Welcome to the sixth letter from TheIntersection team. We hope you are enjoying this weekly letter. Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: JPMorgan speeds up token adoption, compliance and DeFi

- Data: On-exchange token, AuM is still small

- Analysis: Amundi’s first tokenised fund

- More Analysis: On-chain assets ‘worth $10trn by 2030’

- Our weekly events round-up

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

XRPL tokenised asset activity surges

Tokenised real-world assets on the XRP Ledger (XRPL) have risen sharply in early 2026. Assets issued on the network have grown from roughly $990m at the start of the year to about $2.3bn, meaning more value has been added in the first two months of 2026 than during all of 2025.

The increase has been driven largely by institutional integrations. Recent developments include Société Générale launching a euro-denominated stablecoin on XRPL, Aviva Investors partnering with Ripple on tokenised fund infrastructure, and Deutsche Bank integrating Ripple technology to enable cross-border payment flows that connect to tokenised assets. Why it matters: XRPL is increasingly positioning itself as infrastructure for institutional tokenisation rather than retail crypto trading. Banks and asset managers are testing blockchain rails for payments, funds and tokenised securities — areas where operational efficiency matters more than speculative trading.

News in Brief

1. JPMorgan expands tokenised fund infrastructure

JPMorgan has expanded the rollout of its Kinexys Fund Flow platform (formerly part of the Onyx blockchain division). The system tokenises investor records and automates capital calls and distributions for private equity funds. It is now being integrated across the bank’s wealth management and brokerage divisions. Why it matters: Tokenisation is increasingly being used to modernise back-office infrastructure - particularly in private markets where administration, reporting and settlement processes remain slow and fragmented.

2. China maintains a crypto ban but opens a narrow RWA pathway

China’s central bank has reaffirmed its ban on domestic cryptocurrency activity while allowing tightly controlled offshore tokenisation structures linked to Chinese assets. The framework allows companies to raise capital internationally without opening domestic financial markets to crypto trading. Why it matters: The policy reflects China’s dual strategy — strict domestic controls paired with cautious experimentation in cross-border tokenised financing.

3. Mortgage-backed assets move on-chain

Better Home & Finance has secured a $45m investment from Framework Ventures to develop a mortgage-backed RWA token strategy. The initiative aims to package residential mortgage exposure into tokenised instruments that can trade on blockchain infrastructure while remaining inside regulated financial structures. Why it matters: Mortgage markets represent one of the largest pools of real-world financial assets. Tokenisation could eventually improve transparency and liquidity in mortgage risk trading.

4. Commodities and sustainability assets drive “RWA 2.0”

Issuance of tokenised gold, commodity-backed instruments, carbon credits and energy-linked assets is accelerating as the next phase of the RWA market develops. These assets appeal to institutional investors because blockchain rails offer traceability and auditability — key features for ESG reporting and regulatory oversight. Why it matters: Sustainability-linked assets and commodities could broaden the investor base for tokenised markets beyond crypto-native participants.

Deep Dive

Compliance-first tokenisation becomes the default

The Top Line: Real-world asset tokenisation is shifting toward a compliance-first architecture, with KYC/AML checks, jurisdictional restrictions and transfer rules embedded directly into the token itself.

The Details

As institutional adoption grows, tokenisation platforms are increasingly embedding compliance controls at the token level rather than relying on off-chain checks by brokers or administrators. These controls include identity-verified wallets, jurisdictional whitelists and programmable transfer restrictions that automatically block non-compliant transactions.

Regulators are also becoming clearer about how these instruments should be classified. Increasingly, RWA tokens are treated as digitised financial products, with clearer distinctions emerging between utility tokens, payment tokens and asset-backed tokens. This regulatory clarity makes it easier to structure tokenised instruments within existing securities frameworks. In practice, that means private placement exemptions, permissioned distribution, and regulated secondary trading for assets such as tokenised bonds, private credit, and real estate. The broader implication is that “compliance as code” is becoming a prerequisite for liquidity. If investor eligibility and transfer restrictions are built directly into the asset, trading venues can support secondary markets with fewer operational risks. Many industry observers describe this transition as the emergence of “RWA 2.0” - a phase where tokenisation moves beyond experimentation toward scalable issuance, institutional infrastructure and regulatory alignment.

Further reading

- https://www.ainvest.com/news/institutional-adoption-rwa-tokenization-2026-strategic-inflection-point-blockchain-backed-finance-2512/

- https://www.mexc.com/en-GB/news/82779https://www.mexc.com/en-GB/news/827797

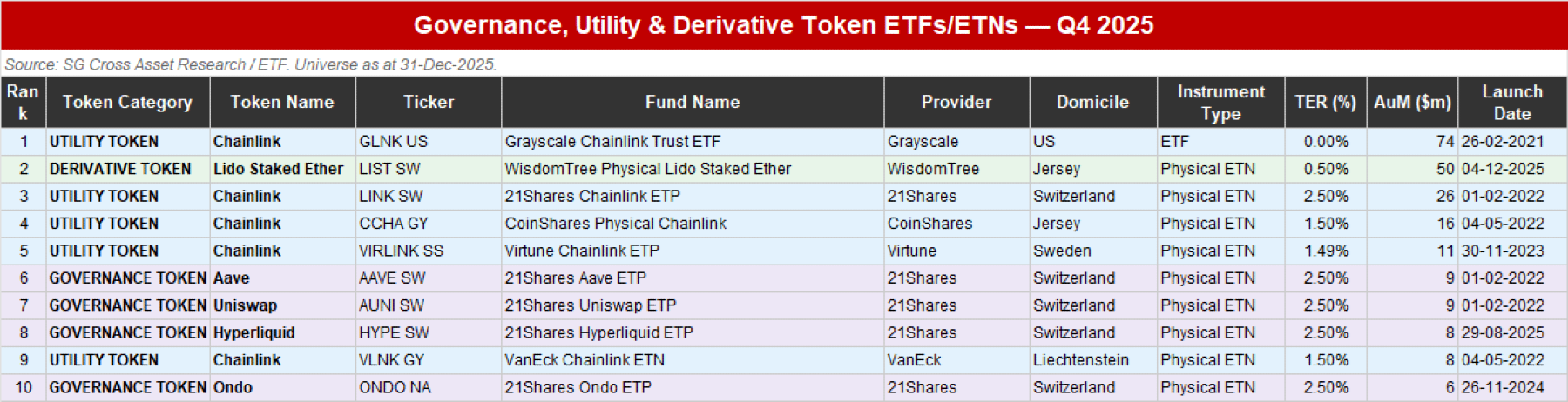

Société Générale deep dive into on-exchange token ETPs

ETF specialists at the French investment bank recently released their comprehensive survey of on-exchange-traded products within the broader crypto space. Quite the most interesting part of this comprehensive survey was the look at on-exchange listed ETPs tracking tokens, in all shapes and guises. Despite the hype surrounding the rise of these funds, the assets under management (AuM) of all 35 of them remain small. Total disclosed AuM across all three categories is roughly $233m, with a heavy concentration in Chainlink utility token products. TERs are consistently high — averaging ~1.8–2.1% across governance and utility tokens — reflecting the niche and newer-vintage nature of these products.

🟣 Governance Tokens (21 products) — dominated by 21Shares and Valour; Aave and Uniswap ETPs are the largest at ~$9m each; many DeFi-native tokens (Ondo, Pyth, Hyperliquid) with very small AuM

🔵 Utility Tokens (12 products) — Chainlink is the standout, led by Grayscale ($74m) and 21Shares ($26m); most others sub-$2m

🟢 Derivative Tokens (2 products) — WisdomTree's Lido Staked Ether ($50m) vs Valour Tether Gold (~$0m)

Token Directory (ranked by AuM, colour-coded by category):

Amundi’s first tokenised fund (and surprisingly conservative outlook)

Amundi launched its first tokenised fund in November. Despite a relatively pessimistic short-term outlook, Europe’s largest asset manager thinks tokenised finds could catch on among crypto-savvy digital natives in the longer term.

“The tokenisation of assets is a transformation set to accelerate in the coming years around the world,” said Jean-Jacques Barbéris, Head of Institutional and Corporate Clients and ESG at Amundi. Barbéris was commenting on the launch of Amundi’s first tokenised share of the Amundi Funds Cash EUR money market fund – its first available in tokenised form.

Amundi’s wasn’t the UK’s first tokenised fund. The month before, Federated Hermes launched its first non-US digital assets initiative by offering two of its UCITS money market funds[1] (Federated Hermes Short-Term Sterling Prime Fund and Federated Hermes Short-Term U.S. Prime Fund) in tokenised forms. Prior to that, in June 2025, Baillie Gifford launched the UK’s first tokenised OEIC[2] , a feeder to its Strategic Bond Fund. More asset managers could soon join the party: Aviva Investors announced [3]. But it is a significant development for Europe’s largest asset manager to embrace tokenised funds, and one that highlights their potential for the industry – even if Amundi is surprisingly bearish about the opportunity (in the short term, at least).

How excited is Amundi about tokenised funds?

Amundi’s December 2025 report into the fund tokenisation market[4] puts the value of the market at $10 billion at the end of last year (compared to a global asset management industry overseeing around $128 trillion), with a neutral estimate that sees it reaching $120 billion by 2030. Its conservative scenario sees tokenised funds reaching $30 billion in AUM by 2030. These outlooks don’t paint a particularly exuberant picture, compared to other forecasts. Its most bullish scenario – $300 billion in AUM by 2030 – posits the same market size as McKinsey’s most conservative projection, and half that of BCG’s conservative estimate.

Tokenised funds – 2030 global AUM projections ($ billion)

|

|

Conservative |

Neutral |

Bullish |

|

Amundi |

30 |

120 |

300 |

|

BCG |

600 |

1000 |

1300 |

|

McKinsey |

300 |

600 |

1200 |

Source : Amundi BI / BCG / McKinsey

Amundi is also conservative about the potential revenue that tokenised funds could generate for the asset management industry by 2030. Its most optimistic estimate is $3 billion – well below the equivalent projections from McKinsey ($12 billion) and BCG ($13 billion). So why is Amundi bothering? In essence, it believes that the major growth spurt in tokenised funds may not begin until after the end of this decade. In the words of the report’s author: “Whereas the revenues to be generated from tokenised funds in the short term may be underwhelming, asset managers that look beyond the horizon line and that prepare for an on-chain world that is already in the making may well end up on the winning side of the industry.”

Can tokenised funds become a trillion-dollar market?

In order for global tokenised funds’ AUM to break through the $1 trillion threshold – as McKinsey’s bullish model and both BCG’s neutral and bullish projections anticipate by 2030 – Amundi thinks that traditional institutions (banks, fund platforms and brokers) will need to incorporate digital assets directly into their client offerings. Amundi does not predict that this transformation will happen fastest in Europe, or even in the US. The report envisages that, while the US has a head start in the tokenised fund space, the greatest future growth will come from digital natives in Asia. As much as 58% of the world’s digital wallets are based in Asia, according to recent analysis from Triple A, a crypto payment service provider.

Crypto readiness is seen as an important precursor to the adoption of tokenised funds: as Amundi says, “investors that are the most likely to proactively invest in tokenized fund assets are the ones that will be most familiar with the crypto environment, and for which the learning curve for token investing will be the shorter.” Amundi expects that a portion of the global $4 trillion crypto market cap will migrate into tokenised funds as these crypto-savvy digital natives derisk their holdings, without wanting to move off-chain. “On-chain investors will eventually demand an entirely on-chain experience,” said the report’s authors. “And like traditional off-chain investors, they will want to diversify their portfolio, but without going back to the off-chain world.” This process will also see the digital assets industry become less exclusively the preserve of professional, US-based investors, a demographic that currently dominates the space. It is notable how concentrated the global tokenised fund market currently is: BlackRock’s tokenised US Treasury fund, BUIDL[5]AUM. But assuming continued development of cryptocurrencies and a supportive regulatory environment, Amundi predicts that the next decade could see digital assets “break the technical ceiling limiting them to the digitally native community and become a usual, non-exotic way of trading assets”. That, it suggests, could push the market for tokenised funds into the realms of trillions of dollars.

Why (and why not) tokenise a fund?

It’s common for the stated benefits of tokenised funds (and other RWAs) to centre on operational efficiency gains and cost improvements. Amundi’s report, though, argues that this is an inward-looking perspective on the part of the asset management industry and overlooks key benefits for consumers. According to Amundi, the main benefits of tokenised funds for investors are instant order execution, expanded access for a more digitally-focused generation of investors, and 24/7 operability.

But tokenised funds also bring particular challenges. One of these, highlighted by the Investment Association[6], pertains to dispute resolution and governance. Decentralised ledgers could expose funds to 51% attacks (in which a single entity gains control of a network’s majority hashing power, potentially enabling it to alter previous transactions and block new ones).

There is also the challenge of implementing robust know-your-customer (KYC) protocols for tokenised funds. While tokenised funds offer many advantages on this front (wallet-based identity verification, on-chain wallet address whitelisting for access control, and the potential for KYC portability across platforms), pseudonymous blockchain wallets could also be used to finance illicit activities. This means that tokenised funds need KYC to be built in at the protocol level.

What’s happening with UK regulation of tokenised funds?

In the UK, the industry is seemingly aware of the potential for a future in which a new generation of investors demands on-chain access to their assets, but is also looking closely at how to address the challenges this raises. Regulators and industry bodies have been fine-tuning the infrastructure that will support tokenised funds since 2023. A report published in November that year[7] by the Technology Working Group (part of HMT’s Asset Management Taskforce) proposed a staged progression from trad-fi funds towards a fully distributed ledger technology (DLT)-based fund ecosystem, beginning with a baseline or ‘stage one’ model. This proposed only one significant change from a traditional investment fund: the deployment of DLT for fund registry and transactions, with a private, permissioned chain serving as the master record for the fund unit register. Crucially, fund unit transactions are settled off-chain, via the authorised fund manager, as with traditional funds.

“It needs to enhance provision in some way: make things cheaper, or quicker, or increase choice, or enable something that just can’t be done today,” said Walls. “Done right, we believe that tokenisation can do this.”[8] The Technology Working Group published its second report[9] in March 2024. This highlighted three key steps for the next stages of fund tokenisation: enabling on-chain fund settlement using digital money; enabling funds to hold tokenised assets in their portfolios; and expanding the scope to use public permissioned networks. The regulatory environment will continue to evolve; the FCA closed a consultation in February, whose goals included discussing future tokenisation models that use DLT to provide tokenised portfolio management at retail scale, with the results to be announced in due course.

“There are many things that firms can do under our existing rules and more that become possible with the changes we propose enacting now,” said Walls ahead of the consultation. “We stand ready to design the next stage with the industry.”

[1]https://www.hermes-investment.com/uk/en/intermediary/press/federated-hermes-partners-with-archax-to-offer-tokenised-ucits-money-market-funds/

[2]https://capitalpioneer.co.uk/revealed-first-uk-tokenised-fund/

[3]https://www.avivainvestors.com/en-gb/about/company-news/2026/02/aviva-investors-seeks-to-tokenise-products-with-ripple/

[4]https://about.amundi.com/files/nuxeo/dl/4c73d033-5b89-439b-b702-e4851bd8eec4?inline=

[5]https://uk.finance.yahoo.com/news/blackrock-takes-first-defi-step-145710525.html

[6]https://www.theia.org/sites/default/files/2021-09/Tokenised%20Funds%204%20-%20Disputes%20considerations.pdf

[7]https://www.theia.org/sites/default/files/2023-11/UK%20Fund%20Tokenisation%20-%20A%20Blueprint%20for%20Implementation.pdf

[8]https://www.theia.org/sites/default/files/2025-11/Bridging%20the%20Adoption%20Gap%20-%20Aligning%20Digital%20Asset%20Offerings%20with%20Buy%20Side%20Requirements%20%20Nov25.pdf

[9]https://www.theia.org/sites/default/files/2024-03/Further%20Fund%20Tokenisation%20-%20Achieving%20IF3%20Through%20Collaboration%20%20Mar24.pdf

On-chain assets ‘worth $10trn by 2030’

By Damien Black

Tokenization is not here to augment the way we do business – it represents a fundamental reordering of the investment world. And the new industry could command digital assets worth as much as $10 trillion by the end of the decade. That’s the verdict from one of the advocates of distributed ledger technology.

Nick Mersh is a portfolio manager at Canadian brokerage Purpose Investments who looks after funds that include tech stocks such as Tesla, Microsoft and Amazon. He also believes that blockchain-assembled investment vehicles are a near-future reality – and by 2030, this online, or rather on-chain, industry will be worth trillions.

Growing strong: predictions looking rosy for tokenized assets

“We have to restart from a perspective of thinking about doing this on-chain first,” he says. “Tokenization is not really this incremental feature layered on top of capital markets but a structural reset of the market’s core rails, around issuance, custody, trading, settlement, collateralization and compliance.”

Key technological breakthroughs – for instance, cash-like instruments that use stablecoins – will signpost the way towards a brave new world where natively assembled on-chain asset classes become the norm.

“This will provide the transaction and settlement layers upon which further technology can be built,” he says. “Over the next five-year period the biggest shift is not just more crypto assets, but new institutional products getting designed on-chain first, and then secondarily wrapped into that legacy distribution.”

Too good to dismiss

Simply put, the traditional system of ledger settlements is too clunky not to be superseded by a fully evolved tokenised system. “The reason that this is structural and not incremental is that if you think about traditional capital markets, the system still relies on multiple ledgers,” Mersh explains. “Brokers, custodians, and clearing houses still need a lot of reconciliation workflow [which leads to] delayed settlement in terms of the individual transactions, and what tokenization really introduces is a different architecture.”

Think a shared ledger with programmable transfer rules, with the potential for cash and assets to be settled together as one package rather than separately. “This matters because it changes the economics of time, capital and operational friction, and there are a lot of advantages that drive the structural framing,” says Mersh.

Essential core components

Mersh envisages three essential components or stages to building the new ecosystem of on-chain investing. The first of these consists of public blockchains like Ethereum, which offer the deepest liquidity, strongest security, and very rich developer ecosystems. Institutional investors are already using these with permissioning, identity layers, and regulated custody.

“But the next bucket is a permissioned or consortium network built specifically for regulated participants,” he says, a process he warns will entail exchanging “some decentralisation for control, privacy, and compliance”. He adds: “That matters when you're dealing with these large equity markets.”

The last component is what Mersh refers to as “hybrid or interoperable models”, which is what he believes the ecosystem is ultimately going towards. These models would allow assets to be issued on one chain, but then settled on another, and bridged across systems depending on the use case. At that point, blockchain becomes the new normal of investing.

“What really matters here is standardisation, interoperability, legal certainty – and maybe not maximal decentralisation,” says Mersh, suggesting a compromise will have to be reached between freedom and privacy on the one hand and regulation and security on the other.

“Because when institutions say ‘on-chain’ they don't mean just ‘one chain’ – they mean these programmable settlement rails that meet a lot of these regulatory standards.”

Tokenized assets at a glance

What’s the bottom line?

That’s a lot to digest, so I push him on a prediction. Late last year Mersh went on the record as saying tokenized assets could be a “multi-trillion dollar” market by 2030. But that seems a tad vague to me. How much does he mean really?

“I think putting it into the five-to-ten trillion range in the next couple years is a reasonable estimate,” he says without blinking. The first wave of this monetization will be stablecoins and tokenized cash-like products. “That market the entire system is built upon is huge. So you talk about that figure, you're looking at short duration in government bonds or money market funds, which are well into the tens of trillions of dollars.” Mersh thinks the second wave will be tokenized funds that share asset classes and ETF units.

“So you’re talking about an even larger investment market when it comes to trillions of dollars overall in that ecosystem. And then you'll get native tokenized equities. And if you think about the market caps of some of these companies right now – Nvidia is over $5 trillion, and Google yesterday touched over $4 trillion. If you get tokenised assets, accessing that you can see just how much dollar-figure amounts will accelerate.”

Speed and efficiency

What are the other core benefits Mersh sees in tokenization? Faster transaction settlements, turning days into “near instant, which reduces counterparty risk and really frees up capital and balance sheet capacity”. This will really appeal to institutional investors, he adds. “The real prize here is not novelty, it’s balance-sheet efficiency, a lower operational risk, and the ability to mobilize liquidity with a lot less friction.”

“Once assets are sharing a digital and interoperable format, they can plug into these new workflows, so real-time collateral, automated rebalancing, on-chain repurchase, and eventually more continuous portfolio execution,” says Mersh. “And this is really where tokenization does begin to look less like this financial product innovation and more like this new operating system for the plumbing around markets themselves.”

Democratised?

Capital markets that have up until now been restricted to institutional investors like BlackRock or J.P. Morgan could be opened up to smaller retail investors, because tokenized assets can be reduced to the tiniest of fractions. A classic example of this is Bitcoin, where $1,000 can buy you BTC0.000011. “Absolutely, I think that adoption by institutions is the starting point in mass adoption,” says Mersh, a process he describes as “the democratization of individual asset classes”.

He adds: “Tokenization has this appeal intuitively if you think about fractional ownership, broader distribution, and then also potential secondary transferability. Because if you look at some of these asset classes, what you have from a lot of these funds is they're extremely illiquid and have trouble getting those secondary markets going.”

Tokenization: gateway to hidden markets?

Mersh believes tokenization could open up previously inaccessible markets to investors in countries that have hitherto been locked out of global capital markets. “It’s very hard if you’re somewhere in Venezuela or Turkey or Argentina to buy, say, an Apple stock directly, right? So, what this does is it really opens up not only those pockets of the market but it democratizes a lot of these different asset classes available on brokerage accounts in the U.S.”

If the prospect of assets being available beyond the traditionally ring-fenced preserve of what Mersh calls “guarded institutions” sounds far-fetched, there is already a precedent – of sorts. Mersh points to the U.S. equity market, where the largest share is held collectively by individual households. That’s true up to a point – American households hold 40% of equities, though the top tenth of those hold the lion’s share. Retail investors won’t be the only beneficiaries, of course. Even larger players sometimes struggle to secure assets in less accessible regions of the world. Tokenization could see those hard-to-reach stocks opened up to the wider world too.

“If I’m looking at investing in certain companies in China or I want to get involved in a semiconductor company in Taiwan, I have the best trading and operational capabilities in-house here – but I still can’t access some of these markets [because] of the hurdles that are proven there,” says Mersh. “Tokenization unlocks that in a big way.”

Events on our radar:

- Digital Assets Forum Abu Dhabi launches on 13 May 2026, bringing together banks, asset managers, regulators, and digital asset leaders to discuss tokenisation, market infrastructure, and institutional adoption across the Middle East and global capital markets - tickets HERE

- Bitcoin 2026 – Las Vegas, 27-29 April - premier Bitcoin ecosystem event – tickets HERE

- DigiAssets Connect Zurich, 16-17 June - Custody, banking, and institutional infrastructure – tickets HERE