1. JPMorgan expands tokenised fund infrastructure

JPMorgan has expanded the rollout of its Kinexys Fund Flow platform (formerly part of the Onyx blockchain division). The system tokenises investor records and automates capital calls and distributions for private equity funds. It is now being integrated across the bank’s wealth management and brokerage divisions. Why it matters: Tokenisation is increasingly being used to modernise back-office infrastructure — particularly in private markets where administration, reporting and settlement processes remain slow and fragmented.

2. China maintains crypto ban but opens narrow RWA pathway

China’s central bank has reaffirmed its ban on domestic cryptocurrency activity while allowing tightly controlled offshore tokenisation structures linked to Chinese assets. The framework allows companies to raise capital internationally without opening domestic financial markets to crypto trading. Why it matters: The policy reflects China’s dual strategy — strict domestic controls paired with cautious experimentation in cross-border tokenised financing.

3. Mortgage-backed assets move on-chain

Better Home & Finance has secured a $45m investment from Framework Ventures to develop a mortgage-backed RWA token strategy. The initiative aims to package residential mortgage exposure into tokenised instruments that can trade on blockchain infrastructure while remaining inside regulated financial structures. Why it matters: Mortgage markets represent one of the largest pools of real-world financial assets. Tokenisation could eventually improve transparency and liquidity in mortgage risk trading.

4. Commodities and sustainability assets drive “RWA 2.0”

Issuance of tokenised gold, commodity-backed instruments, carbon credits and energy-linked assets is accelerating as the next phase of the RWA market develops. These assets appeal to institutional investors because blockchain rails offer traceability and auditability — key features for ESG reporting and regulatory oversight. Why it matters: Sustainability-linked assets and commodities could broaden the investor base for tokenised markets beyond crypto-native participants.

Deep Dive

Compliance-first tokenisation becomes the default

The Top Line: Real-world asset tokenisation is shifting toward a compliance-first architecture, with KYC/AML checks, jurisdictional restrictions and transfer rules embedded directly into the token itself.

The Details

As institutional adoption grows, tokenisation platforms are increasingly embedding compliance controls at the token level rather than relying on off-chain checks by brokers or administrators. These controls include identity-verified wallets, jurisdictional whitelists and programmable transfer restrictions that automatically block non-compliant transactions.

Regulators are also becoming clearer about how these instruments should be classified. Increasingly, RWA tokens are treated as digitised financial products, with clearer distinctions emerging between utility tokens, payment tokens and asset-backed tokens. This regulatory clarity makes it easier to structure tokenised instruments within existing securities frameworks. In practice, that means private-placement exemptions, permissioned distribution and regulated secondary trading for assets such as tokenised bonds, private credit and real estate.

The broader implication is that “compliance as code” is becoming a prerequisite for liquidity. If investor eligibility and transfer restrictions are built directly into the asset, trading venues can support secondary markets with fewer operational risks. Many industry observers describe this transition as the emergence of “RWA 2.0” — a phase where tokenisation moves beyond experimentation toward scalable issuance, institutional infrastructure and regulatory alignment. What they say:“KYC-gated wallets, jurisdictional restrictions and AML integration are becoming standard, ensuring compliance without sacrificing efficiency.”

Further reading

- https://www.ainvest.com/news/institutional-adoption-rwa-tokenization-2026-strategic-inflection-point-blockchain-backed-finance-2512/

- https://www.mexc.com/en-GB/news/82779https://www.mexc.com/en-GB/news/827797

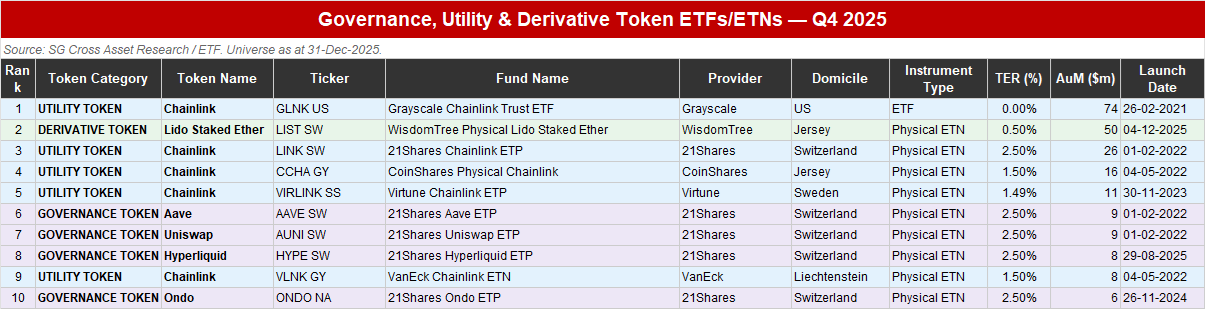

Société Générale deep dive into on-exchange token ETPs

ETF specialists at the French investment bank recently released their comprehensive survey of on-exchange-traded products within the broader crypto space. Quite the most interesting part of this comprehensive survey was the look at on-exchange listed ETPs tracking tokens, in all shapes and guises. Despite the hype surrounding the rise of these funds, all 35 of them, assets under management (AuM) remain small. Total disclosed AuM across all three categories is roughly $233m, with a heavy concentration in Chainlink utility token products. TERs are consistently high — averaging ~1.8–2.1% across governance and utility tokens — reflecting the niche and newer-vintage nature of these products.

🟣 Governance Tokens (21 products) — dominated by 21Shares and Valour; Aave and Uniswap ETPs are the largest at ~$9m each; many DeFi-native tokens (Ondo, Pyth, Hyperliquid) with very small AuM

🔵 Utility Tokens (12 products) — Chainlink is the standout, led by Grayscale ($74m) and 21Shares ($26m); most others sub-$2m

🟢 Derivative Tokens (2 products) — WisdomTree's Lido Staked Ether ($50m) vs Valour Tether Gold (~$0m)

Token Directory (ranked by AuM, colour-coded by category):