Welcome to the launch letter from TheIntersection team.

Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

Every week, subscribers will receive bite-sized news, thought-provoking analysis, insightful data and controversial opinions from an experienced team of investment writers and industry observers, asking all the questions you’d expect from market veterans.

In this issue:

1. News: NYSE and tokens, Perpetual RWA futures, and equity income token fund launch

2. Analysis: Tokenisation is among the biggest challenges faced by global central banks

3. Data: The big global banks dig into stablecoins, emerging markets, and real-world assets

4. Opinion: Jurgen Blumberg of Centrifuge - When ETFs Meet Tokens

5. How traditional investing is evolving, a podcast with founder, David Stevenson and Nik Lysiuk

6. Our weekly events roundup

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested, and we also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

Need to know: A key trading development highlighted for 2026 is the rise of RWA perpetual futures, which provide synthetic exposure to commodities, equities and macro indices without directly tokenising the underlying, thereby avoiding some custody and operational friction. One derivatives venue reportedly closed 2025 with about 53.1 billion USD in tokenised RWA futures volume, indicating meaningful demand for RWA‑linked leverage and hedging products. Separately, T+0 settlement is being framed as an “invisible upgrade” that could push tokenised securities into the mainstream; Deloitte’s 2026 outlook places same‑day settlement for tokenised securities and stablecoins among the year’s central themes.

News in brief:

1. BNY and DigiFT Launch: In one of the most significant moves for public blockchain adoption, DigiFT (a regulated RWA exchange) partnered with BNY to launch the DigiFT U.S. Equity Income Fund (bEQTY). The first actively managed tokenized U.S. equity income fund on the Ethereum blockchain. Unlike static "wrapped" stocks, this is a professionally managed strategy brought on-chain, signalling that custody giants like BNY are moving beyond stablecoins into complex portfolio management.

2. NYSE 24/7 Blockchain Trading Platform: The New York Stock Exchange (NYSE) confirmed it is building a blockchain-based venue for around-the-clock trading of tokenized stocks and ETFs. This project aims to bring "instant settlement" to the traditional financial world, potentially ending the T+1 or T+2 settlement cycles.

3. Tokenised Stocks Explode on Solana: Solana has emerged as the dominant network for tokenised equities this week, with total Assets Under Management (AUM) in the sector surpassing $1 billion. Backed Finance expanded its offerings to over 60+ "xStocks," allowing global users to trade tokenised versions of Apple, Nvidia, and Microsoft 24/7 with high liquidity. One recent market summary reported that the total on‑chain RWA value is running at roughly 21.35 billion USD, with the number of platforms/issuers increasing from 137 to 140 over the week (about 2.2% growth).

Tokenisation is a big challenge facing central banks

By Michael Hunter

Alongside the international institutions of the international system, the world’s monetary guardians are defining their approach to this latest financial frontier. Detailed preparations for a new era in cross-border payments are underway, covering the ground where global commerce and geopolitics often intersect.

This is the story of how the most influential organisations are preparing for a major digital transformation. There are a variety of strategies in place and under development. Each involves stablecoin-style payments for the transactions at the wholesale level of finance – across borders and between central banks – taking the blockchain beyond retail-level transactions between individual users. The technology, already established and in use for retail stablecoins, could help make cross-border payments faster and cheaper. Such transactions currently depend on the global correspondent banking network. It can be cumbersome, time-consuming and costly. To accept payment, a bank requires an account with an institution within the jurisdiction from where the transaction originates. Without that, a third party is required. This is often a bank where both parties to the transaction have accounts.

Ending the paper wait

This is an aged system, often reliant on paperwork and underpinned by the SWIFT interbank messaging system. Regulatory oversight in each country can delay settlement times. Each transaction can depend on a web of bilateral relations, while being loaded with fees, making the system cumbersome and exposing it to geopolitical turbulence. Tokenisation offers a route around many of these legacy problems with international payments. And it works electronically, dramatically reducing settlement times, even making them instantaneous. All required transactions can be recorded simultaneously in the same blockchain ledger, rather than moving in turn from one jurisdiction to another. Regulatory oversight could also be integrated into the process, significantly speeding it up.

Central banks are aware of the benefits. The extent to which they are open to change and prepared for it is uneven. The Federal Reserve in the US recently held a landmark conference covering tokenisation last October, the first event of its kind at the United States central bank covering innovative digital finance. For one day, the Payments and Digital Asset Innovation Conference brought together experts and regulators to “consider a broad range of perspectives on how to further innovate and improve the payment system”.

Fed’s token message

Christopher J. Waller, a member of the Fed’s board of governors, opened the gathering and said it was intended “to send a message that this is a new era for the Federal Reserve in payments” and that “payments innovation moves fast, and the Federal Reserve needs to keep up.”

As the world’s most influential central bank, the Fed has been careful around financial innovation and tokenisation, giving Waller’s pledge and the conference itself particular resonance. He outlined “a possible prototype” for a Fed payment account. It will come with limits as Washington’s monetary authorities take careful steps into a digital future. “I sometimes call it a ‘skinny’ master account,” Waller said, adding it “would provide access to the Federal Reserve payment rails while controlling for various risks to the Federal Reserve and the payment system.” But interest would not be paid on balances and balance caps may be imposed. The accounts would also not qualify to borrow from the Fed’s discount lending window, a key part of US financial architecture, or have access to all of the Fed’s payment services. Waller said “the payments landscape, as well as the types of providers, has evolved dramatically in recent years, and, accordingly, a new payments account could better reflect this new reality.”

ECB’s bridge and road to the future

The European Central Bank has also adopted twin initiatives regarding what it refers to as distributed ledger technology (DLT), namely the arrival of tokenisation and blockchain in international payments. Both have Latin names that reflect the intention behind each. Pontes, meaning 'bridge,' for instance, is designed for the near term. Later this year, it will link new payment methods to Europe’s existing settlement infrastructure, called TARGET, short for Trans-European Automated Real-time Gross settlement Express Transfer. The ECB says Pontes will offer a “Eurosystem DLT-based solution, linking DLT platforms and TARGET Services to settle transactions in central bank money from the third quarter of 2026”.

Appia, named after the famous Roman road, the Appian Way, has ambitions that stretch into the future. The ECB says it will head toward an innovative and integrated payments and securities ecosystem in Europe that also facilitates safe and efficient operations at the global level. It aims for “interoperability and standardisation” to establish “compatibility between applications across the value chain”.

Bank of England’s sandbox

The Bank of England has already set up what it calls “the regulatory framework” to “enable the private sector to set up trading venues and settlement systems for tokenised assets”. And according to Sarah Breeden, deputy governor for financial stability, the UK’s so-called “Digital Securities Sandbox” will be “real-world transactions in tokenised securities, and market participants will interact with these trading venues and settlement systems in the same way as they do in the conventional financial system. “These won’t merely be prototypes or experiments,” she said in a speech at DC Fintech Week last October.

“Market participants will interact with these trading venues and settlement systems in the same way as they do in the conventional financial system.”

She said the BOE has 15 firms “preparing with regulators to launch trading and settlement venues” as early as 2026, “ranging from established financial firms [including] Euroclear, HSBC, JP Morgan and the London Stock Exchange Group … to new players, and across the full range of asset classes [including] equities, corporate and government bonds, and investment funds including real estate funds.”

The Bank of International Settlements (BIS) – the Swiss-based self-styled “bank of central banks” – has also repeatedly pledged its support for innovation. Andréa M Maechler, deputy general manager of the BIS, told the Singapore Fintech Festival in November that “understanding the technology behind tokenisation, together with the opportunities and risks it presents, is crucial”. She added:

“This requires identifying the fundamental principles that foster trust and stability and understanding how these translate in a tokenised ecosystem. Tokenisation turns static records of financial assets into verifiable digital tokens that can operate on programmable platforms. The programmability and composability of tokenised platforms mean that multiple steps and transactions can be automated and bundled, enabling major efficiency gains and entirely new contracting possibilities.”

BIS’ Project Agorá

The BIS runs a pioneering initiative, Project Agorá, exploring tokenisation for central banks. Named after the Greek word for marketplace, it aims to speed up settlement times.

Seven central banks have signed up, including the Federal Reserve Bank of New York, the Bank of France, the ECB, the Bank of England, and the Bank of Japan. Mexico and South Korea are involved, as is the Swiss National Bank. They are working alongside what the BIS calls a “large group of private financial firms convened by the Institute of International Finance (IIF).”

Maechler explained:

“It combines tokenised deposits and tokenised reserves on a programmable platform, thereby enabling the bundling of multiple steps involved in a cross-border payment in one seamless atomic transaction, including the settlement in central bank money.”

But tokenisation also comes with implications of its own. Western institutions have dominated the international financial system. The dollar is the world’s reserve currency, under US control, giving Washington extra political leverage through sanctions. The European Union’s dominance of the still-essential SWIFT system, given its domicile in Belgium, gives Brussels' international measures similar heft. During times of increasing geopolitical uncertainty, any moves away from these established mechanisms could become more controversial and delayed.

The BIS, long seen as the lead advocate of innovation, has hit problems with previous efforts. Its “mBridge” initiative, dating back to 2021, looked to distributed ledger technology as a means of international payment avoiding SWIFT and the dollar. It was backed by China, Hong Kong, the United Arab Emirates, Saudi Arabia and Thailand. In October 2024, the BIS itself pulled out of the scheme after Russia called for a similar system to be used among the nations of the BRICS bloc, predominantly from the Global South, but dominated by Moscow and Beijing. The renewed effort from the BRICS was widely seen as a potential means around sanctions and the call from the Kremlin came amid sanctions imposed after its invasion of Ukraine in 2022.

IMF’s flash crash warning

The International Monetary Fund has added a note of caution to the discourse on tokenisation in global finance. The 191-member organisation is designed to prevent crises in the global financial system and to advise members on policies for stable economic growth, while also acting as a lender to nations in emergencies. In a video posted on social media, the IMF warned that the increased speed of tokenised transactions may deepen the risk of “flash crashes”, or sudden, steep and dramatic falls in asset prices as markets fragment at times of crisis. Itai Agur, senior IMF economist, said: “Specific policies may be needed for tokenisation to really deliver on its promise while limiting the risks.” He pointed to the prospect of more attention from political authorities, alongside the actions of monetary institutions:

“Governments have rarely been content to stay on the sidelines during important evolutions of money. So If history is any guide, they may take a more active role in the future of tokenisation”.

The Bank of Japan is moving at a pace among the major global economies toward a fully developed tokenised financial ecosystem. It was the first major economy to adopt a law covering stablecoins in June 2023. The legislation was widely seen as a key step toward the tokenisation of a range of assets, setting clear, detailed rules. A digital yen is already being piloted. The BOJ has compared account-based and token-based versions of the currency. Other major central banks remain in the design or consultation phases of using blockchain-style technology to back a digital version of the national currencies. Central Bank Digital Currencies – CBDCs – may prove to be the ultimate test for globalised and tokenised assets. They are likely to take time to develop. Plans toward a CBDC in the US were halted by executive order in January 2025. In the meantime, moves toward tokenised international payments are in the spotlight as investors prepare for the next phase of global finance.

Michael Hunter is an experienced markets and investment writer who’s worked for the FT, Bloomberg, and others over the last 25 years.

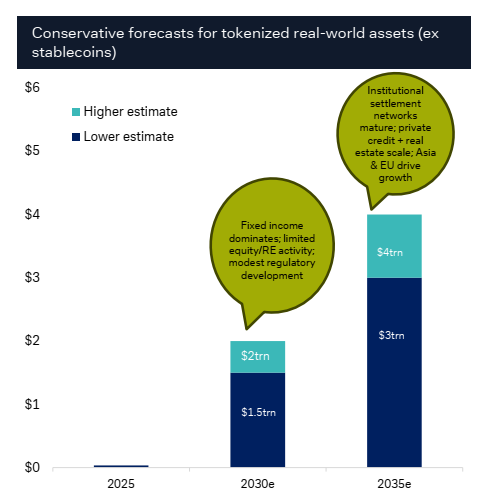

Deutsche on the potential for tokenised real-world assets

Our weekly deep dive into the realms of data kicks off with the Deutsche Bank Research Institute (Asset Tokenisation 101), which maps out the potential for tokenising real-world assets.

“Tokenised capital markets could become the default infrastructure for issuance and trading by the 2030s”

When ETFs Meet Tokens: The Quiet Convergence of Traditional and On-chain Finance

Jürgen Blumberg from Centrifuge

For most investors, ETFs and tokenized assets still appear to belong to different worlds. ETFs are familiar, regulated, and comfortably held in brokerage accounts. Tokenized assets, by contrast, are associated with crypto-native platforms, digital wallets, and a vocabulary that can feel opaque to some outside the digital asset ecosystem.

Yet beneath the surface, these two worlds are already moving toward each other. Over time, the distinction between an “ETF” and a “onchain asset” is likely to blur, not because one replaces the other, but because both evolve toward a shared goal: delivering investment exposure as efficiently and transparently as possible.

ETFs as the Benchmark for Financial Packaging

ETFs solved a powerful problem in traditional finance: how to package investment exposure in a simple, liquid, and low-cost form. They standardized access to equities, bonds, commodities, and increasingly sophisticated strategies. From an investor’s perspective, ETFs represent financial abstraction done well.

Tokens address a different, but complementary, set of constraints. They make assets programmable, transferable around the clock, and native to digital infrastructure. A token is not merely a digital wrapper, it is software that can enforce rules and move value directly.

The point of convergence becomes clear when we ask a practical question: what happens when ETF-like exposure is delivered using token-like infrastructure? Tokenization is often framed as a challenge to existing financial products. In practice, it is better understood as an infrastructure upgrade rather than a replacement. Today’s ETF ecosystem relies on multiple layers of intermediaries: custodians, transfer agents, clearing systems, and settlement processes that still operate on T+1 or T+2 timelines. Tokenized representations of fund interests, or of the underlying assets themselves, have the potential to simplify this stack.

Practically, this can translate into faster settlement, lower operational friction, atomic delivery-versus-payment, and native fractional ownership. None of these change the economic exposure an ETF provides. They change how efficiently that exposure is delivered and managed.

Where Convergence Is Already Taking Shape

Early signs of this convergence are already visible. One example is the emergence of tokenized funds and treasury products. Economically, these often resemble money market funds or ultra-short bond ETFs. Operationally, they behave like onchain assets that can be transferred, settled, or used as collateral with fewer intermediaries.

Another is the appearance of token-based wrappers that mirror existing ETF exposure. Regulatory constraints limit direct issuance in many jurisdictions, but these structures reflect growing demand for familiar investment exposure delivered through digital rails. At the same time, traditional ETFs are beginning to absorb lessons from tokenized markets. Expectations around transparency, intraday liquidity, and operational efficiency increasingly shape how ETF products are evaluated.

The Shift Toward Programmable Investment Exposure

The most significant change is not technical, but conceptual. Tokens introduce programmability into asset ownership. This opens the door to investment products where income distribution, collateral rules, and certain governance functions are enforced directly in code rather than through manual processes. As these capabilities mature, the distinction between an ETF and a token becomes less about form and more about function. What ultimately matters is not the label attached to an instrument, but the exposure it provides, the governance around it, and the trust framework that supports it.

This convergence between ETS and tokens will be shaped by regulation. ETFs benefit from well-established standards around disclosure, investor protection, and governance. Any tokenized equivalent intended for mainstream investors will need to meet similar expectations. Tokenization does not weaken these standards. In many cases, it can enhance them by making holdings, flows, and constraints more observable and verifiable in real time.

Parallel Forms, Shared Purpose

In the years ahead, ETFs are unlikely to disappear, just as tokens are unlikely to remain confined to niche markets. Instead, we are likely to see parallel forms of the same economic reality:

- traditional ETFs held through brokerage platforms,

- tokenized representations used in digital settlement environments, and

- hybrid models that bridge both.

For investors, this is not about choosing sides. It is about recognizing that the familiar investment products they rely on today are gradually evolving under the hood.

The ETF was one of the most successful financial innovations of the past thirty years. Tokens may not replace it, but they are increasingly shaping the infrastructure that carries it forward.

Jürgen Blumberg is a senior financial services executive with over two decades of experience across global markets, trading, ETFs, and blockchain-enabled capital markets. He is Chief Operating Officer at Centrifuge, where he leads operational strategy and drives institutional adoption of tokenized real-world assets (RWA) in decentralized finance (DeFi). In parallel, he serves as Chief Investment Officer at Anemoy, Centrifuge’s Web3-native asset manager, where he develops tokenized RWA funds using a best-in-class multi-manager approach. Centrifuge empowers asset managers to tokenize, manage, and distribute funds onchain, while giving investors access to diversified portfolios of tokenized real-world assets

What do you think? Do you have a strong opinion you'd like to share with us :

Email us at teams@theintersection.news

Worth watching (or even listening):

Watch and listen to our founder, David Stevenson, talking to industry expert Nik Lysiuk talking about how traditional finance and tokenisation are converging:

How Traditional Investing Is Evolving — And How to Position for It

Nik Lysiuk's work focuses on long-term allocation, ownership and custody, behavioural discipline, and continuity planning. Nik shares practical Bitcoin education through YouTube and social media where his content has reached over half a million views.https://www.niklysiuk.com/

Events on our radar:

· Digital Assets Forum 3 – London, 5-6 February - The premier event for the Institutional Digital Assets industry – tickets HERE

· Bitcoin 2026 – Las Vegas, 27-29 April - premier Bitcoin ecosystem event – tickets HERE

· DigiAssets Connect Zurich, 16-17 June - Custody, banking, and institutional infrastructure – tickets HERE