SEC opens the door to tokenised equities

Tokenisation has moved into the heart of U.S. equity markets. The SEC’s approval of Nasdaq’s framework for tokenised securities marks one of the clearest regulatory endorsements of blockchain-based market infrastructure to date. Under the proposal, eligible equities can trade in tokenised form alongside traditional shares, with settlement handled via a DTC-linked blockchain pilot. Crucially, the structure keeps everything familiar, same tickers, same prices, same investor rights, while upgrading the underlying rails.

Why it matters: This is no longer about crypto-native experimentation. U.S. regulators are signalling that tokenisation can operate within the existing market structure - not outside it - accelerating its path into mainstream capital markets.

News in Brief

NASDAQ, Kraken and Boerse Stuttgart get together. A wave of alliances between traditional exchanges and crypto platforms is accelerating. Intercontinental Exchange has invested in OKX with plans to launch tokenised stocks and derivatives, while Nasdaq has partnered with Kraken and Germany’s Boerse Stuttgart (via Seturion) to expand tokenised trading infrastructure globally. Why it matters: Tokenisation is no longer being built in isolation - it is being integrated directly into existing exchange ecosystems and distribution networks.

Crypto-native firms gain access to financial plumbing. Kraken Financial has secured access to the U.S. Federal Reserve payment system, marking a significant step for crypto-native institutions operating within traditional financial infrastructure. At the same time, tokenised commodity markets (including oil) have demonstrated the ability to trade through weekend volatility while traditional markets remain closed. Why it matters: The gap between crypto rails and traditional finance is narrowing, with blockchain markets increasingly complementing, rather than competing with, existing systems.

Regulatory momentum builds behind tokenised securities. The SEC’s Investor Advisory Committee has recommended reforms to enable broader tokenisation of equity securities, citing clear potential benefits for investors. This builds on the Nasdaq approval and adds further regulatory backing for tokenised market structures in the U.S. Why it matters: Policymakers are moving from observation to active support, reducing uncertainty for institutions building tokenised products.

Europe tightens standards under MiCA Across the EU, MiCA implementation is beginning to reshape the market, with stricter compliance and operational requirements driving consolidation among crypto platforms. New guidance from ESMA and the expiry of transitional arrangements are accelerating this shift. Why it matters: Regulatory clarity is improving globally — but it is also raising the bar, favouring well-capitalised and compliant players.

Deep Dive — Nasdaq + Kraken test tokenised equity distribution

The Top Line. Nasdaq’s partnership with Kraken turns its tokenised securities framework into a real-world distribution test — not just a regulatory milestone.

The Details

Nasdaq’s newly approved framework solves one side of the equation: how to issue tokenised equities within existing market rules. Kraken addresses the other - how to distribute them. Through its xStocks platform - which has already processed around $25bn in volume - Kraken provides a global, crypto-native access point to tokenised shares. This opens equity markets to users outside traditional brokerage channels, without changing the underlying asset. Importantly, the structure keeps everything familiar. Tokenised shares carry the same pricing, voting rights and dividend entitlements as conventional stock, with settlement routed through DTC-linked infrastructure. What changes is access — not the asset.

Why it matters for markets

Distribution is the unlock: Tokenised equities have existed for years but lacked scalable access. Kraken provides that missing layer.

Exchanges are extending their reach: Nasdaq isn’t competing with crypto platforms — it’s using them to expand distribution.

Liquidity becomes the next test: If trading splits across traditional and crypto venues, maintaining price alignment will be critical.

A hybrid model is emerging: Traditional rails handle issuance and compliance, while crypto platforms expand access and trading hours.

The bottom line. This is less about tokenisation and more about who controls access to equity markets. If successful, the Nasdaq–Kraken model could redefine how stocks are distributed globally, without overhauling the system itself.

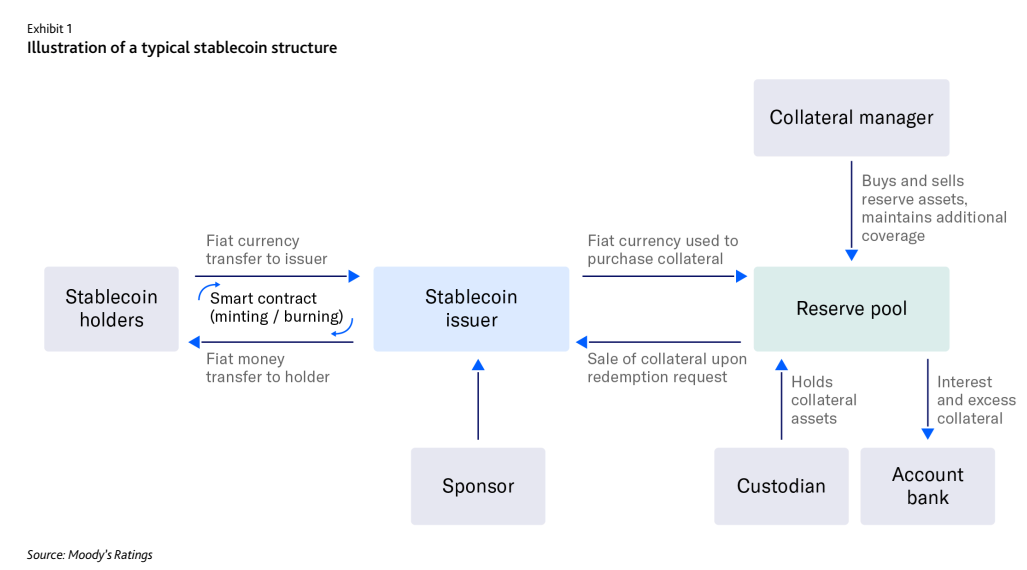

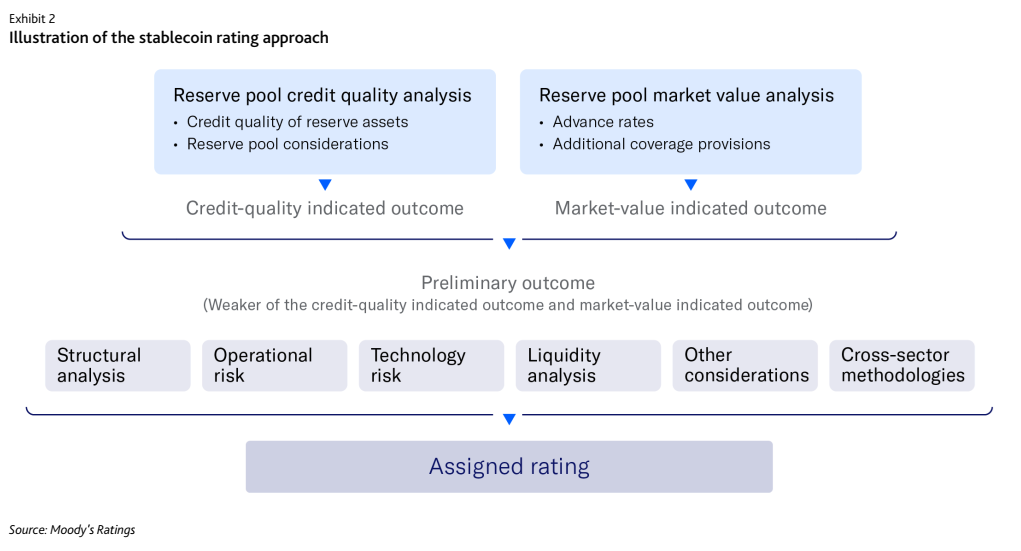

Moody's Ratings has published the first cross‑sector rating methodology for stablecoins, providing a transparent and independent framework to assess their credit risk. Stablecoins increasingly function like on‑demand deposits, but unlike cash, they carry credit risk. Until now, the market has lacked a consistent, fundamentals‑based way to assess that risk.

How it works: The Moody's methodology focuses on credit fundamentals, not price or sentiment:

- Reserve asset risk: Credit quality of the assets backing the stablecoin, including weighted‑average quality and the weakest link.

- Market value risk: Haircuts (advance rates) applied to reserve assets to test whether they can withstand stress and still cover redemptions.

- Liquidity risk: Ability to meet rapid, on‑demand redemptions without forced sales.

- Operational & technology risk: Execution failures, counterparty disruptions, and reliance on blockchain and smart contracts.

- Cash flow: Whether operating costs or interest payments could erode buffers between reserves and obligations.

The methodology applies these factors through a structured credit approach: bottom‑up analysis of reserve pools combining credit quality and market‑value stress tests; a preliminary outcome based on the lower of credit‑quality and market‑value results, expressed as an alphanumeric score; and notching adjustments for additional risks—including liquidity, operational, technology, and structural considerations to arrive at a final deposit rating.

The bigger picture: Stablecoins are already a core building block of digital finance and global payments. Market capitalisation reached roughly $300 billion last year and could grow to $2–$3 trillion by the end of the decade. As their role in payments and settlement expands, understanding credit risk becomes critical.