Welcome to the fourth letter from TheIntersection team. We hope you are enjoying this weekly letter.

Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: Gulf states back digital assets

- Data: Wisdom Tree ETFs on why Crypto ETFs adds value to portfolio diversification

- Analysis: Swift’s not-so-swift blockchain bid

- More analysis: Crowdfunder Republic unleashes Kraken

- Our weekly events round-up

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

News in Brief

1. TradFi partnerships accelerate tokenisation adoption:

Institutional involvement continues to deepen. Aviva Investors is collaborating with Ripple to explore tokenised fund issuance on the XRP Ledger, BlackRock has extended its tokenised Treasury exposure into DeFi trading venues, VerifyMe (NASDAQ: VRME) is merging with Open World to build a regulated RWA infrastructure, and Robinhood has launched a Layer-2 testnet designed for tokenised assets and DeFi liquidity integration.

Why it matters: Tokenisation is increasingly being driven by established financial institutions integrating blockchain into existing products rather than launching standalone crypto experiments.

2. Market infrastructure pivots toward liquidity and settlement efficiency: Avalanche’s RWA total value locked has surpassed roughly $1.3bn, supported by institutional tokenised funds and structured credit issuance. Meanwhile, exchanges including the NYSE are exploring blockchain-enabled 24/7 trading venues, with atomic delivery-versus-payment settlement increasingly seen as the next infrastructure upgrade.

Why it matters: The focus is shifting from token creation toward liquid secondary markets, continuous trading and faster settlement.

3. RWA growth broadens across assets and networks: On-chain RWA value is estimated around $24–25bn, with strong growth in Treasuries, private credit and specialised assets such as aviation finance and shipping. Ethereum continues to dominate institutional value flows, while Solana leads in retail wallet growth. Competition among chains — including XRP Ledger — is intensifying as networks position themselves for tokenisation infrastructure.

Why it matters: Tokenisation is expanding beyond financial assets into real-economy use cases, with different blockchains specialising in institutional versus retail adoption.

Deep Dive — The Gulf’s $500bn tokenisation opportunity

Tokenisation could unlock roughly $500bn in real-world assets across the Gulf by 2030, positioning the region as a potential global hub for regulated digital asset infrastructure, according to consultancy Kearney.

The Details

Kearney’s analysis suggests the GCC — particularly the UAE and Saudi Arabia — is unusually well positioned for tokenisation due to large sovereign capital pools, significant real estate portfolios and proactive regulatory development. Governments across the region are linking digital asset initiatives with broader economic diversification and financial modernisation strategies. Real estate is expected to be an early anchor asset class. Large commercial property portfolios and infrastructure projects lend themselves to fractional ownership, improved liquidity and cross-border investment access. Private credit, infrastructure financing and commodities are also highlighted as strong candidates, especially where tokenisation can reduce settlement friction and improve transparency.

Regulation appears to be the decisive factor. The UAE’s virtual asset licensing frameworks and sandbox initiatives have attracted fintech partnerships, institutional pilots, and investment in digital asset infrastructure. That regulatory clarity is helping move tokenisation from proof-of-concept pilots toward production-grade financial products. For financial institutions, the primary appeal remains operational efficiency rather than speculative upside: faster settlement cycles, programmable compliance, reduced administrative costs and broader investor reach. Sovereign wealth funds, regional banks and asset managers are increasingly exploring tokenised funds, structured credit issuance and alternative asset financing. If adoption continues along current trajectories, tokenisation could become embedded within Gulf capital markets rather than remaining a niche digital asset experiment.

Source: Kearney — “Real-world asset tokenisation: A $500bn opportunity for the GCC.”

ETF issuer Wisdom Tree there weresays crypto is integrating into institutional portfolios

Crypto is migrating out of the ‘alternatives’ bucket and into mainstream asset-allocation discussions, alongside gold, commodities and other diversifiers. A growing body of academic and practitioner research suggests that small, disciplined allocations can improve portfolio efficiency over full cycles. Outcomes remain regime-dependent and implementation-sensitive, but the diversification case is no longer theoretical.

Bitcoin is increasingly analysed as a non-sovereign, scarcity-driven asset, sensitive to confidence in fiat systems rather than realised inflation alone.

Asymmetry works only with discipline: small sizing, systematic rebalancing and no momentum chasing.

Governance is decisive. Good governance captures volatility, while poor governance magnifies risk.

Figure: Small bitcoin allocations have historically improved portfolio risk/return metrics

| 60/40 | 1% | 3% | 5% | 10% | MSCI AC World | Bloomberg Multiverse | Bitcoin |

Annualised Return | 6.40% | 7.01% | 8.23% | 9.44% | 12.43% | 9.83% | 1.01% | 48.75% |

Volatility | 8.76% | 8.83% | 9.12% | 9.57% | 11.30% | 13.90% | 4.99% | 65.30% |

Sharpe Ratio | 0.52 | 0.59 | 0.70 | 0.80 | 0.94 | 0.58 | -0.16 | 0.72 |

Information Ratio |

| 0.93 | 0.93 | 0.92 | 0.92 |

|

|

|

Sortino Ratio | 0.63 | 0.71 | 0.86 | 0.98 | 1.20 | 0.68 | -0.22 | 0.97 |

Beta | 69% | 71% | 73% | 75% | 80% | 100% | 24% | 178% |

Source: Bloomberg, WisdomTree. From 31 December 2013 to 31 December 2025. Based on daily USD returns. The 60/40 Global Portfolio is composed of 60% MSCI All Country World and 40% Bloomberg Multiverse. You cannot invest directly in an index. Historical performance is not an indication of future performance, and any investment may go down in value.

Swift’s not-so-swift blockchain bid

by Anna Fedorova

Swift has announced a new blockchain-based “universal” ledger, built with Consensys, as it scrambles to stay relevant in a world where stablecoins are exploding and near‑instant crypto payments are starting to outshine traditional bank rails. The idea isn’t to replace Swift’s existing network, but to bolt on a compliant, interoperable blockchain layer using ISO 20022—though big questions remain.

On 29 September 2025, at the SIBOS Conference in Frankfurt, Swift – the global financial messaging network that enables payments for more than 11,500 financial institutions – announced its foray into blockchain, with plans to launch a “universal” digital ledger to enable what it calls “always-on cross-border payments”.

It’s undertaking this initiative in partnership with Consensys – a leading crypto infrastructure player that, among other things, runs the ecosystem’s most widely used digital wallet, MetaMask. Consensys has spent years adapting Ethereum-based infrastructure for enterprises and regulated financial institutions, including JPMorgan Chase and Société Générale. As such, it is no stranger to institutional integrations or payments, so this choice of partner makes sense for Swift’s blockchain move.

What’s more interesting is the motivation behind it – and to understand it, we need only to look at the relentless rise of stablecoins and the uproar this has caused in the banking sector. Over recent weeks, crypto exchanges and banks in the US have been locked in a stalemate over whether crypto firms should be permitted to pay interest on stablecoins under the Clarity Act, which is currently being hashed out. Banks argue that high yields on stablecoins could threaten traditional bank deposits, with the US Treasury predicting that deposit flight could reach trillions of dollars.

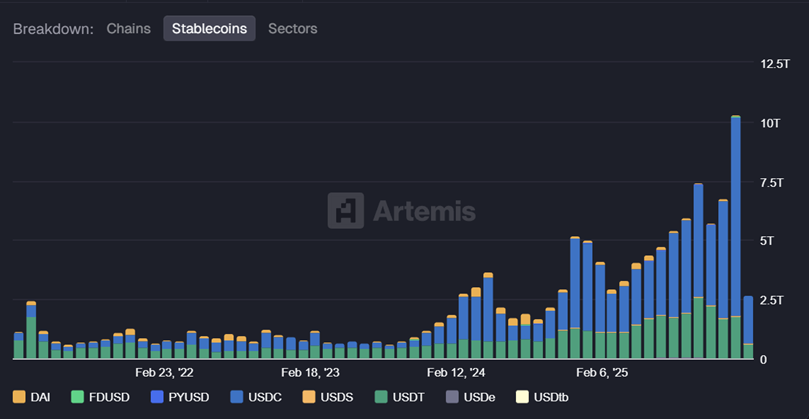

Meanwhile, stablecoin transaction volume rose 72% in 2025 to $33 trillion, and then skyrocketed to $10 trillion in January 2026 alone, according to data from Artemis Analytics. While still small compared to Swift’s $150 trillion in annual transactions, stablecoins are quickly becoming a force to be reckoned with.

Stablecoin transaction volume growth (Source: Artemis Analytics) Stablecoins | Artemis Terminal

Rising to the challenge

Against that backdrop, it’s no wonder banks are looking to remain competitive – and this means upgrading existing infrastructure. Announcing the blockchain ledger at the Sibos conference, Swift’s CEO Javier Pérez-Tasso was clear: “Banks are ready for it and they’re asking us to play a bigger role”. And Swift appears to be ready to rise to the challenge. However, to say Swift is keeping the details of its blockchain bid tightly under wraps would be the understatement of the century. While some details have emerged since the announcement more than four months ago, they’re few and far between.

In an interview with Bloomberg about the Swift project, Joe Lubin, CEO and founder of Consensys, watched every word carefully and offered little beyond what was already in the press release. He was, however, clear that sentiment toward digital finance had changed "significantly" since the early days of Ethereum – of which he is a co-founder. Back then, the idea of TradFi and DeFi working together was a pipe dream.

“The vibe in Frankfurt [at the 2025 Sibos conference] was very different,” Lubin said. “And the feedback we…and the Swift leadership have heard from banks is very positive. It’s basically about time for TradFi to merge, or make use of, DeFi.”

The facts

What we do know is that Swift is building a blockchain-based shared ledger that will combine with its existing messaging and APIs, following ISO 20022 – the global standard for structuring and exchanging financial messages. It aims to facilitate real-time 24/7 cross-border transactions, supporting what it calls the “trusted movement of tokenised value”.

During his opening speech at Sibos 2025, Pérez-Tasso made it clear that Swift isn’t planning to replace its existing rails with blockchain technology, but rather to add a new feather to its cap. He called this approach a combination of "rejuvenation and innovation” – developing the system along two parallel tracks that have “one foot in the past and one in the future”.

“I hear a lot of noise out there that the industry needs to do away with existing rails and replace everything from scratch. But I don’t think we need to throw out the baby with the bathwater,” he said. “It’s not either or, it’s definitely both.”

According to Swift’s CEO, today, 75% of payments on the Swift network reach their end beneficiary banks within 10 minutes. But in the world of near-instant stablecoin payments, this is no longer enough. So this is one area he plans to tackle with the integration of blockchain technology.

Ultimately, though, Swift’s blockchain initiative is less about making payments faster, and more about preserving its role as the neutral coordinator of global finance in a world where coordination is no longer guaranteed. It aims to record, sequence and validate transactions via smart contracts in a way that is interoperable with both existing financial infrastructure and the emerging financial economy.

However, Swift doesn’t intend to build its own blockchain or issue its own digital assets – its focus is solely on the infrastructure side. Industry reporting suggests Swift’s prototype may be running on Consensys’s Linea blockchain – an Ethereum Layer-2 network focused on faster and cheaper transactions.

The Holy Grail of crypto

In the months since the announcement, Swift has made some practical progress. In December, it announced a proof-of-concept for cross-border transfers of tokenised deposits, in collaboration with Ant International and HSBC. This showed that, with ISO 20022, the transfer of tokenised deposits can plausibly scale beyond random one-off experiments into something akin to the existing global banking system.

Then, in January, Swift completed what it called a “landmark digital asset interoperability trial” with BNP Paribas Securities Services, Intesa Sanpaolo, and Societe Generale, demonstrating that the seamless exchange and settlement of tokenised bonds were possible using both fiat and crypto payments. Its goal is clear: to solve the fragmentation problem that has plagued the digital assets space since its inception, paving the way for a unified financial system.

As Swift’s Thomas Duguauquier, tokenised assets product lead, puts it: “By proving that Swift can orchestrate multi-platform tokenised asset transactions, we’re paving the way for our members to adopt digital assets with confidence, and at scale. It’s about creating a bridge between traditional finance and emerging technologies.”

But it’s important not to underestimate how tall an order this is for an ecosystem where even interoperability between different blockchains remains the illusory Holy Grail. Crypto has struggled with interoperability since there are multiple blockchains between more than one blockchain.

For example, you can’t simply send a USDT stablecoin issued on Ethereum to Solana without relying on mechanisms such as swaps, cross-chain bridges, or intermediaries. This quickly undermines one of the key benefits of stablecoin transfers.

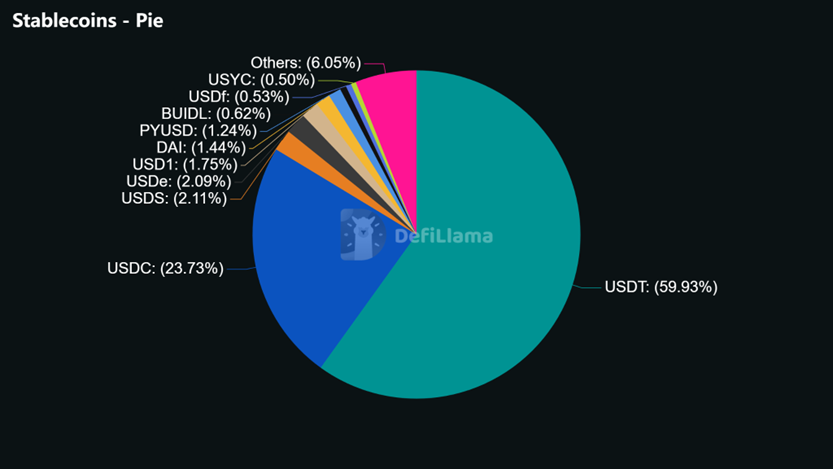

Stablecoins: by type (Source: DeFi Llama)

Fragmentation & regulation

If Swift can truly solve this issue by providing infrastructure that allows financial institutions to move all types of digital assets across the globe using both fiat systems and blockchain, that would be nothing short of groundbreaking. But it will likely face many challenges along the way.

It’s not just the technology that is fragmented – it’s also the regulatory landscape. A global blockchain ledger will have to meet the requirements of jurisdictions worldwide with very different attitudes toward blockchain technology, many of which haven’t finalised their frameworks yet. This may well be a major headwind.

Some in the industry disagree. Nick New, co-founder and CEO of Optalysys, argues in a blog that the calibre of institutions involved in this project, including banks like HSBC, JPMorgan and Deutsche Bank, will encourage regulators to review their rules or propose new, supportive legislation.

This may well be. In fact, Swift says it has already submitted a proposal for new market practice guidelines to the Securities Market Practice Group (SMPG). But regulatory changes typically take time, and time isn’t necessarily a luxury Swift has.

When asked by Bloomberg about a potential timeline for the rollout of this new ledger, Joe Lubin chose to remain silent, and Swift hasn’t been forthcoming with a detailed plan. Realistically, it will take years for this to move from the experiment phase to a finished offering. In that time, competition from existing stablecoin rails will no doubt intensify.

From pilot to success

This brings us full circle to the question of revenue. Just as with the rollout timeline, Swift hasn’t yet explained how this new blockchain layer will be monetised. Does it consider this a necessary investment to remain relevant in a rapidly changing landscape? Or will this be a premium service available only to a handful of major banks that work with Swift?

The latter would certainly be easier to implement on a single, permissioned blockchain. Although even then, the trillions of dollars in institutional flows across the globe would test such a blockchain to its limit. But if this universal ledger is limited to a select few participants – which I suspect it will be at least to start with – how long will it be before the benefits are passed on to the average user of the Swift network, whether small businesses or individuals?

For the project to be declared a success, these questions must be clearly answered, and the beneficiaries must be clearly defined. That’s because for this to move from controlled pilot to universally used infrastructure, commercial incentives must align for all participants. If Swift’s move is seen primarily as a defensive response to the growth of stablecoins, rather than as a value-creating initiative, adoption may stall even if the technology doesn’t.

In practical terms, success would mean Swift moving from controlled pilots to a live production corridor with real volume, real liquidity, and clearly defined governance, before stablecoin-native rails become the default for cross-border settlement.

On the technology front, Swift’s plan relies heavily on universal adoption of ISO 20022. And so far, this adoption remains uneven – especially when it comes to smaller banks. If banks continue relying on legacy internal formats, this could also slow the scalability of Swift’s new model.

Not only that, but banks and other institutions will have to agree on a wide range of governance questions: from who sets the rules and settles disputes, to how smart contracts are updated. And there are many cooks in this kitchen – each of Swift’s 30 bank partners has its own risk appetite and commercial priorities.

But none of this will matter if regulators can’t agree on a consistent global framework for tokenised assets. Especially given Swift’s explicit emphasis on a compliance-first design. While it can influence regulatory decisions, it can’t force regulatory alignment – and this may well end up dictating the timeline.

Republic Europe releases the Kraken

Damien Black

Kraken has long been known as a platform for trading digital assets – now investors, both large and small, can invest in the US cryptocurrency exchange itself, thanks to a new vehicle from Republic Europe that aims to lower the barrier to entry.

For as little as $45 (£33), the price of a single share, you can take a punt on rKRKN, a special purpose vehicle (SPV) specifically designed to allow smaller retail investors to hold Kraken equity for the first time. Republic Europe’s announcement comes on the back of some pretty solid figures for the Kraken platform, which allows users to trade in more than 450 digital assets including cryptocurrencies such as Bitcoin, Dogecoin and Ethereum. Last year, it reported tidy revenues of $2.2bn, around the same time it received an overall valuation of $200bn for investment.

Giving the small guy a chance

Kraken stock has previously been available for investment, but only to larger institutional investors. The rKRKN SPV, overseen by Republic Europe, aims to change that by lowering the entry barrier. “We believe that access to later-stage private companies shouldn't be reserved for the few,” said Republic Europe, an equity crowdfunding platform. “By using this SPV structure, we can lower the minimum investment amounts and handle the institutional investment, allowing you to diversify your portfolio with a global digital asset platform.”

Republic Europe stressed that rKRKN is an indirect investment. “Kraken has not reviewed, endorsed or participated in this offering,” it said. “Investors will become shareholders in the SPV through the Republic Europe nominee structure. The SPV will hold common shares directly in Kraken.”

Making quality accessible

Incorporated by Republic Europe in London on 27 January this year, rKRKN provides access to the US platform, headquartered in San Francisco and serving more than 13 million users across 5.7 million funded accounts. Republic Europe has been licensed by the Financial Conduct Authority in the UK.

It believes that the SPV move will democratise investing – an idea that lies at the heart of the cryptocurrency and tokenization world. “With many companies staying private for longer, the most significant wealth creation opportunities do not enable access for the masses,” said Theodora Bishop, Senior Investment Manager at Republic Europe. She added: “The launch of the Kraken SPV offers a rare opportunity: enabling the community to take an indirect financial interest in a global leader shaping the future of finance. This marks a defining moment for Republic Europe, and investors, as we bring private-market quality into the public sphere.”

It wasn’t always thus

How times have changed. In November, Kraken announced it had filed an S-1 form with the Securities and Exchange Commission (SEC), paving the way for an initial public offering (IPO) after raising $800bn on the back of the Citadel valuation. But earlier that same year, the SEC dropped a lawsuit against Kraken that it had filed in 2023. This accused the cryptocurrency platform of operating as an unregistered online trading platform in violation of securities law.

The SEC dropped the suit in March 2025 after Kraken successfully argued that it was being wrongfully targeted amid a climate of regulatory uncertainty – the rulebook for crypto firms has not yet been written. The SEC’s decision to relent marks a broader regulatory shift in favour of crypto companies, as evidenced by the GENIUS Act, which regulates stablecoins and was passed amid considerable fanfare last year. Other big players in the space who have recently been let off by the regulatory body include Coinbase, MetaMask, Robinhood and OpenSea.

Release the Kraken!

For smaller investors, the problem with Kraken is that it is not a publicly listed company – yet. Until now, you needed to be an accredited investor to get skin in the game – that usually means having a net worth of at least a cool million.

What rKRKN effectively does, therefore, is act as a middleman, bypassing this gate. Republic Europe has presumably bought a large chunk of shares using its own capital, wrapped the Kraken stock in a single entity (the SPV) and offered fractional units to investors. What that means is small fish like you and me get to have a nibble at the very big fish that is Kraken. Of course, one should also emphasise what it doesn’t mean – namely, that you are guaranteed to make money. Caveat emptor (“buyer beware”) applies always, to smaller investors who don’t have all the money in the world, all the more so.

Convenience costs money

Another thing to bear in mind is that Republic Europe is not a charity – it is charging a premium for its service. So don’t be too disgruntled when you take to private secondary markets and see that their valuations (the ones open to the ‘big boys’ who meet accredited status) are averaging well below Republic’s $45 per share. Also, don’t forget that Kraken doesn’t have an official fixed share price – as it would do if it were listed openly on, say, the NYSE. Different private secondary marketplaces such as Forge Global ($36.42), Hiive ($34.62) and Nasdaq ($41.57) are all charging different rates. Figures quoted here were valid at the time of writing.

So all things considered, Republic Europe’s asking price of $45 isn’t too shoddy. But even so, there’s no getting away from the conclusion that asking prices are lower for those players who meet the capital requirements to invest directly. In other words, the richer you are, the lower the price. Whoever said finance was fair?

{kind=link}