by Anna Fedorova

Swift has announced a new blockchain-based “universal” ledger, built with Consensys, as it scrambles to stay relevant in a world where stablecoins are exploding and near‑instant crypto payments are starting to outshine traditional bank rails. The idea isn’t to replace Swift’s existing network, but to bolt on a compliant, interoperable blockchain layer using ISO 20022—though big questions remain.

On 29 September 2025, at the SIBOS Conference in Frankfurt, Swift – the global financial messaging network that enables payments for more than 11,500 financial institutions – announced its foray into blockchain, with plans to launch a “universal” digital ledger to enable what it calls “always-on cross-border payments”.

It’s undertaking this initiative in partnership with Consensys – a leading crypto infrastructure player that, among other things, runs the ecosystem’s most widely used digital wallet, MetaMask. Consensys has spent years adapting Ethereum-based infrastructure for enterprises and regulated financial institutions, including JPMorgan Chase and Société Générale. As such, it is no stranger to institutional integrations or payments, so this choice of partner makes sense for Swift’s blockchain move.

What’s more interesting is the motivation behind it – and to understand it, we need only to look at the relentless rise of stablecoins and the uproar this has caused in the banking sector. Over recent weeks, crypto exchanges and banks in the US have been locked in a stalemate over whether crypto firms should be permitted to pay interest on stablecoins under the Clarity Act currently being hashed out. Banks argue that high yields on stablecoins could threaten traditional bank deposits, with the US Treasury predicting deposit flight could reach trillions of dollars.

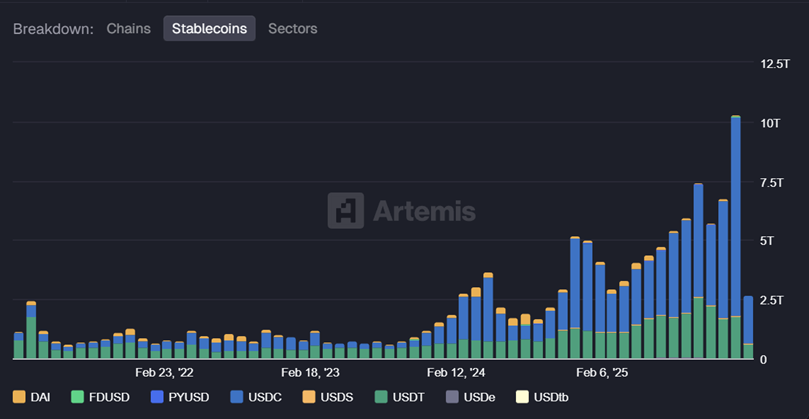

Meanwhile, stablecoin transaction volume rose 72% in 2025 to $33 trillion, and then skyrocketed to $10 trillion in January 2026 alone, according to data from Artemis Analytics. While still small compared to Swift’s $150 trillion in annual transactions, stablecoins are quickly becoming a force to be reckoned with.

Stablecoin transaction volume growth (Source: Artemis Analytics) Stablecoins | Artemis Terminal

Rising to the challenge

Against that backdrop, it’s no wonder banks are looking to remain competitive – and this means upgrading existing infrastructure. Announcing the blockchain ledger at the Sibos conference, Swift’s CEO Javier Pérez-Tasso was clear: “Banks are ready for it and they’re asking us to play a bigger role”. And Swift appears to be ready to rise to the challenge. However, to say Swift is keeping the details of its blockchain bid tightly under wraps would be the understatement of the century. While some details have emerged since the announcement more than four months ago, they’re few and far between.

In an interview with Bloomberg about the Swift project, Joe Lubin, CEO and founder of Consensys, watched every word carefully and offered little beyond what was already in the press release. He was, however, clear that sentiment toward digital finance had changed "significantly" since the early days of Ethereum – of which he is a co-founder. Back then, the idea of TradFi and DeFi working together was a pipe dream.

“The vibe in Frankfurt [at the 2025 Sibos conference] was very different,” Lubin said. “And the feedback we…and the Swift leadership have heard from banks is very positive. It’s basically about time for TradFi to merge, or make use of, DeFi.”

The facts

What we do know is that Swift is building a blockchain-based shared ledger that will combine with its existing messaging and APIs, following ISO 20022 – the global standard for structuring and exchanging financial messages. It aims to facilitate real-time 24/7 cross-border transactions, supporting what it calls the “trusted movement of tokenised value”.

During his opening speech at Sibos 2025, Pérez-Tasso made it clear that Swift isn’t planning to replace its existing rails with blockchain technology, but rather to add a new feather to its cap. He called this approach a combination of "rejuvenation and innovation” – developing the system along two parallel tracks that have “one foot in the past and one in the future”.

“I hear a lot of noise out there that the industry needs to do away with existing rails and replace everything from scratch. But I don’t think we need to throw out the baby with the bathwater,” he said. “It’s not either or, it’s definitely both.”

According to Swift’s CEO, today, 75% of payments on the Swift network reach their end beneficiary banks within 10 minutes. But in the world of near-instant stablecoin payments, this is no longer enough. So this is one area he plans to tackle with the integration of blockchain technology.

Ultimately, though, Swift’s blockchain initiative is less about making payments faster, and more about preserving its role as the neutral coordinator of global finance in a world where coordination is no longer guaranteed. It aims to record, sequence and validate transactions via smart contracts in a way that is interoperable with both existing financial infrastructure and the emerging financial economy.

However, Swift doesn’t intend to build its own blockchain or issue its own digital assets – its focus is solely on the infrastructure side. Industry reporting suggests Swift’s prototype may be running on Consensys’s Linea blockchain – an Ethereum Layer-2 network focused on faster and cheaper transactions.

The Holy Grail of crypto

In the months since the announcement, Swift has made some practical progress. In December, it announced a proof-of-concept for cross-border transfers of tokenised deposits, in collaboration with Ant International and HSBC. This showed that, with ISO 20022, the transfer of tokenised deposits can plausibly scale beyond random one-off experiments into something akin to the existing global banking system.

Then, in January, Swift completed what it called a “landmark digital asset interoperability trial” with BNP Paribas Securities Services, Intesa Sanpaolo, and Societe Generale, demonstrating that the seamless exchange and settlement of tokenised bonds were possible using both fiat and crypto payments. Its goal is clear: to solve the fragmentation problem that has plagued the digital assets space since its inception, paving the way for a unified financial system.

As Swift’s Thomas Duguauquier, tokenised assets product lead, puts it: “By proving that Swift can orchestrate multi-platform tokenised asset transactions, we’re paving the way for our members to adopt digital assets with confidence, and at scale. It’s about creating a bridge between traditional finance and emerging technologies.”

But it’s important not to underestimate how tall an order this is for an ecosystem where even interoperability between different blockchains remains the illusory Holy Grail. Crypto has struggled with interoperability since the moment there was more than one blockchain.

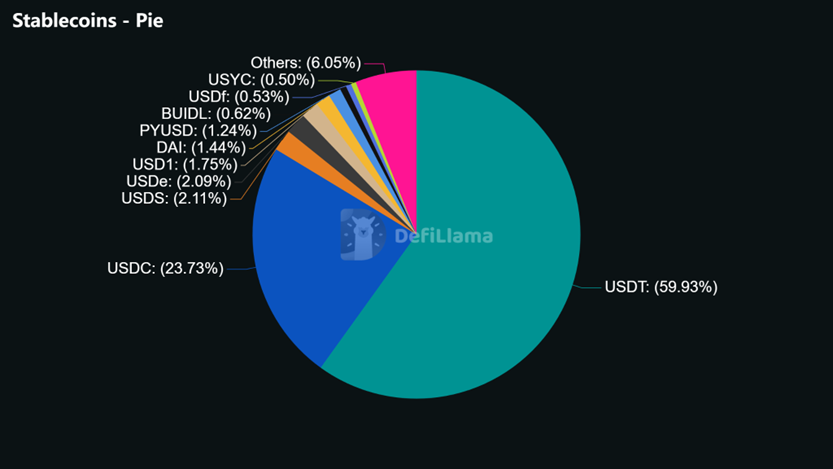

For example, you can’t simply send a USDT stablecoin issued on Ethereum to Solana without relying on mechanisms such as swaps, cross-chain bridges, or intermediaries. This quickly undermines one of the key benefits of stablecoin transfers.

Stablecoins: by type (Source: DeFi Llama)

Fragmentation & regulation

If Swift can truly solve this issue by providing infrastructure that allows financial institutions to move all types of digital assets across the globe using both fiat systems and blockchain, that would be nothing short of groundbreaking. But it will likely face many challenges along the way.

It’s not just the technology that is fragmented – it’s also the regulatory landscape. A global blockchain ledger will have to meet the requirements of jurisdictions worldwide with very different attitudes toward blockchain technology, many of which haven’t finalised their frameworks yet. This may well be a major headwind.

Some in the industry disagree. Nick New, co-founder and CEO of Optalysys, argues in a blog that the calibre of institutions involved in this project, including banks like HSBC, JPMorgan and Deutsche Bank, will encourage regulators to review their rules or propose new, supportive legislation.

This may well be. In fact, Swift says it has already submitted a proposal for new market practice guidelines to the Securities Market Practice Group (SMPG). But regulatory changes typically take time, and time isn’t necessarily a luxury Swift has.

When asked by Bloomberg about a potential timeline for the rollout of this new ledger, Joe Lubin chose to remain silent, and Swift hasn’t been forthcoming with a detailed plan. Realistically, it will take years for this to move from the experiment phase to a finished offering. In that time, competition from existing stablecoin rails will no doubt intensify.

From pilot to success

This brings us full circle to the question of revenue. Just as with the rollout timeline, Swift hasn’t yet explained how this new blockchain layer will be monetised. Does it consider this a necessary investment to remain relevant in a rapidly changing landscape? Or will this be a premium service available only to a handful of major banks that work with Swift?

The latter would certainly be easier to implement on a single, permissioned blockchain. Although even then, the trillions of dollars in institutional flows across the globe would test such a blockchain to its limit. But if this universal ledger is limited to a select few participants – which I suspect it will be at least to start with – how long will it be before the benefits are passed on to the average user of the Swift network, whether small businesses or individuals?

For the project to be declared a success, these questions must be clearly answered and the beneficiaries clearly defined. That’s because for this to move from controlled pilot to universally used infrastructure, commercial incentives must align for all participants. If Swift’s move is seen primarily as a defensive response to the growth of stablecoins, rather than as a value-creating initiative, adoption may stall even if the technology doesn’t.

In practical terms, success would mean Swift moving from controlled pilots to a live production corridor with real volume, real liquidity, and clearly defined governance, before stablecoin-native rails become the default for cross-border settlement.

On the technology front, Swift’s plan relies heavily on universal adoption of ISO 20022. And so far, this adoption remains uneven – especially when it comes to smaller banks. If banks continue relying on legacy internal formats, this could also slow the scalability of Swift’s new model.

Not only that, but banks and other institutions will have to agree on a wide range of governance questions: from who sets the rules and settles disputes, to how smart contracts are updated. And there are many cooks in this kitchen – each of Swift’s 30 bank partners has its own risk appetite and commercial priorities.

But none of this will matter if regulators can’t agree on a consistent global framework for tokenised assets. Especially given Swift’s explicit emphasis on a compliance-first design. While it can influence regulatory decisions, it can’t force regulatory alignment – and this may well end up dictating the timeline.

{kind=link}