrastructure, and institutional adoption across the Middle East and global capital markets - tickets HERE

- Bitcoin 2026 – Las Vegas, 27-29 April - premier Bitcoin ecosystem event – tickets HERE

- DigiAssets Connect Zurich, 16-17 June - Custody, banking, and institutional infrastructure – tickets HERE