By Damien Black

Tokenization is not here to augment the way we do business – it represents a fundamental reordering of the investment world. And the new industry could command digital assets worth as much as $10 trillion by the end of the decade. That’s the verdict from one of the advocates of distributed ledger technology.

Nick Mersh is a portfolio manager at Canadian brokerage Purpose Investments who looks after funds that include tech stocks such as Tesla, Microsoft and Amazon. He also believes that blockchain-assembled investment vehicles are a thing of the near future – and by 2030, this online, or rather on-chain, industry will be worth trillions.

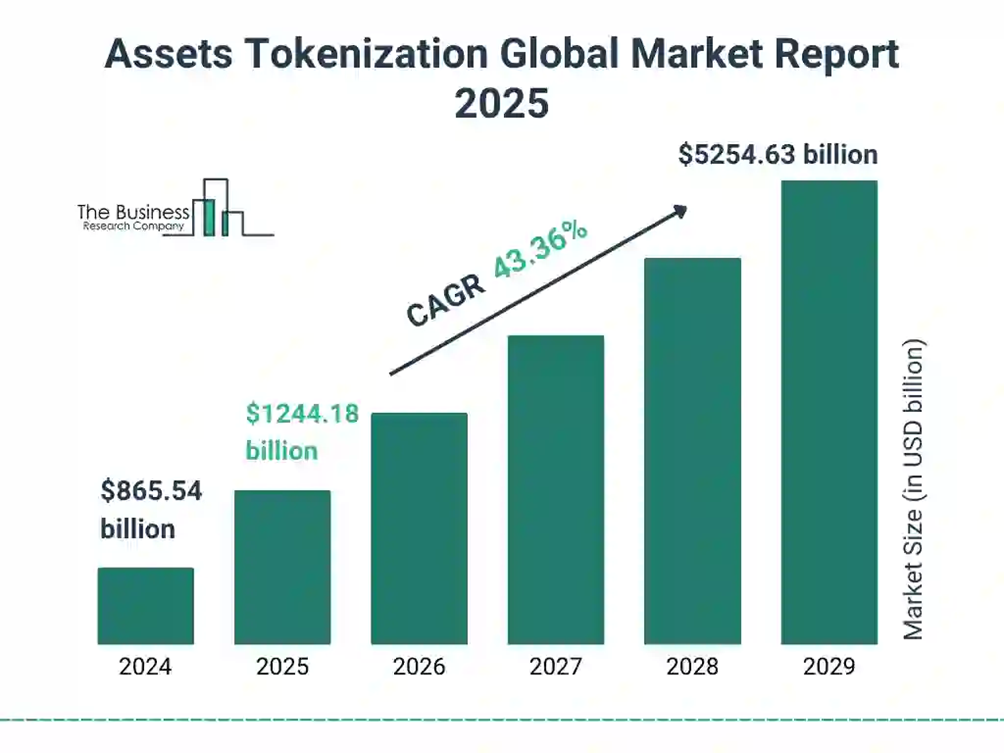

Growing strong: predictions looking rosy for tokenized assets

“We have to restart from a perspective of thinking about doing this on-chain first,” he says. “Tokenization is not really this incremental feature layered on top of capital markets but a structural reset of the market’s core rails, around issuance, custody, trading, settlement, collateralization and compliance.”

Key technological breakthroughs – for instance, cash-like instruments that use stablecoins – will signpost the way towards a brave new world where natively assembled on-chain asset classes become the norm.

“This will provide the transaction and settlement layers upon which further technology can be built,” he says. “Over the next five-year period the biggest shift is not just more crypto assets, but new institutional products getting designed on-chain first, and then secondarily wrapped into that legacy distribution.”

Too good to dismiss

Simply put, the traditional system of ledger settlements is too clunky to not be superseded by a fully evolved tokenized system.

“The reason that this is structural and not incremental is because if you think about traditional capital markets, the system still relies on multiple ledgers,” Mersh explains. “Brokers, custodians, and clearing houses still need a lot of reconciliation workflow [which leads to] delayed settlement in terms of the individual transactions, and what tokenization really introduces is a different architecture.”

Think a shared ledger with programmable transfer rules with the potential for cash and assets to be settled together as one package rather than separately. “This matters because it changes the economics of time, capital and operational friction, and there's a lot of advantages that drive the structural framing,” says Mersh.

Essential core components

Mersh envisages three essential components or stages to building the new ecosystem of on-chain investing. The first of these consists of public blockchains like Ethereum “which offer the deepest liquidity, strongest security, and very rich developer ecosystems”. Institutional investors are already using these with permissioning, identity layers, and regulated custody.

“But the next bucket is a permissioned or consortium network built specifically for regulated participants,” he says, a process he warns will entail exchanging “some decentralization for control, privacy, and compliance”. He adds: “That matters when you're dealing with these large equity markets.”

The last component is what Mersh refers to as “hybrid or interoperable models” which is what he believes the ecosystem “is ultimately going towards”. These models would allow assets to be issued on one chain, but then settled on another “and bridged across systems depending on the use case”. At that point, blockchain becomes the new normal of investing.

“What really matters here is standardization, interoperability, legal certainty – and maybe not maximal decentralization,” says Mersh, suggesting a compromise will have to be reached between freedom and privacy on the one hand and regulation and security on the other.

“Because when institutions say ‘on-chain’ they don't mean just ‘one chain’ – they mean these programmable settlement rails that meet a lot of these regulatory standards.”

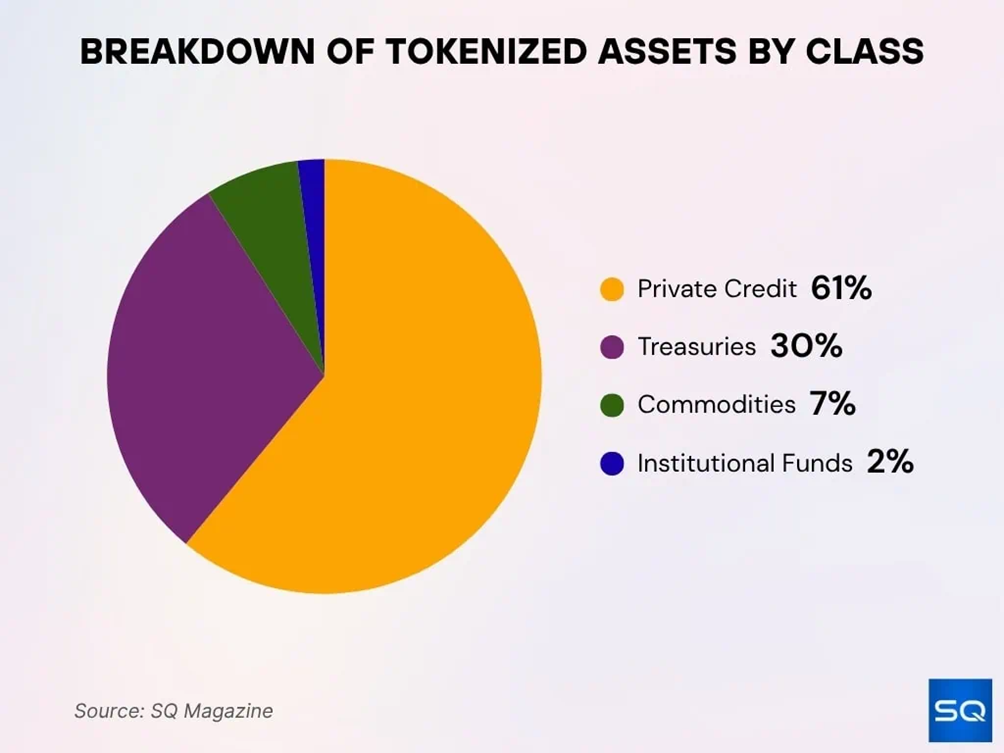

Tokenized assets at a glance

What’s the bottom line?

That’s a lot to digest, so I push him on a prediction. Late last year Mersh went on the record as saying tokenized assets could be a “multi-trillion dollar” market by 2030. But that seems a tad vague to me. How much does he mean really?

“I think putting it into the five-to-ten trillion range in the next couple years is a reasonable estimate,” he says without blinking. The first wave of this monetization will be stablecoins and tokenized cash-like products. “That market the entire system is built upon is huge. So you talk about that figure, you're looking at short duration in government bonds or money market funds, which are well into the tens of trillions of dollars.” Mersh thinks the second wave will be tokenized funds that share asset classes and ETF units.

“So you’re talking about an even larger investment market when it comes to trillions of dollars overall in that ecosystem. And then you'll get native tokenized equities. And if you think about the market cap of some of these companies right now – Nvidia is over $5 trillion, Google yesterday touched over four. If you get tokenized assets accessing that you can see just how much dollar-figure amounts will accelerate.”

Speed and efficiency

What are the other core benefits Mersh sees in tokenization? Faster transaction settlements, turning days into “near instant, which reduces counterparty risk and really frees up capital and balance sheet capacity”. This will really appeal to institutional investors, he adds. “The real prize here is not novelty, it’s balance-sheet efficiency, a lower operational risk, and the ability to mobilize liquidity with a lot less friction.”

“Once assets are sharing a digital and interoperable format, they can plug into these new workflows, so real-time collateral, automated rebalancing, on-chain repurchase, and eventually more continuous portfolio execution,” says Mersh. “And this is really where tokenization does begin to look less like this financial product innovation and more like this new operating system for the plumbing around markets themselves.”

democratised

Capital markets that have up until now been restricted to institutional investors like BlackRock or J.P. Morgan could be opened up to smaller retail investors, because tokenized assets can be reduced to the tiniest of fractions. A classic example of this is Bitcoin, where $1,000 can buy you BTC0.000011. “Absolutely, I think that adoption by institutions is the starting point in mass adoption,” says Mersh, a process he describes as “the democratization of individual asset classes”.

He adds: “Tokenization has this appeal intuitively if you think about fractional ownership, broader distribution, and then also potential secondary transferability. Because if you look at some of these asset classes, what you have from a lot of these funds is they're extremely illiquid and have trouble getting those secondary markets going.”

Tokenization: gateway to hidden markets?

Mersh believes tokenization could open up previously inaccessible markets to investors in countries that have hitherto been locked out of global capital markets. “It’s very hard if you’re somewhere in Venezuela or Turkey or Argentina to buy, say, an Apple stock directly, right? So, what this does is it really opens up not only those pockets of the market but it democratizes a lot of these different asset classes available on brokerage accounts in the U.S.”

If the prospect of assets being available beyond the traditionally ring-fenced preserve of what Mersh calls “guarded institutions” sounds far-fetched, there is already a precedent – of sorts. Mersh points to the U.S. equities market, where the largest share is collectively held by individual households. That’s true up to a point – American households hold 40% of equities, though the top tenth of those hold the lion’s share. Retail investors won’t be the only beneficiaries of course. Even bigger players sometimes struggle to get their hands on assets in less accessible regions of the world. Tokenization could see those hard-to-reach stocks opened up to the wider world too.

“If I’m looking at investing in certain companies in China or I want to get involved in a semiconductor company in Taiwan, I have the best trading and operational capabilities in-house here – but I still can’t access some of these markets [because] of the hurdles that are proven there,” says Mersh. “Tokenization unlocks that in a big way.”