Welcome to the tenth letter from TheIntersection team. We hope you are enjoying this weekly letter. Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: IMF worries about DeFi

- Data: Stablecoin flows in Q1 in emerging markets

- Analysis: The $10 Billion Product Nobody Has Stress-Tested

- Opinion: The Last Bitcoin

- Our weekly events round-up

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

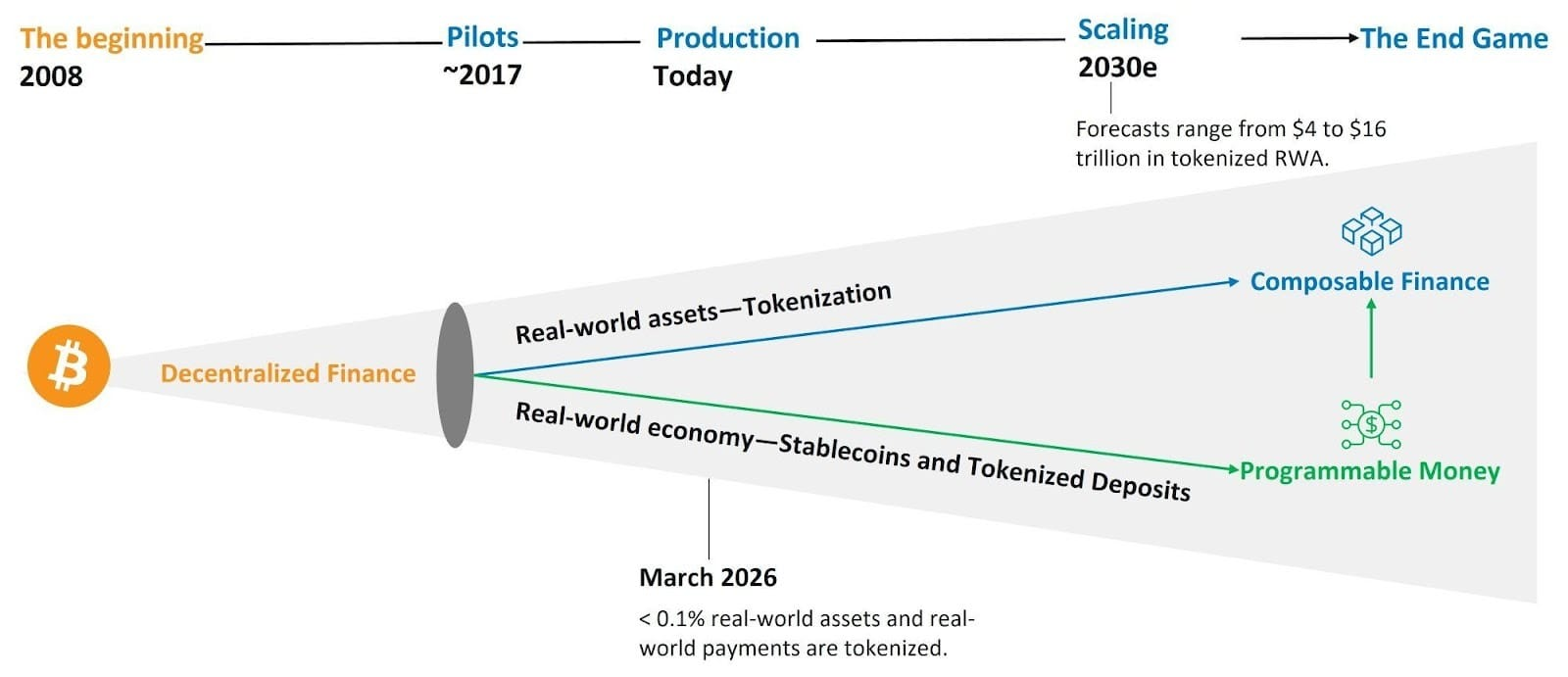

Quick opening thought: As of April 2, 2026, the RWA segment reached $27.65 billion, a c.4% increase over the last 30 days. U.S. Treasuries remain the dominant asset class, accounting for nearly half of that value ($12.78 billion).

News in Brief

Centralised exchanges race to dominate tokenised asset access

A new industry overview highlights how centralised crypto exchanges are becoming the primary gateways for buying and trading tokenised real-world assets in 2026. Platforms such as Change NOW, Kraken and others are expanding support for RWA tokens across multiple blockchains, offering faster swaps, cross-chain access and simplified onboarding for investors. At the same time, regulatory clarity ( particularly in regions like the EU under MiCA ) is helping exchanges scale these offerings within compliant frameworks. Why it matters: As tokenisation grows, distribution is becoming the battleground. Exchanges ( not issuers ) are increasingly controlling access, liquidity and user adoption for tokenised assets.

Tokenisation moves into real-world financial products A new report from Celent highlights tokenised money market funds and programmable money as the most mature institutional use cases, with major global banks already participating. Why it matters: The focus is shifting from experimental pilots to production-ready financial products embedded in existing banking workflows.

BlackRock brings tokenised Treasuries into DeFi trading BlackRock and Securitize have integrated the BUIDL fund with UniswapX, allowing institutional investors to trade tokenised Treasury shares on-chain via a request-for-quote model. Why it matters: This marks a major step in bridging regulated financial products with DeFi liquidity infrastructure.

Legal clarity improves for digital assets in the U.S. New amendments to the Uniform Commercial Code (Article 12) are coming into force across key states, including New York, providing clearer legal treatment for digital assets used as collateral. Why it matters: Legal certainty is a key enabler for institutional adoption, particularly in lending, repo and collateral markets.

Deep Dive - IMF warns tokenisation could amplify the next crisis

The Top Line?

Tokenisation may make markets more efficient — but it could also make financial crises unfold faster and harder to contain.

The International Monetary Fund is sounding a clear note of caution just as tokenisation moves into mainstream finance. In a recent report, IMF officials warned that shifting core market infrastructure onto blockchain rails could accelerate financial crises beyond regulators’ ability to respond.

Tokenised markets compress that timeline dramatically. Stress events could propagate in real time, leaving less room for discretionary intervention. Automation adds another layer of risk. Smart contracts and algorithmic triggers can enforce liquidations or margin calls instantly, potentially creating feedback loops that amplify volatility. What used to unfold over days could play out in minutes.

There are also structural concerns. Tokenisation often relies on shared ledgers and concentrated infrastructure, meaning that failures or disruptions at key nodes could have system-wide consequences. At the same time, stablecoins (increasingly used as settlement assets ) may be vulnerable to run dynamics if confidence breaks down. None of this means tokenisation is inherently destabilising. The IMF acknowledges its benefits: lower costs, reduced settlement risk and greater transparency. But the trade-off is clear: efficiency comes at the cost of resilience.

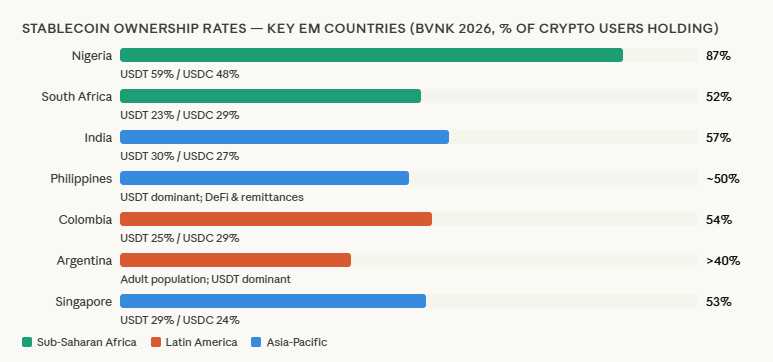

Q1 Sstablecoin flows in emerging markets

USDT vs USDC as a policy signal. The split between the two is now a real-time readout of institutional trust. USDT goes where dollar access is scarce and regulation is light. USDC follows the regulatory perimeter - and as the GENIUS Act embeds itself in institutional workflows, its EM share will grow wherever local frameworks allow it.

Brazil is the most consequential regulatory moment. Brazil's Central Bank classified all fiat-referenced stablecoin transactions as foreign exchange operations from 2 February 2026, with mandatory capital markets reporting beginning 4 May 2026, in a country where, per BCB data, around 90% of crypto transaction volume is stablecoin-driven. It is effectively a decision to bring a shadow dollar economy into the formal financial system.

Nigeria is the canary. 87% of Nigerian crypto users have recently used stablecoins (the highest rate globally), with 59% holding USDT and 48% holding USDC.

The IMF is paying attention (see News above). A March 2026 IMF working paper documented spillovers from stablecoin-based FX to traditional currency markets, and Goldman Sachs and the IMF have both flagged that if users shift savings from domestic banks into stablecoins at scale, central banks may lose control over monetary policy and capital flows. That tension between utility and systemic risk is the defining policy debate for EM stablecoins in 2026.

The $10 Billion Product Nobody Has Stress-Tested

Tokenised investment funds are being woven into the fabric of global finance at extraordinary speed. The oversight is struggling to keep up.

by Anna Federova

At the Federal Reserve’s inaugural Payments Innovation Conference in Washington in October, Governor Christopher Waller told delegates to “embrace the disruption” coming from digital asset technology. He said that distributed ledgers and crypto-assets are “no longer on the fringes”, but instead “increasingly woven into the fabric of the payment and financial systems”. In the months that followed, he has continuously been proven correct.

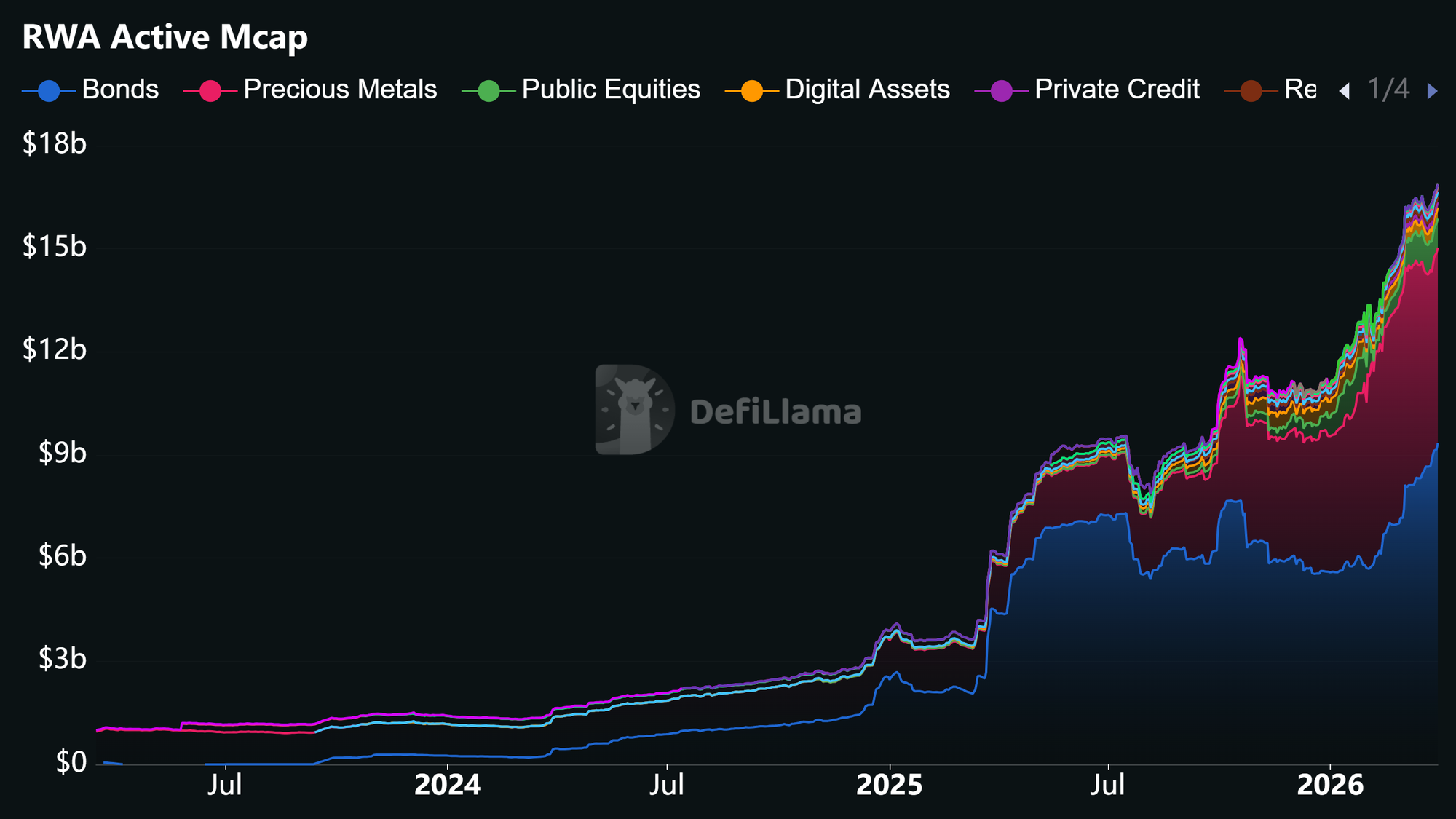

However, what Waller didn’t address in his speech – and what remains in question – is whether digital assets could cause this fabric to tear and what would happen to financial stability if so. As tokenised assets continue to swell and become more intertwined with the incumbent financial ecosystem, this question is becoming more pertinent, particularly with regard to tokenised investment funds. In simple terms, these are shares of traditional mutual funds, such as money market funds (MMFs) or government bond funds, represented on a blockchain as tokens. Having started as a niche fintech experiment, tokenised funds have grown to over $10 billion in assets under management (AUM) in less than two years.

RWA Active MCap 2026-03-31

Among them is BlackRock’s BUIDL behemoth, with an on-chain market cap of nearly $3 billion, and the $900 million Franklin OnChain US Government Money Fund (BENJI), blockchains. Last July, Goldman Sachs and BNY Mellon also launched a tokenized money market funds solution. And more developments have been rolling in this year: intraday trading its tokenised money market fund, and so on. No one can call this niche anymore. And that’s precisely why now is the time to talk about the risks.

Why tokenise at all?

The tokenization of funds brings real benefits. Their shares can be used as collateral for margin calls, transferred peer-to-peer outside of normal trading hours, and even used as a settlement asset, all the while still earning interest in the background. In the digital asset space, people like to call this “rehypothecation”.

And this is a potentially huge advantage for institutional investors and treasury managers. Lucas Outumuro, VP of Institutional DeFi at Sentora, explains that while “in traditional markets, capital is effectively ‘parked’ between settlement windows, on-chain, that same capital can be continuously reallocated, rehypothecated or used as collateral in real time”. He says this therefore “opens the door to strategies that optimise for capital efficiency rather than just asset allocation”. For now, tokenised funds are an admittedly tiny part of the wider mutual funds market, with US funds alone holding $23.5 trillion in AUM as of Q4 2025. But if they continue to grow as quickly as they have been, the potential for disruption really is as big as Governor Waller says.

The concentration problem

There is, however, a catch. Though institutional interest in these products is clearly building, this remains an intimate gathering rather than a house party. And in finance, intimate gatherings are not always a good thing. The tokenized equities landscape, for example, is currently dominated by two protocols – Ondo and xStocks – that control 76.4% of total market value, according to a report by Sentora. Investment in the actual funds is also equally concentrated. According to the Bank for International Settlements (BIS), around 90% of the total holdings in both BlackRock’s BUIDL and WisdomTree's WTGXX funds are in the hands of just four wallet addresses.

Outumuro says this concentration is a feature of early adoption, but concedes that it introduces both counterparty and liquidity risks that investors are not accustomedtransparency, instant settlement, 24/7 trading – create a risk profile that has to underwriting in public markets. He says: “The risk is not concentration itself, but how that concentration interacts with liquidity. If a small number of holders can materially move markets or withdraw collateral quickly, it creates fragility that traditional fund structures are specifically designed to avoid”. In simple terms, what Outomuro is saying is that it’s a catch-22. Participation remains low because the risks are poorly understood, which in turn exacerbates the risks.

When is a bank run not a bank run?

This is far from the only potential risk, though. Across the board, the features that make tokenised funds attractive – transparency, instant settlement, 24/7 trading – create a risk profile that hasin which meaning is produced not by linking words to real objects, but by the differences and relationships among yet to be tested in real-life scenarios. Take transparency, for example. In traditional funds, investors may not even learn about redemptions until the fund reports at the end of a month or quarter. On the blockchain, withdrawals can be seen immediately by anyone.

The Federal Reserve Bank of New York, in a September 2025 research paper on the financial stability implications of tokenized funds, flagged this as a key concern, saying that blockchain transparency “acts as a coordination device among investors”. The paper’s authors warn that “round-the-clock trading and settlement may speed up a run on an investment fund, if disruptions in the market for tokens outside normal market hours escalate”. Once redemptions start, panic may soon follow – and suddenly an orderly queue for the exit becomes a stampede. And with no closing bell, there’s no natural pause for investors’ emotions to take a breather.

Stress testing a run

A run scenario can create several potential problems. Firstly, it’s questionable whether all redemption requests could even be met. That’s because while tokens settle instantly, the underlying assets don’t. US Treasuries, for example, still clear on T+1, as does the majority of the financial system. This is a risk the BIS highlights in its November 2025 Bulletin. If everyone rushes for the exit, the question is whether tokenised funds could face the same constraints as open-ended property funds in the UK after Brexit, or private credit funds this year.

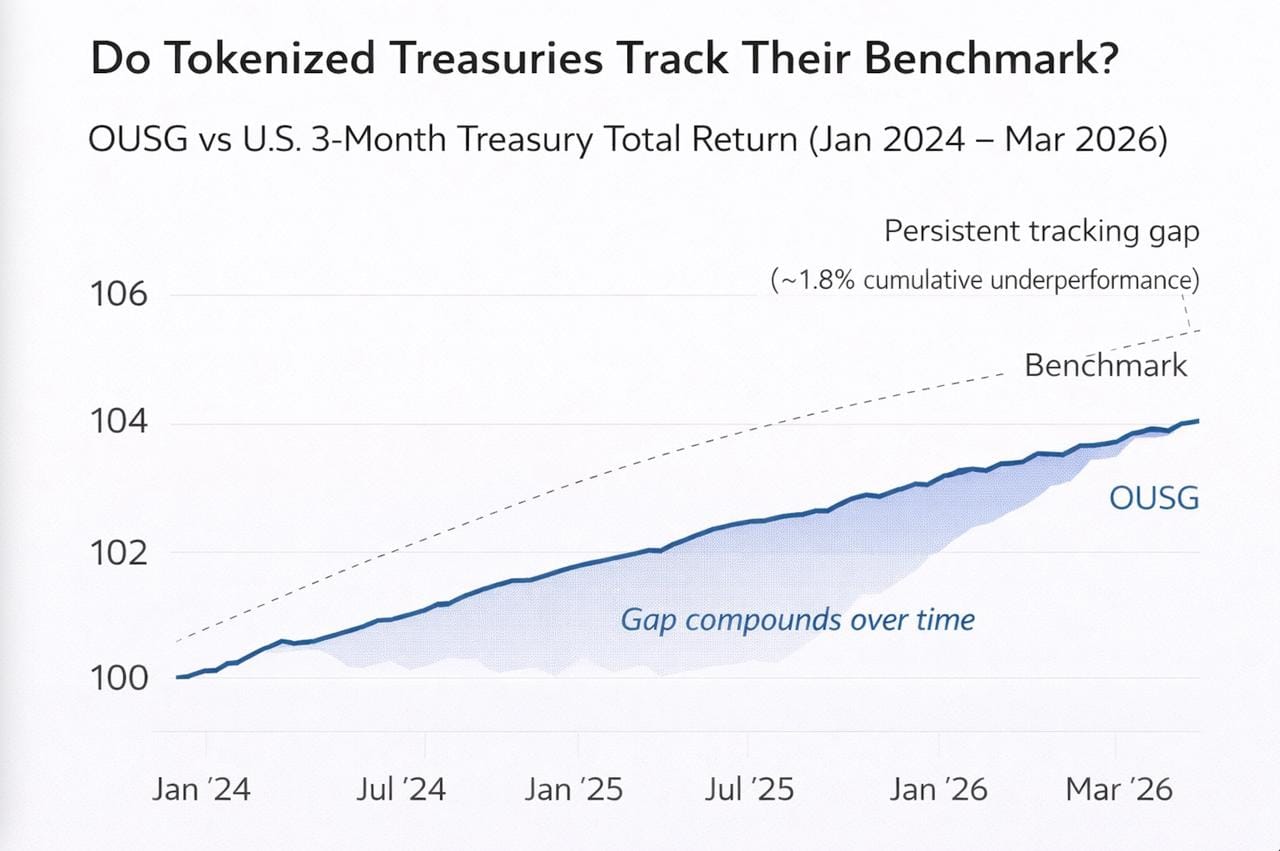

Secondly, under stress, the gap between tokenised funds and the underlying assets they track could widen, even if this divergence is relatively negligible right now. Jason Rowlett, founder of RWA data platform Foretoken, points out a consistent gap between tokenised treasuries and the underlying benchmarks they track, for example.

Foretoken - Tokenized Treasury Fund vs Benchmark

“For institutional investors, that distinction matters,” he says. “Tokenised assets should be evaluated based on how faithfully they track their benchmarks, not just their standalone returns”, adding that this represents “a clear example of basis risk in practice”.

And finally, the interconnectedness of the tokenised ecosystem could exacerbate a run, according to the New York Fed’s paper: “In times of stress, tokenized shares might amplify the systemic impact of a run on an investment fund if tokens are used to meet margin calls while also being used as a reserve asset for other financial products.” In other words, if the same token is simultaneously used as someone’s margin collateral and someone else’s reserve asset, the impact could be stacked.

The great regulatory divide

But while researchers are sounding the alarm, regulatory oversight of the space has loosened rather than tightened. The US Financial Stability Oversight Council – the body created after the 2008 financial crisis to identify systemic risks before they become crises – removed crypto and digital assets from its list of financial vulnerabilities in its December 2025 annual report. They were reclassified as “significant market developments to monitor”. The SEC and CFTC, meanwhile, have made a complete U-turn on their previously restrictive policies. CFTC Acting Chair Caroline Pham publicly said last September that “the public has spoken: tokenized markets are here, and they are the future”, while SEC Chair Paul Atkins echoed the sentiment when he described the new regulatory agenda as “a golden age of financial innovation on US soil”. There are certainly reasons for this optimism, which are widely acknowledged. However, the BIS and the IMF don’t appear to share it.

IMF Monetary and Capital Markets chief Tobias Adrian said in October that it’s “paramount to make sure regulations keep up with the growing role of non-bank and digital assets, especially as new risks emerge in areas like stablecoins and foreign exchange markets”. Similarly, London Business School Professor Hélène Rey, wrote in the IMF’s Finance & Development journal in September: “Major financial stability risks, including increased volatility in exchange rates, threats to public finances in many economies, and competition across currency networks are likely”.

The NY Fed paper, meanwhile, notes a detail almost in passing that should give every traditional investor pause: the largest tokenised fund in the market, BlackRock's BUIDL, operates as a private fund. That means it’s exempt from the disclosure requirements and liquidity risk management rules that apply to registered money market funds. And so, as the paper notes, regulators and the public have “little visibility into their operations”.

What to watch

These funds were born into an era of plentiful liquidity, near-zero rates, and a broadly risk-on environment. None of the major products have been tested by a real stress event to date. We simply don’t know how a major sell-off might impact funds that are simultaneously used as collateral, settlement instruments and reserve assets for stablecoins. We don’t know how wide the liquidity gap could become at scale. And we don’t know if the transparency of on-chain redemptions would indeed cause widespread panic, or actually aid price discovery.

What we do know is that the tokenised assets sector roughly tripled in size in 2025 alone, regulatory constraints are loosening, and the only institutions currently asking the hard questions about systemic risk are those with no jurisdiction to take action. That is not necessarily a reason to avoid tokenised funds. However, it is a very good reason to understand exactly what you're holding, who else is holding it, and how quickly you could get out if things went wrong.

The Last Bitcoin

by John Jameson

Bitcoin’s true power is not in its mathematical design, but in the collective strength of its myth. The 21 million hard stop of supply is a brilliant piece of postmodern fiction, a decimal point shift that successfully rebranded a quadrillion-unit protocol into one of the world's most sought-after scarce assets.

The American Empire is a network of intangibles, of systems built on trust. Japan's democracy, the global rules of trade, the reserve currency, the petrodollar, all of it engineered into existence by the United States. But to build a world built on trust you need signs and symbols.

A mechanism has been used to construct the world you live in. It went into overdrive during the 50s and 60s when the Mad Men of Madison Avenue used it to transmute ideas, layering meaning on top of meaning to sell more and more products and services. But, over time, it’s built a world which no longer seems real. A world divorced from reality. To explain it, I need to draw on four twentieth-century philosophers.

First, there was Ferdinand de Saussure. He saw language as a system of signs in which meaning is produced not by linking words to real objects, but by the differences and relationships amongAnd on this second level, the first level sign becomes the new input signifier, and a new signified (a cultural concept) is societally generated from it, forming a new second level sign. signs within the system. A sign is made of two parts. The signifier, the physical form (a word, an image, a sound) and the signified, the mental concept or idea. Together, they form an atomic unit of meaning.

Then, in the 1950s, Roland Barthes took it further. He called it Semiotics. Barthes, like Saussure, said that the signifier and the signified become a sign, but Barthes used the complete sign as the input for a second level of meaning. And on this second level, the first level sign becomes the new input signifier, and a new signified (a cultural concept) is societally generated from it, forming a new second level sign, which Barthes called the signified attached to level two, a myth.

Umberto Eco later argued that semiotic meaning need not stop at the second level. It can continue iteratively through a process called semiosis. The complete second-level sign is being used as input for the third. And on and on, each level moving further away from reality. In the 1970s, Jean Baudrillard coined the term "hyperreality" to describe this phenomenon. Baudrillard said hyperreality is created when signs no longer point to a stable reality. The signifier free floats, divorced from its original signified meaning. In a hyperreal world, a signifier only references other signifiers, in a closed system of signs creating a simulation that feels more real than the underlying reality. People respond to the simulation as if it were real. In a state of hyperreality, the chain of meaning has been pushed so far that there is nothing from the real world left to refer to. The simulation has become the reality. Baudrillard called it the Simulacra.

And Bitcoin is a part of it.

Everyone knows Bitcoin is scarce. 21 million coins. Hard-coded. Built in. No more, ever. It is the founding myth of Bitcoin as an asset class. It’s the reason it gets called digital gold. That’s why it’s classified as a hedge against inflation. The scarcity is treated as a brute fact of nature, as solid and immutable as the finite supply of gold buried inside the earth. But perception is derived from cultural myth and the placement of a decimal point. Let’s iterate Bitcoin through five levels of meaning.

|

L1 |

Signifier |

Bitcoin.

(Its name) |

|

L1 |

Signified |

The concept

of decentralised digital currency. |

|

L1 |

Sign |

Bitcoin is a

decentralised digital currency. |

(The Level 1 Sign is the input for the Level 2 Signifier)

|

L2 |

Signifier |

Bitcoin is a

decentralised digital currency. |

|

L2 |

Signified |

(myth)

Bitcoin is a store of value. |

|

L2 |

Sign |

Bitcoin is a

decentralised store of value. |

(The Level 2 Sign is the input for the Level 3 Signifier)

|

L3 |

Signifier |

Bitcoin is a

decentralised store of value. |

|

L3 |

Signified |

(myth)

Bitcoin is digital gold. |

|

L3 |

Sign |

Bitcoin is a

digital form of gold |

(The Level 3 Sign is the input for the Level 4 Signifier)

|

L4 |

Signifier |

Bitcoin is a

digital form of gold. |

|

L4 |

Signified |

(myth)

Bitcoin is scarce. |

|

L4 |

Sign |

Bitcoin is

digital gold and scarce. |

(The Level 4 Sign is the input for the Level 5 Signifier)

|

L5 |

Signifier |

Bitcoin is

digital gold and scarce. |

|

L5 |

Signified |

(myth) Bitcoin is valuable. |

|

L5 |

Sign |

Bitcoin is digital gold and valuable. |

Four iterations from reality, Bitcoin is scarce and valuable. To get there took four myths. It’s a store of value. It’s digital gold. It’s scarce, and it’s valuable. But scarce and valuable are no longer related to reality. At level 2, Bitcoin’s first myth is that it’s a store of value. As implied in the Genesis block, ‘The Times 03/Jan/2009 Chancellor on brink of second bailout for banks,’ Bitcoin’s reason for existence is to protect capital from central bank manipulation. So, at level 2, the myth of Bitcoin as a store of value is still grounded in reality.

At level 3, Bitcoin’s second myth is that it’s a form of digital gold. This myth is not generated from the real world, but from outside of it. It’s a myth created by inference. And that makes it what Jean Baudrillard called hyperreal. At level 4, Bitcoin’s third myth is that it’s inherently scarce. But this is inferred because Bitcoin is often thought of as digital gold, rather than what it is in reality. And at level 5, because of the scarcity, Bitcoin’s fourth myth is that it’s valuable. But at level 5, Bitcoin’s value is no longer related to reality. It’s now hyperreal, deriving narrative from other signifiers based on social myth. The myth of Bitcoin's scarcity does not need to be true. Baudrillard said the simulacrum sustains itself entirely through other signs. A store of value, digital gold, scarce, and valuable in a closed self-referential loop. No anchor to reality is required.

But Bitcoin's simulacrum went one step further. It manufactured the appearance of a real-world anchor. The 21 million hard-coded bitcoin supply feels materially real. It feels like a fact about the design choice made by a pseudonymous programmer. It feels as solid and immutable as gold. 21 million. Bitcoin’s maximum supply. That is the number everyone knows. Hard-coded. Can’t be changed. Unless it is hard forked. But then it’s Bitcoin no more.

Let’s compare Bitcoin’s supply of 21 million to the real world. Apple currently has 14.7 billion shares outstanding. Bitcoin's total supply is 0.142 per cent of Apple’s outstanding shares, but when compared to Nvidia’s 24.3 billion shares, Bitcoin’s max supply is just 0.086 per cent. Against those numbers, 21 million sounds almost absurdly small. The kind of scarcity that should command a premium just by virtue of existing, but that feeling is Baudrillard’s simulacrum working its magic. On you. One bitcoin is one hundred million satoshis. That is not a rounding convention or a display preference. The Satoshi is the base unit of the Bitcoin protocol. Every transaction, at every scale, in every wallet, on every exchange, is always and only a movement of satoshis. When you hold 0.0067 BTC you hold 670,000 satoshis.

A bitcoin is a collection of 100 million satoshis. There is only Satoshi. (This is not a contradiction. The level 1 signifier is the name ‘Bitcoin’ but a bitcoin is a collection of 100 million satoshis in the same way a pound is a collection of 100 pennies.)

Lean-In: The hyperreal illusion of scarcity depends on the decision about where you put the decimal point.

21 million multiplied by 100 million equals a supply of 2,100,000,000,000,000. That’s 2.1 quadrillion, or said another way, 2.1 million billion units of account. If the Satoshi had been chosen rather than Bitcoin, the founding myth would read very differently. 2.1 quadrillion units of money does not sound scarce. That does not sound like digital gold. That sounds like a near-unlimited supply.

The scarcity myth is not a property of Bitcoin. It is a property of the narrative frame produced by the decision to shift the decimal point eight places to the left and call the resulting number the real unit. 100,000,000 satoshis does not feel scarce. 1 bitcoin does. Bitcoin’s 21 million max supply is a simulacrum of scarcity. It mimics the feel of a finite material, but it is produced by placing a decimal point...And yes, I’m fully aware that this is the technical ceiling and in reality, due to lost private keys, the number of bitcoins is closer to 17 million. Compared to Apple's 14.7 billion shares or Nvidia's 24.3 billion, 21 million feels vanishingly rare. But that comparison is itself part of the simulation. It compares the unit of 1 bitcoin to the actual units of stock. But shift the decimal place and it tells a completely different story. People respond to the ‘Bitcoin is scarce’ narrative as if it were a fact about the world in the way that ‘gold is finite’ is a fact about the world. They buy Bitcoin on the basis of it, hold it on the basis of it, and build entire investment theses on the basis of it. This is what Baudrillard meant when he argued that the simulation becomes more real than the reality it replaced.

But the technical reality, the 2.1 quadrillion satoshis, the actual units in which all real transactions occur, does not feel scarce. In fact, it is the exact opposite. And this matters because, as The System of the World built by the American Empire is deconstructed, as you’re snapped out of the hyperrealistic trance that’s been built around you, all that is left is the real. In that real world, Bitcoin resolves into what it actually is. A system running at over 1 zettahash, a thousand, billion, billion hashes per second. According to the Cambridge Bitcoin Electricity Consumption Index, Bitcoin now consumes more than 200 terawatt-hours of electricity annually, that’s roughly three quarters of the entire United Kingdom's electricity demand.

And as trust breaks down inside The System of the World, as the hyperreal narrative falls away, all that is left is what is real. Wasted energy and lost opportunity cost. To me, this is a background condition. Not for higher prices but for economic abandonment.

The last bitcoin will never be mined.

John Jameson is a global macro speculator, writer, (and art addict.) He uses storytelling to dissect the System of the World. Get more insight from John at PrettyBangBang. Popular culture, capital, power, and the social controls you aren't supposed to notice.

Events on our radar

Digital Assets Forum Abu Dhabi launches on 13 May 2026, bringing together banks, asset managers, regulators, and digital asset leaders to discuss tokenisation, market infrastructure, and institutional adoption across the Middle East and global capital markets - tickets HERE

Bitcoin 2026 – Las Vegas, 27-29 April - premier Bitcoin ecosystem event – tickets HERE

DigiAssets Connect Zurich, 16-17 June - Custody, banking, and institutional infrastructure – tickets HERE