Welcome to the third letter from TheIntersection team.

Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: China gets tough, and seismic tokens

- Analysis: Digital Gold comes of age

- Data: Tether has become a big buyer of physical gold

- Opinion: Why the Real-World Asset Revolution Isn't Just a Better Wrapper

- Our weekly events round-up

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

China extends crypto ban to stablecoins and tokenised assets

Chinese regulators, including the People’s Bank of China and securities authorities, have expanded their crypto crackdown to explicitly cover stablecoins and tokenised real-world assets. The updated rules prohibit the issuance of RMB-linked stablecoins without approval, restrict overseas tokenisation of domestic assets, and extend compliance obligations to financial institutions and technology providers involved in such projects. The move reinforces China’s long-standing priority of maintaining monetary sovereignty and tight control over capital flows, even as other jurisdictions explore tokenisation frameworks.

Why it matters: China is signalling that tokenisation linked to domestic assets, payments, or currency exposure will remain tightly controlled, highlighting how regulatory fragmentation continues to shape where RWA markets can realistically scale.

News in Brief

Retail access to tokenised markets expands

MetaMask has integrated Ondo Global Markets, allowing eligible users to trade more than 200 tokenised U.S. stocks, ETFs and commodities directly from self-custodial wallets. At the same time, industry groups, including ChainUp and 1exchange, are forecasting that 2026 will be the year secondary market liquidity becomes the priority rather than simple token issuance, with an increasing focus on continuous trading and deeper order books. Why it matters: The narrative is shifting from creating tokenised assets to building functional trading infrastructure that mirrors traditional capital markets.

Institutional tokenisation accelerates in emerging markets

The XDC Network, working with Liqi Digital Assets, has surpassed $100m in tokenised RWAs in Brazil, with major banks such as Itaú and ABC focusing on credit assets and regulated debt instruments. Separately, NewGen has launched a tokenised real estate bond initiative via Hong Kong’s regulated Evident Capital platform, reflecting continued interest in property-backed issuance structures. Why it matters: Banks are moving beyond pilots into credit, trade finance and real estate — sectors where tokenisation can improve liquidity, transparency and investor access.

News Deep Dive

Tokenising seismic data: Blue Horizon tests a new frontier in RWA used in energy exploration, which has historically generated licensing revenue but has remained difficult to value transparently.

Blue Horizon is assessing whether blockchain-based asset structuring could unlock value from a 3D seismic dataset in Montana with an estimated internal fair value of roughly CAD $15m. The data used in energy exploration has historically generated licensing revenue but has remained difficult to value transparently in public markets. Management argues that long-life data assets, such as seismic surveys, often trade at a discount because they are illiquid, generate uneven cash flows, and sit outside a company’s core operations. Rather than selling the asset outright or raising traditional financing against it, the company is considering a regulated tokenisation structure designed to surface embedded value while retaining strategic control.

The proposed model would place economic rights from the dataset into a special purpose vehicle (SPV), which could issue regulated securities linked to licensing income. Blue Horizon would keep operational oversight, while investors would gain exposure to revenue streams without governance control. If implemented, blockchain would function primarily as an administrative registry and settlement layer rather than a speculative crypto vehicle. The initiative remains exploratory, with no confirmed issuance timeline. The broader implication is that tokenisation is expanding beyond traditional financial assets into data, intellectual property and resource analytics — areas where valuation opacity and illiquidity have historically constrained capital formation.

Digital gold offers investors the best of both

The World Gold Council is trialling a new form of gold ownership which could unlock novel advantages and use cases for investors and institutions

by Dan McEvoy

Everyone wants a piece of the gold pie – but what if you want a fraction of a gold bar? Gold’s epic rise was the investing story of 2025. Gains of over 64% marked the yellow metal’s best calendar year since 1979. Investors the world over are now piling into the stuff: the World Gold Council’s latest gold demand trends report showed that global gold demand for investment purposes increased to 2,175 tonnes in 2025, up from 1,185 tonnes the previous year. Of this uplift, the vast majority – around 804 tonnes – was accounted for by ‘ETFs and similar products’.

This makes sense, on the face of it. Retail investors, on the whole, don’t want to buy an entire bar of gold in one go. It’s inconvenient to store, and fundamentally fairly illiquid.

But there is a catch. A big part of the investment rationale for gold is its ability to act as a hedge against instability in the TradFi system. As such, many gold bugs insist that you need to buy the real thing. Owning it through ETFs exposes you to counterparty risk: you don’t actually own any gold, but rather a contract that is backed by gold (for that reason, this is known as ‘unallocated gold’). You could easily be left out of pocket if the issuer goes bust (and historically, gold really comes into its own in the kind of environment where financial institutions start going bust).

Owning a gold bar (or a gold coin, or other smaller chunks of gold) is known as ‘allocated’ ownership. You can keep that bar at home if you want, or entrust it to a custodian, but either way, there is a piece of physical gold out there that belongs to you. But as well as the cost and logistics involved in either storing your own gold securely or entrusting it to a custodian, owning allocated gold also means you must buy gold in multiples of one bar. A standard 400oz gold bar currently costs over £1 million. Some brokers sell smaller bars, but even the smallest will still cost over £100. Physical gold is not a particularly liquid asset (unless you have access to a thousand degrees C of heat, in which case, you can think about melting your gold down and dividing it into more manageable chunks). So how do you get the security of allocated gold while retaining the convenience of unallocated gold?

What’s happening with digital gold?

Digitising ownership of physical gold could solve this conundrum. In December, the World Gold Council (WGC) to develop an innovative new digital form of gold, Pooled Gold Interests (PGI). The idea is to give holders ownership of a fractional share of a physical gold bar, in increments as small as a thousandth of a troy ounce. The WGC is designing this system to be technology-neutral but with a modern technology stack in mind; as such, it will be compatible with distributed ledger technology (DLT) and blockchain. “Technology has the power to transform the global gold industry, making it more accessible, transparent, and trusted than ever before,” said David Tait, CEO of the World Gold Council[1] .

Where can you buy tokenised gold?

While the World Gold Council is venturing into digital gold for the first time, there are some forms of tokenised gold already available for anyone who wants access to the precious metal’s price action without relying on either an ETF or physical ownership. HSBC became the world’s first global bank to offer tokenised physical gold back in 2023 through its HSBC Gold Token. Initially, it was aimed purely at institutional investors, though it soon opened up access to retail investors based in Hong Kong.

But the biggest players in tokenised gold are the gold-backed digital tokens Tether Gold (XAUt) and Pax Gold (PAXG). According to ARK Invest’s latest DeFi quarterly[2] report, tokenised commodities grew 64% quarter-over-quarter in Q4 2025, largely driven by these two tokens. Tether is estimated to hold $24 billion worth of gold[3] , making it the largest gold holder that isn’t a government, a central bank or an ETF issuer.

Why digitise physical gold?

Digitising physical gold ownership offers a few key advantages to investors:

Improved liquidity

Digitised gold offers improved liquidity in gold trading.

Digital gold, such as PGI, can be stored and traded on DLT, potentially facilitating faster trade execution: in theory, digital gold would be accessible and tradeable 24/7 from anywhere in the world and could settle instantaneously.

Smart contracts could also be used to automate parts of the buying and selling process for digital gold.

Fractional trading

Digitised gold can divide ownership of physical gold into units as small as one thousandth of a troy ounce.

That will enable investors to buy and sell gold in far smaller quantities. Based on £3.50[4].

Mitigating counterparty risk

Investing in digitised gold also reduces counterparty risk compared with buying gold ETCs.

If you buy a gold ETC and the issuer goes bust, you stand to lose your investment. But buying a digital gold token means that your investment is permanently logged in the distributed ledger.

Fairer pricing

Buying physical gold on DLT also eliminates the need to transport or store it, meaning investors can access itup to 30% to the price of gold purchased through traditional channels at closer to spot prices. CoinDesk estimates that these premiums can add up to 30% to the price of gold purchased through traditional channelsthat the gold used be physically segregated from other gold holdings, meaning it must.

Collateralisation and other new use cases

There are further advantages of tokenised gold, especially for financial institutions: particularly its potential to unlock the use of gold as collateral in financial transactions. Being the quintessential store of value, gold ought to be an excellent candidate for collateral. However, under European Market Infrastructure Regulation (EMIR) rules, financial institutions in the UK and the EU can’t use unallocated gold as collateral.

Theoretically, allocated gold can be used, but underwriting financial contracts with physical gold bars has some major drawbacks. Most clearing houses and exchanges require that the gold used be physically segregated from other gold holdings, meaning it mustthe use of be physically exchanged and stored by the clearing house. The upshot is that gold effectively can’t be used as collateral, meaning that it sits on institutional balance sheets as a dormant, yieldless asset.

The WGC has designed its PGI ecosystem to facilitate the use offrom gold as collateral. The underlying gold bars are already segregated, so there is no need for a physical transfer. Tait told an interview with the Financial Times. “For the banks, from a collateral perspective, they will make a lot of money, as they get an opportunity to use the gold on their balance sheet as collateral,” he said.

The WGC is trialling PGI with commercial participants early in 2026. We will wait and see what other use cases emerge fromde-dollarisation these trials.

[1]https://www.gold.org/news-and-events/press-releases/world-gold-council-launches-report-exploring-future-uses-digitalised

[2]https://www.ark-invest.com/crypto-reports/defi-quarterly-q4-2025

[3]https://fortune.com/2026/01/30/the-crypto-industry-used-to-store-bitcoin-in-swiss-vaults-now-one-firm-is-using-vaults-to-hold-gold-instead/

[4]Or $5 if you are part of our US audience

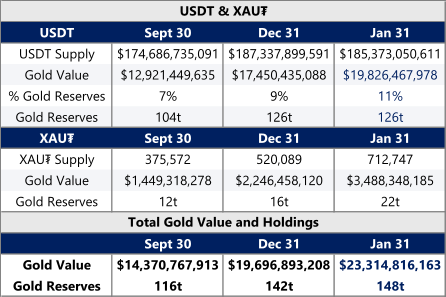

Tether is now a major player in the gold markets

According to analysts at US investment bank Jefferies, stablecoin Tether remains the largest non-sovereign buyer of physical gold and ranks within the top 30 global holders. As of Jan 31, we estimate that Tether's physical gold holdings rose to 148t valued at $23B after purchasing 26t in 4Q25 and 6t in Jan'26. Central bank and investment demand, geopolitical uncertainty, and de-dollarisation contributed to gold's 49% rise from Jul'25 through Jan'26, but we continue to believe that Tether's buying also played a role.

Exhibit 1 - Physical gold held as reserves for USDT and XAU₮ rose to ~142t ($19.7B) as of Dec 31 and ~148t ($23.3B) as of Jan 31

"Recent commentary from Tether's CEO Paolo Ardoino reinforces that the company’s pace of physical gold buying is not only continuing but is now strategically anchored by an explicit reserve allocation framework. Mr. Ardoino stated that Tether plans to allocate 10-15% of its investment portfolio to physical gold, formalizing what has already been a multiyear accumulation trend. We cannot say categorically what Tether’s current gold position represents in percentage terms, as the company has not disclosed the size or composition of the ‘investment portfolio’ referenced, or how much of that portfolio is currently allocated to physical gold."

Opinion: Why the Real-World Asset Revolution Isn't Just a Better Wrapper

By Mathew Harrowing of Instruxi

The numbers look like a victory lap. Since the start of 2025, tokenized U.S. Treasury debt has surged by over 127%, crossing the $10 billion mark this January. BlackRock’s BUIDL fund alone sits at $1.81 billion in assets. To the casual observer, the "Real-World Asset" (RWA) revolution has arrived, dressed in the pinstripes of institutional sovereign debt.

But if we step back from the charts, a sobering question emerges: Is faster access to the same T-bills really the ceiling of what we’re building? Until the landmark Ondo Summit in February 2026, tokenized Treasuries were merely the "comfort food" for institutions. They map cleanly to existing workflows, the customers are predictable, and the risk is low. But let’s be honest: moving the same exclusive assets between the same exclusive players on slightly faster rails is traditional finance wearing a Web3 mask.

The real RWA revolution is about enabling products that could not exist without the blockchain, and Treasury bills appear to have been merely an overture.

The "Boring" Ceiling of Digital Wrappers

The problem with the current "Conservative Play" is that it preserves the very market structures blockchain was meant to disrupt. We have gated access, limited composability, and little participation from anyone other than a corporate treasurer or an asset manager.

Institutional adoption has proven that banks will use blockchain when it saves them a few basis points on settlement. However, it has not yet substantiated the readiness to fully leverage the technology's inherent attributes- namely programmability, transparency, and atomic settlement- to foster a more equitable or innovative financial ecosystem.

Ondo’s recent announcement to pivot from a simple issuer to a full-stack on-chain prime brokerage hints that more innovative offerings are finally afoot. By integrating hundreds of tokenized U.S. stocks and ETFs directly into MetaMask, they have effectively bypassed traditional retail brokerage accounts for eligible non-U.S. users. Furthermore, Ondo’s confidential registration statement filed with the SEC signals a new standard for transparency and reporting in tokenized securities markets globally.

Beyond the Low-Hanging Fruit

To move past the "wrapped asset" phase, we must leverage the technical capabilities currently left on the table. Imagine a financial ecosystem where compliance is not a manual hurdle but a "golden thread" woven into the asset itself.

By using Decentralized Identifiers (DIDs), Verifiable Credentials (VCs), and governance structures, we can create credentialed and policy-bound wallets. Once a wallet is verified for jurisdictional or accredited status, that "passport" stays with the user, unlocking products across the ecosystem and gating access without repeated onboarding. Tokenized assets traded on-chain are thus tethered to a verifiable data stream, forming an unbreakable chain from the token to the underlying data verifying its price and state. In this model, compliance is automated.

What Real Innovation Looks Like

We are finally seeing the first glimpses of this "Phase Two". In January 2026, we saw the launch of pmUSD, a stablecoin backed by $235 million in tokenized gold securities. Unlike static T-bills, pmUSD utilizes on-chain trading fees captured to reward holders, creating a self-reinforcing cycle of real-world revenue and liquidity. The integration with Gearbox Protocol turns this flywheel into a turbine by unlocking "Leverage-as-a-Service". Investors can now borrow against gold-backed holdings (up to 90% LTV) to compound yields. Because Instruxi’s TrustSync proves reserves in real-time, DeFi protocols can safely offer this leverage. Looking forward, this infrastructure enables streaming credit- disbursing loans second-by-second based on verified milestones- and cross-chain collateralization via Chainlink’s CCIP.

The Road Ahead: Yield or Utility?

Conservative estimates suggest the tokenized Treasury market will hit $14 billion later this year. That’s a healthy business, but it’s a game of basis points and brand power. The real opportunity lies with the institutions willing to ask: What can I build next? The infrastructure is ready, and the capital is committed. We can continue to use the world's most powerful financial technology to shuffle 13-week bills slightly faster, or we can start building the transparent, automated, and hyper-efficient markets the next decade demands.

Mathew Harrowing, Co-Founder and CEO of Instruxi, a Web3 infrastructure company focused on deployable tokenisation, identity, and policy enforcement for enterprise and real-world asset use cases. His background spans EY, PwC, and Fitch Ratings, including work in blockchain and distributed systems.

Who is Instruxi? Instruxi provides the control plane for institutional, permissioned blockchain applications. We help enterprises connect existing Web2 systems, identity, data, audit, and workflows, to Web3 execution environments, smart contracts, wallets, and on-chain settlement, without pushing sensitive data on-chain or giving up operational control.