Tokenised investment funds are being woven into the fabric of global finance at extraordinary speed. The oversight is struggling to keep up.

by Anna Fedorova

At the Federal Reserve’s inaugural Payments Innovation Conference in Washington in October, Governor Christopher Waller told delegates to “embrace the disruption” coming from digital asset technology. He said that distributed ledgers and crypto-assets are “no longer on the fringes”, but instead “increasingly woven into the fabric of the payment and financial systems”. In the months that followed, he has continuously been proven correct.

However, what Waller didn’t address in his speech – and what remains in question – is whether digital assets could cause this fabric to tear and what would happen to financial stability if so. As tokenised assets continue to swell and become more intertwined with the incumbent financial ecosystem, this question is becoming more pertinent, particularly with regard to tokenised investment funds. In simple terms, these are shares of traditional mutual funds, such as money market funds (MMFs) or government bond funds, represented on a blockchain as tokens. Having started as a niche fintech experiment, tokenised funds have grown to over $10 billion in assets under management (AUM) in less than two years.

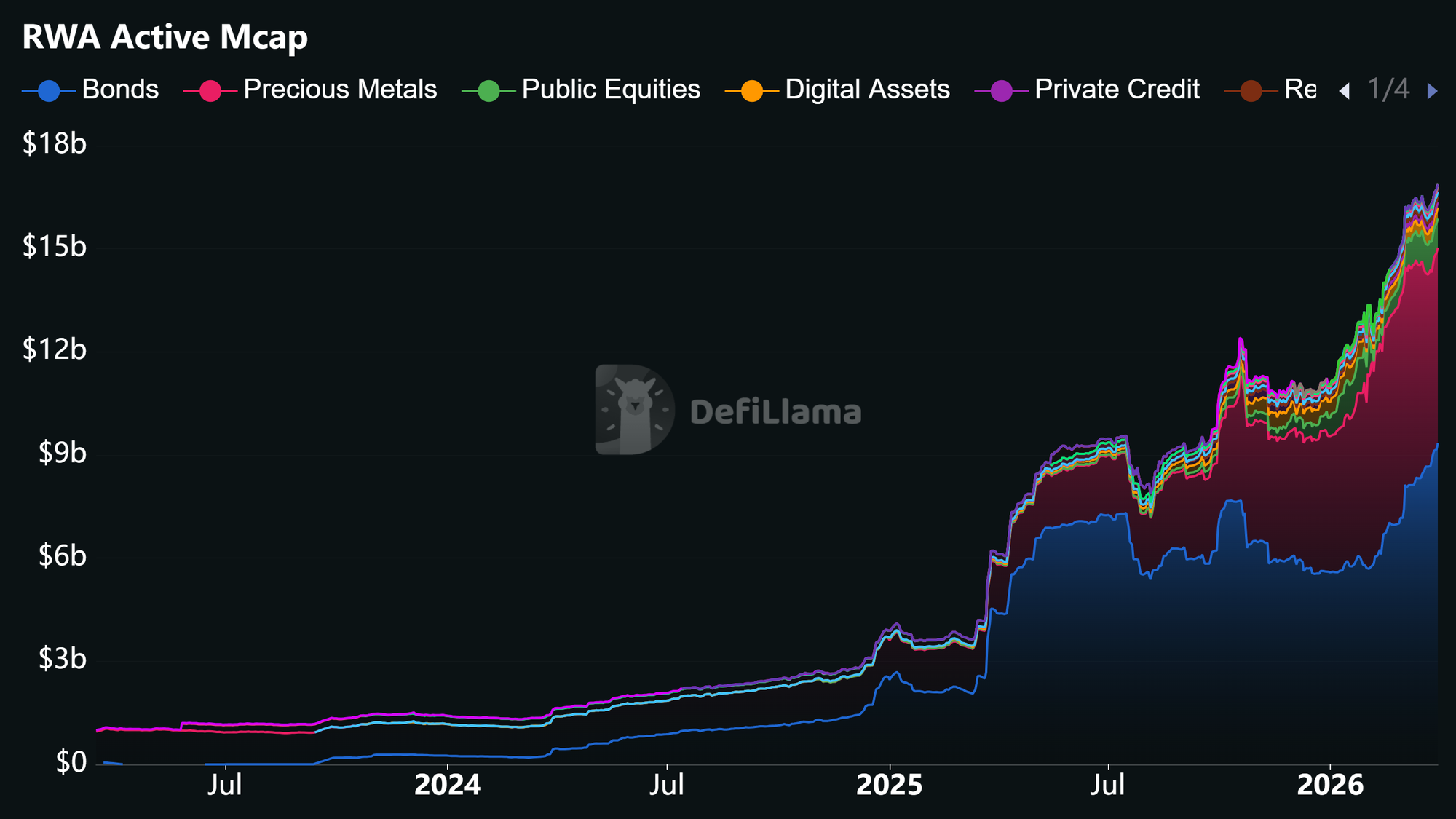

RWA Active MCap 2026-03-31

Among them is BlackRock’s BUIDL behemoth, with an on-chain market cap of nearly $3 billion, and the $900 million Franklin OnChain US Government Money Fund (BENJI), blockchains. Last July, Goldman Sachs and BNY Mellon also launched a tokenized money market funds solution. And more developments have been rolling in this year: intraday trading its tokenised money market fund, and so on. No one can call this niche anymore. And that’s precisely why now is the time to talk about the risks.

Why tokenise at all?

The tokenization of funds brings real benefits. Their shares can be used as collateral for margin calls, transferred peer-to-peer outside of normal trading hours, and even used as a settlement asset, all the while still earning interest in the background. In the digital asset space, people like to call this “rehypothecation”.

And this is a potentially huge advantage for institutional investors and treasury managers. Lucas Outumuro, VP of Institutional DeFi at Sentora, explains that while “in traditional markets, capital is effectively ‘parked’ between settlement windows, on-chain, that same capital can be continuously reallocated, rehypothecated or used as collateral in real time”. He says this therefore “opens the door to strategies that optimise for capital efficiency rather than just asset allocation”. For now, tokenised funds are an admittedly tiny part of the wider mutual funds market, with US funds alone holding $23.5 trillion in AUM as of Q4 2025. But if they continue to grow as quickly as they have been, the potential for disruption really is as big as Governor Waller says.

The concentration problem

There is, however, a catch. Though institutional interest in these products is clearly building, this remains an intimate gathering rather than a house party. And in finance, intimate gatherings are not always a good thing. The tokenized equities landscape, for example, is currently dominated by two protocols – Ondo and xStocks – that control 76.4% of total market value, according to a report by Sentora. Investment in the actual funds is also equally concentrated. According to the Bank for International Settlements (BIS), around 90% of the total holdings in both BlackRock’s BUIDL and WisdomTree's WTGXX funds are in the hands of just four wallet addresses.

Outumuro says this concentration is a feature of early adoption, but concedes that it introduces both counterparty and liquidity risks, which investors are not used to underwriting in public markets. He says: “The risk is not concentration itself, but how that concentration interacts with liquidity. If a small number of holders can materially move markets or withdraw collateral quickly, it creates fragility that traditional fund structures are specifically designed to avoid”. In simple terms, what Outomuro is saying is that it’s a catch-22. Participation remains low because the risks are poorly understood, which in turn exacerbates the risks.

When is a bank run not a bank run?

This is far from the only potential risk, though. Across the board, the features that make tokenised funds attractive – the transparency, instant settlement, 24/7 trading – all create a risk profile that is yet to be tested in real-life scenarios. Take transparency, for example. In traditional funds, investors may not even learn about redemptions until the fund reports at the end of a month or quarter. On the blockchain, withdrawals can be seen immediately by anyone.

The Federal Reserve Bank of New York, in a September 2025 research paper on the financial stability implications of tokenized funds, flagged this as a key concern, saying that blockchain transparency “acts as a coordination device among investors”. The paper’s authors warn that “round-the-clock trading and settlement may speed up a run on an investment fund, if disruptions in the market for tokens outside normal market hours escalate”. Once redemptions start, panic may soon follow – and suddenly an orderly queue for the exit becomes a stampede. And with no closing bell, there’s no natural pause for investors’ emotions to take a breather.

Stress testing a run

A run scenario can create several potential problems. Firstly, it’s questionable whether all redemption requests could even be met. That’s because while tokens settle instantly, the underlying assets don’t. US Treasuries, for example, still clear on T+1, as does the majority of the financial system. This is a risk the BIS highlights in its November 2025 Bulletin. If everyone rushes for the exit, the question is whether tokenised funds could face the same constraints as open-ended property funds in the UK after Brexit, or private credit funds this year.

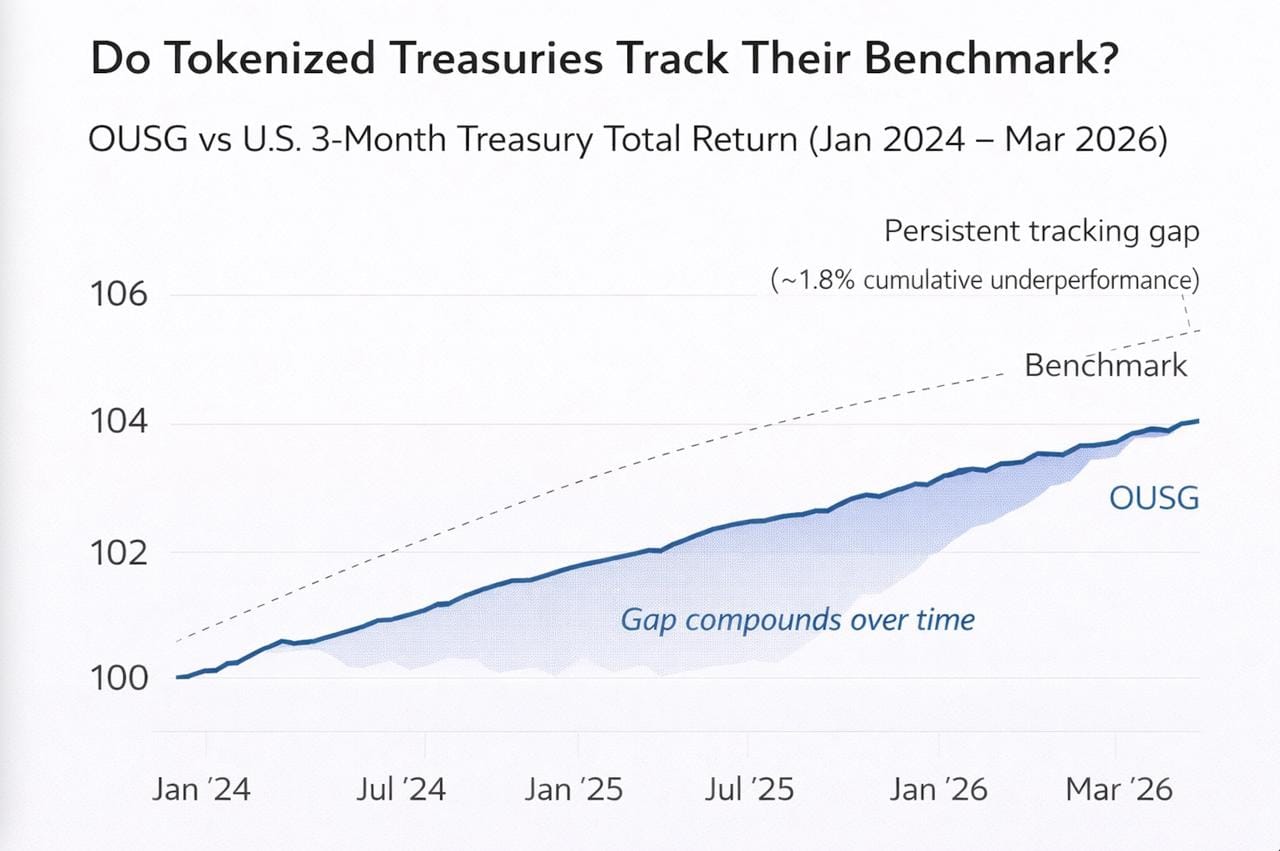

Secondly, under stress, the gap between tokenised funds and the underlying assets they track could widen, even if this divergence is relatively negligible right now. Jason Rowlett, founder of RWA data platform Foretoken, points out a consistent gap between tokenised treasuries and the underlying benchmarks they track, for example.

Foretoken - Tokenized Treasury Fund vs Benchmark

“For institutional investors, that distinction matters,” he says. “Tokenised assets should be evaluated based on how faithfully they track their benchmarks, not just their standalone returns”, adding that this represents “a clear example of basis risk in practice”.

And finally, the interconnectedness of the tokenised ecosystem could exacerbate a run, according to the New York Fed’s paper: “In times of stress, tokenized shares might amplify the systemic impact of a run on an investment fund if tokens are used to meet margin calls while also being used as a reserve asset for other financial products.” In other words, if the same token is simultaneously used as someone’s margin collateral and someone else’s reserve asset, the impact could be stacked.

The great regulatory divide

But while researchers are sounding the alarm, regulatory oversight of the space has loosened rather than tightened. The US Financial Stability Oversight Council – the body created after the 2008 financial crisis to identify systemic risks before they become crises – removed crypto and digital assets from its list of financial vulnerabilities in its December 2025 annual report. They were reclassified as “significant market developments to monitor”. The SEC and CFTC, meanwhile, have made a complete U-turn on their previously restrictive policies. CFTC Acting Chair Caroline Pham publicly said last September that “the public has spoken: tokenized markets are here, and they are the future”, while SEC Chair Paul Atkins echoed the sentiment when he described the new regulatory agenda as “a golden age of financial innovation on US soil”. There are certainly reasons for this optimism, which are widely acknowledged. However, the BIS and the IMF don’t appear to share it.

IMF Monetary and Capital Markets chief Tobias Adrian said in October that it’s “paramount to make sure regulations keep up with the growing role of non-bank and digital assets, especially as new risks emerge in areas like stablecoins and foreign exchange markets”. Similarly, London Business School Professor Hélène Rey, wrote in the IMF’s Finance & Development journal in September: “Major financial stability risks, including increased volatility in exchange rates, threats to public finances in many economies, and competition across currency networks are likely”.

The NY Fed paper, meanwhile, notes a detail almost in passing that should give every traditional investor pause: the largest tokenised fund in the market, BlackRock's BUIDL, operates as a private fund. That means it’s exempt from the disclosure requirements and liquidity risk management rules that apply to registered money market funds. And so, as the paper notes, regulators and the public have “little visibility into their operations”.

What to watch

These funds were born into an era of plentiful liquidity, near-zero rates, and a broadly risk-on environment. None of the major products have been tested by a real stress event to date. We simply don’t know how a major sell-off might impact funds that are simultaneously used as collateral, settlement instruments and reserve assets for stablecoins. We don’t know how wide the liquidity gap could become at scale. And we don’t know if the transparency of on-chain redemptions would indeed cause widespread panic, or actually aid price discovery.

What we do know is that the tokenised assets sector roughly tripled in size in 2025 alone, regulatory constraints are loosening, and the only institutions currently asking the hard questions about systemic risk are those with no jurisdiction to take action. That is not necessarily a reason to avoid tokenised funds. However, it is a very good reason to understand exactly what you're holding, who else is holding it, and how quickly you could get out if things went wrong.