Welcome to the second letter from TheIntersection team.

Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

Every week, subscribers will receive bite-sized news, thought-provoking analysis, insightful data and controversial opinions from an experienced team of investment writers and industry observers, asking all the questions you’d expect from market veterans.

In this issue:

- News: RWA tokens institutionalize

- Analysis: HSBC bets big on tokens

- Data: Stablecoins and their impact on EM banks

- Opinion: What If Tokenisation Isn’t Optional?

- Our weekly events roundup

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

Need to know:Going institutional

The real-world asset (RWA) market is entering 2026 with clear signs of institutionalisation. On-chain RWA value has surpassed $21bn, driven by repeat issuance of tokenised U.S. Treasuries, gold and other cash-like instruments rather than one-off pilots. At the same time, derivatives venues are expanding synthetic RWA exposure through perpetual futures, allowing traders and institutions to gain commodity, equity and macro exposure without directly holding tokenised assets.

The focus is also shifting to settlement and infrastructure upgrades. Same-day (T+0) settlement is increasingly framed as an “invisible upgrade” that could make tokenised securities economically compelling by freeing collateral, reducing counterparty risk and compressing post-trade costs. Deloitte’s 2026 outlook places tokenised securities and stablecoins at the centre of this transition. Taken together, the trend suggests tokenisation is moving beyond experimentation and toward selective, utility-driven deployment — where assets are tokenised not because they can be, but because doing so meaningfully improves liquidity, efficiency or access.

🔗 Further reading: https://cryptorank.io/news/feed/25dc8-plume-blockchain-rwa-2026-roadmap

News in Brief

1. Tokenised Treasuries exceed $10bn. Circle’s USYC and BlackRock/Securitize’s BUIDL each sit near $1.7bn in assets, while Ondo’s USDY surged 16% week-on-week to roughly $1.5bn. Importantly, Ethena is now using BUIDL as backing for its USDtb stablecoin, tightening the link between tokenised government debt and on-chain money.

Why it matters: Treasuries are emerging as the system’s default on-chain cash equivalent, anchoring both yield and stablecoin credibility.

2. Tokenised equities near $1bn. Securitize plans to launch SEC-registered, natively tokenised public stocks in Q1 2026, moving beyond synthetic wrappers. Ondo Global Markets remains the largest issuer, while Kraken, following its acquisition of Backed Finance, is scaling tokenised equities on Solana with sub-second finality.

Why it matters: Public equities are beginning to migrate onto regulated on-chain rails, enabling faster settlement and potentially continuous trading.

3. Regulation and banks step in. MiCA is now enforceable across the EU, giving legal certainty to issuers and custodians, while Riyad Bank (Jeel) and Ripple are testing blockchain-based settlement through a Saudi regulatory sandbox.

Why it matters: Regulatory clarity and bank participation reduce execution risk for institutions considering live RWA deployment.

No token efforts: HSBC bets big

By Damien Black

HSBC has made big strides in the tokenization market since its 2022 launch of Orion, an in-house platform for issuing digital bonds. Two years later, it introduced a gold token and digital asset custody for institutional investors, and it now facilitates tokenised domestic and cross-border payments.

Launched in 2025, HSBC’s tokenized deposit service promises “a new standard in digital money, combining speed with blockchain, and the security and reliability of a global bank”. More prosaically, it offers instant cross-border payments with real-time transaction transparency. The service is live in Hong Kong, Luxembourg, Singapore and the UK and supports sterling, dollar and euro transactions.

The watershed moment came in September, when HSBC used the service to complete its first US dollar-denominated transaction between Hong Kong and Singapore. Its first customer was Ant International, a digital payments company that prides itself on being at the cutting edge of financial technology. “The service addresses the growing demand for instant, cross-border settlement by providing an always-on, blockchain-based platform, whilst supporting the rise of digital money and meeting clients’ evolving needs,” Financial IT reported at the time.

Tokenized deposits vs. cryptocurrency

One important distinction to make before we go any further. Tokenized deposits are not stablecoins. Whereas the latter are digital currencies pegged to traditional fiat currencies such as the dollar and typically backed by assets such as government bonds, deposit tokens are created on the issuer’s balance sheet and issued on the blockchain.

What this means in practical terms is instantaneous transfers backed by regulation, with the issuing bank assuming liability for any claims. And because they are issued by banks, tokenized deposits can also give interest payouts – something stablecoin issuers like Circle and Tether are currently banned from doing in the US, UK and EU.

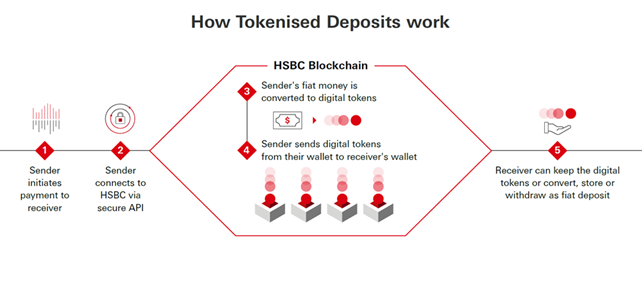

How do they work? In HSBC’s own words, a sender initiates a payment via the bank. The HSBC blockchain then converts the fiat payment into digital tokensand sends them to the intended recipient’s wallet. The recipient can then keep the money in digital token form in their wallet, or convert it to fiat to be stored or withdrawn as they wish.

Tokenised deposits at a glance, courtesy of HSBC

Tokens are good as gold

HSBC’s journey into tokenization has seen it pass several salutary milestones. In November, its Gold Token passed the $1 billion mark, indicating rising demand for tokenized versions of real-world assets (RWA) as banks scramble to get in on the action. HSBC boasts it is “the first bank in the world to offer tokenised ownership of physical gold, unlocking new possibilities in the precious metals market”. It’s available to institutional investors in the UK and their smaller retail counterparts in Hong Kong. John O’Neill, HSBC boss of digital assets and currencies, told the Hong Kong FinTech Week that the token had facilitated more than 100,000 transactions since its launch in March 2024. Gold and tokenization, it would appear, are a match made in financial heaven.

Green shoots look promising

If gold is a good fit for tokens, so is green. That same month, HKMA announced “another milestone on the HKSAR Government’s bond tokenisation journey” with the issuance of HK$10 billion in digital green bonds. The transaction was denominated in Hong Kong dollars, US dollars, the renminbi, and euros.

“For both the HKD and RMB tranches, the option to settle via tokenised central bank money was introduced alongside traditional settlement rails in the primary issuance process, which helped further reduce settlement time, costs and counterparty credit risk,” said HKMA. The platform underpinning the transaction? HSBC Orion. Never slow to sing its own praises, the bank claimed the digital bond issuance was the largest to date of its kind.

“This latest digital issuance on HSBC Orion saw world record size and increased participation from institutional investors across various markets, further showcasing the potential of distributed ledger technology to enhance scalability in the bond market,” said David Liao, HSBC co-chief executive for Asia and Middle East.

Not all plain sailing

In case you’re thinking this sounds like a fairy tale, it isn’t. HSBC has faced some pushback on its tokenization journey. And, you guessed it, said pushback is coming from traditional finance (TradFi) operators and most likely regulators, too. In December, HSBC disclosed that a “recent meeting of the Securities and Exchange Commission’s (SEC) Investor Advisory Committee showed divisions on how a potential market for tokenized US equities should be regulated”.

HSBC said representatives of TradFi firms, such as Citadel Securities, had called on the SEC to apply existing regulations to decentralised finance (DeFi) actors, while cryptocurrency players like Coinbase disagreed, insisting that a new framework was necessary. The HSBC analysts who tabled the SEC meeting’s findings went on the record, warning DeFi advocates not to expect an easy time of it. “The likelihood that the SEC will allow a token securities trading market subject to laxer standards than existing exchanges is low,” they said, concluding that the SEC would most likely insist on a market structure based on a permissioned blockchain.

A permissioned blockchain is a private, closed network accessible only to authorised users and typically requires identity verification. This offers greater scalability and control, making it ideal for enterprise-level investors, but it compromises the blockchain’s original ethos of peer-to-peer transparency. Come on, tech bros, you didn’t seriously expect Uncle Sam to let you off that easily did you?

HSBC remains unfazed by the disputes. Though TradFi, DeFi and regulators may have their differences, the bank remains confident that all three broadly agree that tokenization is the way of the future. It plans to expand its cross-border tokenized payments service to the US and UAE by the middle of 2026. It also hopes to create what it calls “autonomous treasuries” that use AI and automation to help manage funds. Details are yet to come, though this would in theory see intelligent machines managing liquidity risk and the like.

HSBC betting big

It’s not surprising to find HSBC so bullish about tokenization. The bank estimates that digital assets will balloon in value over the next fifteen years to reach a staggering $16 trillion by 2040 and says four in ten financial market players already use some form of distributed ledger technology (DLT) or digital assets. Nick Mersh, another tokenization advocate recently interviewed by The Intersection, reckons the value of on-chain assets could hit $10 trillion in the next couple of years.

“The topic of tokenization, stablecoins, digital money and digital currencies has obviously gathered so much momentum,” said Manish Kohli, HSBC’s global head of payments solutions. “We are making big bets in this space.”

You can see why.

EM banks vulnerable to stablecoins

Back in October last year, the Standard Chartered Digital Assets team put out a cracking paper on stablecoins – implications for EM. In it, the bank’s analysts argued that the coming “stablecoin summer” could quietly drain up to USD 1tn of deposits from emerging‑market (EM) banks into USD-backed stablecoins over the next three years, with the impact heavily skewed towards a subset of vulnerable countries. The authors frame stablecoins not just as a crypto sideshow, but as the latest step in a long shift of payments, liquidity and credit from traditional banks to non-bank players.

Stablecoins are part of the broader post‑GFC story: tougher bank regulation pushed risk and innovation into asset managers, fintechs and decentralised networks, and now stablecoins sit at the centre of that new plumbing. Despite the US GENIUS Act banning yield on compliant stablecoins, the report expects the market cap to reach around USD 2tn by the end of 2028, with adoption driven by 24/7 availability, instant settlement, and low costs rather than yield. For banks, the two big headaches are a slow structural decline in deposits and pressure on correspondent banking, payments, and FX revenues, even as integrating stablecoins into their operations could bring efficiency gains in areas such as settlements and treasury.

The really punchy call is on EM. Standard Chartered estimates the current global stablecoin supply at about USD 280bn, and reckons roughly two‑thirds of that is effectively savings in EM – people using stablecoins as a de facto USD bank account because they distrust local banks or currencies and want a clean USD claim. On their projections, EM savings held in stablecoins rise from about USD 173bn today to roughly USD 1.22tn by end‑2028, implying a bit over USD 1tn of deposits leaking out of EM banking systems in just over three years, albeit only about 2% of aggregate deposits in their “high‑risk” cohort.

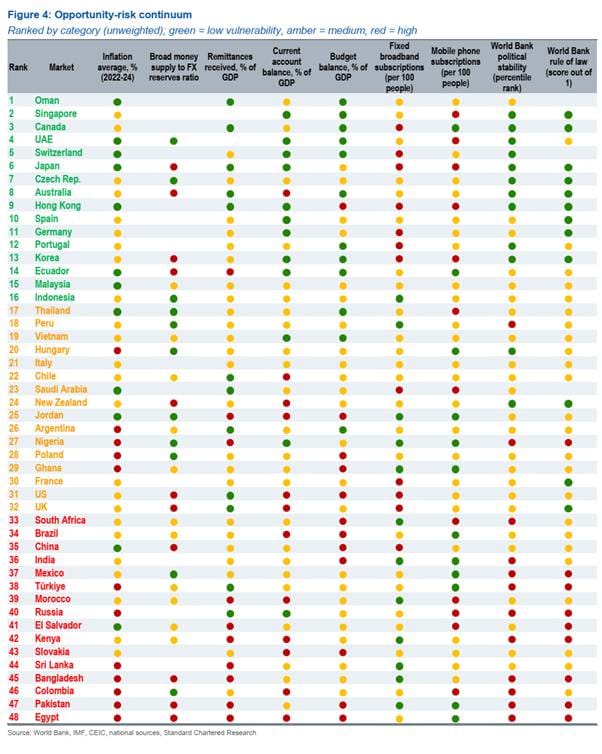

To determine which countries are most exposed, they build an “opportunity‑risk continuum” using nine indicators: inward remittances, inflation, current account and fiscal balances, money-to-FX reserves ratio, broadband and mobile penetration, and two governance measures (political stability and rule of law). They rank 48 markets on each metric, average the rankings, and then group them into low, medium and high vulnerability buckets. On this basis, Egypt, Pakistan, Bangladesh and Sri Lanka stand out as especially at risk of deposit flight into stablecoins, with others like Türkiye, India, China, Brazil, South Africa and Kenya also in the red zone, often characterised by twin deficits or recent balance‑of‑payments stress. At the safer end, countries like Oman, Singapore, Canada, the UAE, and Japan appear relatively insulated, thanks to stronger macroeconomic fundamentals and institutional frameworks.

The authors stress that this is a static snapshot and that policy can change the game. Many EM central banks are exploring CBDCs, pushing digital payment rails (UPI in India, SPEI in Mexico, IMPS in India) and supporting fintechs and mobile money, which both improve inclusion and make the system more competitive versus dollar stablecoins. They also note that macro frameworks in many EMs have quietly improved since the GFC – less aggressive fiscal stimulus post‑COVID, more credible inflation targeting, stronger central‑bank independence and better communication – all of which should help cushion the blow from a stablecoin boom.

For The Intersection, the standout chart is below, Figure 4 – the “opportunity‑risk continuum”. It ranks 48 countries from least to most vulnerable and colour-codes them (green/amber/red) across those nine metrics, so you can instantly see where deposit flight into stablecoins is most likely to bite and where regulators have more breathing room.

What If Tokenisation Isn’t Optional?

By Nik Lysiuk

Nik Lysiuk's work focuses on long-term allocation, ownership and custody, behavioural discipline, and continuity planning. Nik shares practical Bitcoin education through YouTube and social media, where his content has reached over half a million views.https://www.niklysiuk.com/

My to-do list, like yours, is no doubt simultaneously urgent, growing, and stressful to even consider, let alone deal with. So why did I sit in front of the TV last night for 4 hours straight until the clock struck 1 am? Well, because I was glued to a docuseries about the sinking of the Titanic.

Perhaps one’s morbid curiosity clicks up a few levels in January when all is cold, dark and bleak. But more than that, what kept me on edge was the programme’s focus on rigid structures being torn asunder, beyond the horrific and metaphorical sight of the ship itself breaking in two.

The class system across Britain and America in 1912 was deeply embedded across society, but this social construct – where real men were seen as being immune to fear and first class passengers held the moral high ground in every situation – all disappeared at the first real sight of danger.

Anywhere you care to look today – wealth, health, relationships – you’ll see examples of humans simply accepting that the current modus operandi is just fine. Until one day it isn’t. Life is highly contextual and financial markets are no different.

For example, ‘Bitcoin is a Ponzi’, and tokenisation is perhaps orders of magnitude more boring than watching grass grow. Play with context however, and each may go from quite interesting, to absolutely necessary. Just as a breath of fresh air is mindlessly free in this moment, but priceless to poor Benjamin Guggenheim being pulled down to the ocean floor by that unsinkable ship.

‘Bitcoin has no intrinsic value’ if your net worth has already reached a certain point without it, but is highly valuable if you’re a Venezuelan human rights activist trying to avoid assassination attempts, navigate borders and save your country from a leader that builds fabulous wealth while the country and its people collapse into chaos.

The point isn’t that Bitcoin suddenly becomes exciting. It’s that value itself is contextual and often only revealed under pressure.

Closely linked to Bitcoin and blockchain is tokenisation, a concept that may well be mind-numbingly boring if you don’t give a second thought to the timing of when your investments settle or dividend payments clear. Hours, days, weeks – who cares?

Which begs the question, in what context might tokenisation be exciting?

When Larry Fink refers to tokenisation as an overhaul of financial market plumbing, we might have a job on our hands making the concept interesting (apologies to any plumbers who may well find backflow protection systems fascinating). But even plumbing can be exciting in the right context – a flooded basement full of presents on Christmas Eve, for instance.

One problem with tokenisation is that it is inherently boring due to the highly regulated nature of financial markets. The Bitcoin network, for instance, is censorship-free (public), whereas tokenised networks must have participants meet certain entry criteria (and thus be censored) in order to deliver a given quality of service (fees, known counterparties, etc). Adequate regulation is vital in a tokenised world.

So while Bitcoin and tokenisation are related concepts, the latter may never attract cypherpunks intent on changing the world. Perhaps that’s a good thing? But a potential lack of fervour in adoption will not hold tokenisation back because the concept taps into the nature of capitalism itself: the desire to remove cost, friction and dependence on other parties

There are many exciting use cases for tokenisation that ultimately may help protect your portfolio (or company) from AI’s ability to rapidly squeeze margins and accelerate a race to the bottom. When cost cutting becomes a survival technique, tokenisation becomes the lifeboat.

Financial institutions of course abound with examples. The world of investment banking in which I used to live is one that springs to mind, where the need for a persuasion machine across equity research, sales and trading, supported by various middle and back-office functions, collapses when information, price discovery, compliance, and settlement can be embedded in the tokenised asset itself. A report by financial services consultancy firm, Broadridge, estimated that up to 40% of post-trade processing costs could be stripped out by banks using ‘utility models’ to capture economies of scale and network effects.

In fact, any industry with a chain of events that relies on a third party to link provider and user is likely to be capsized by tokenisation. Tokenised property for example, a market where roughly 30% of UK property transactions collapse before completion due to communication breakdowns, could see vast improvement in the costs, speed and efficiency of transactions (not to mention processes across the Land Registry, estate agents, solicitors and insurers).

The Titanic struck an iceberg at 11:40pm, without so much as an ‘I say, what the bally hell was that?’ The incident passed without much notice until she finally plummeted to the depths more than two and a half hours later.

If our current processes are indeed doomed in their current form, the rate at which we are taking on water is slow enough that most people won't notice. But at some point, a mass of people will clock that the passenger-to-lifeboat ratio doesn’t look promising.

Avoiding such panic might be the difference between your portfolio, business, or even your career thriving rather than barely surviving in this new world.