Welcome to the eighth letter from TheIntersection team. We hope you are enjoying this weekly letter. Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: NASDAQ and Kraken

- Data: Moody's new stablecoin ratings approach

- Analysis: Are tokenised assets a big opportunity for market makers?

- Opinion: Tokenised ETFs enhance opportunity but demand equally agile risk oversight

- Our weekly events round-up

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

SEC opens the door to tokenised equities

Tokenisation has moved into the heart of U.S. equity markets. The SEC’s approval of Nasdaq’s framework for tokenised securities marks one of the clearest regulatory endorsements of blockchain-based market infrastructure to date. Under the proposal, eligible equities can trade in tokenised form alongside traditional shares, with settlement handled via a DTC-linked blockchain pilot. Crucially, the structure keeps everything familiar, same tickers, same prices, same investor rights, while upgrading the underlying rails.

Why it matters: This is no longer about crypto-native experimentation. U.S. regulators are signalling that tokenisation can operate within the existing market structure - not outside it - accelerating its path into mainstream capital markets.

News in Brief

NASDAQ, Kraken and Boerse Stuttgart get together. A wave of alliances between traditional exchanges and crypto platforms is accelerating. Intercontinental Exchange has invested in OKX with plans to launch tokenised stocks and derivatives, while Nasdaq has partnered with Kraken and Germany’s Boerse Stuttgart (via Seturion) to expand tokenised trading infrastructure globally. Why it matters: Tokenisation is no longer being built in isolation - it is being integrated directly into existing exchange ecosystems and distribution networks.

Crypto-native firms gain access to financial plumbing. Kraken Financial has secured access to the U.S. Federal Reserve payment system, marking a significant step for crypto-native institutions operating within traditional financial infrastructure. At the same time, tokenised commodity markets (including oil) have demonstrated the ability to trade through weekend volatility while traditional markets remain closed. Why it matters: The gap between crypto rails and traditional finance is narrowing, with blockchain markets increasingly complementing, rather than competing with, existing systems.

Regulatory momentum builds behind tokenised securities. The SEC’s Investor Advisory Committee has recommended reforms to enable broader tokenisation of equity securities, citing clear potential benefits for investors. This builds on the Nasdaq approval and adds further regulatory backing for tokenised market structures in the U.S. Why it matters: Policymakers are moving from observation to active support, reducing uncertainty for institutions building tokenised products.

Europe tightens standards under MiCA Across the EU, MiCA implementation is beginning to reshape the market, with stricter compliance and operational requirements driving consolidation among crypto platforms. New guidance from ESMA and the expiry of transitional arrangements are accelerating this shift. Why it matters: Regulatory clarity is improving globally — but it is also raising the bar, favouring well-capitalised and compliant players.

Deep Dive — Nasdaq + Kraken test tokenised equity distribution

The Top Line. Nasdaq’s partnership with Kraken turns its tokenised securities framework into a real-world distribution test — not just a regulatory milestone.

The Details

Nasdaq’s newly approved framework solves one side of the equation: how to issue tokenised equities within existing market rules. Kraken addresses the other - how to distribute them. Through its xStocks platform - which has already processed around $25bn in volume - Kraken provides a global, crypto-native access point to tokenised shares. This opens equity markets to users outside traditional brokerage channels, without changing the underlying asset. Importantly, the structure keeps everything familiar. Tokenised shares carry the same pricing, voting rights and dividend entitlements as conventional stock, with settlement routed through DTC-linked infrastructure. What changes is access — not the asset.

Why it matters for markets

Distribution is the unlock: Tokenised equities have existed for years but lacked scalable access. Kraken provides that missing layer.

Exchanges are extending their reach: Nasdaq isn’t competing with crypto platforms — it’s using them to expand distribution.

Liquidity becomes the next test: If trading splits across traditional and crypto venues, maintaining price alignment will be critical.

A hybrid model is emerging: Traditional rails handle issuance and compliance, while crypto platforms expand access and trading hours.

The bottom line. This is less about tokenisation and more about who controls access to equity markets. If successful, the Nasdaq–Kraken model could redefine how stocks are distributed globally, without overhauling the system itself.

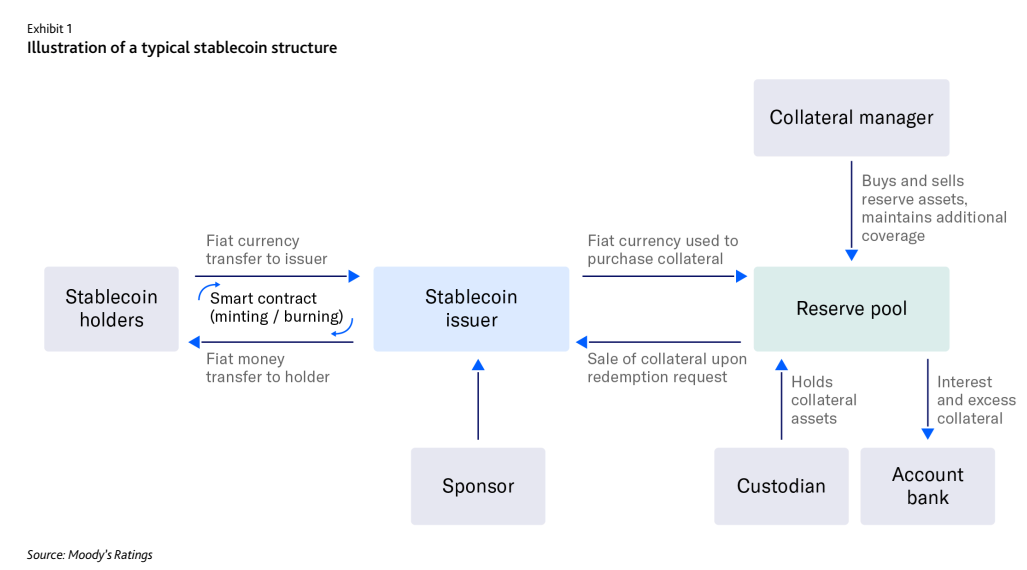

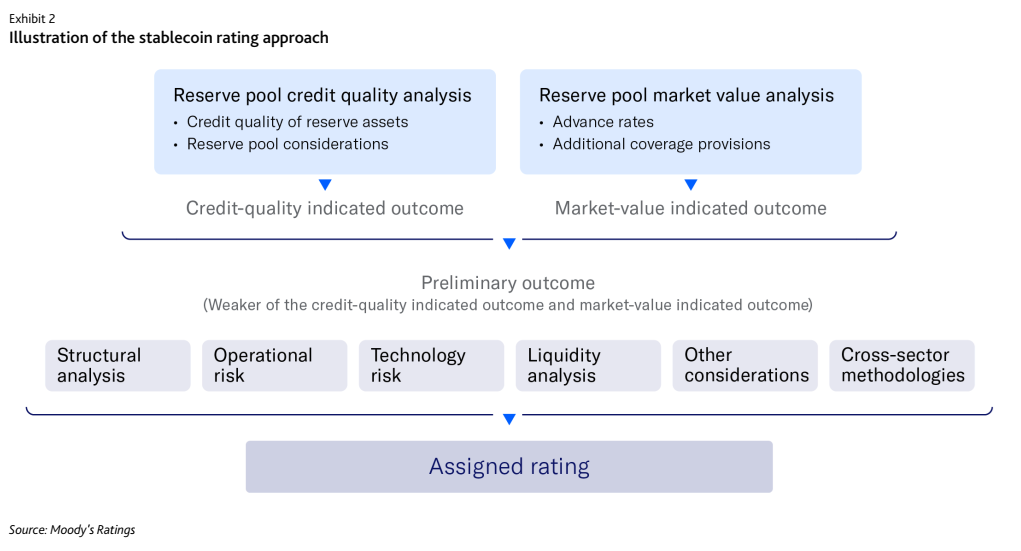

Moody's Ratings has published the first cross‑sector rating methodology for stablecoins, providing a transparent and independent framework to assess their credit risk. Stablecoins increasingly function like on‑demand deposits, but unlike cash, they carry credit risk. Until now, the market has lacked a consistent, fundamentals‑based way to assess that risk.

How it works: The Moody's methodology focuses on credit fundamentals, not price or sentiment:

- Reserve asset risk: Credit quality of the assets backing the stablecoin, including weighted‑average quality and the weakest link.

- Market value risk: Haircuts (advance rates) applied to reserve assets to test whether they can withstand stress and still cover redemptions.

- Liquidity risk: Ability to meet rapid, on‑demand redemptions without forced sales.

- Operational & technology risk: Execution failures, counterparty disruptions, and reliance on blockchain and smart contracts.

- Cash flow: Whether operating costs or interest payments could erode buffers between reserves and obligations.

The methodology applies these factors through a structured credit approach: bottom‑up analysis of reserve pools combining credit quality and market‑value stress tests; a preliminary outcome based on the lower of credit‑quality and market‑value results, expressed as an alphanumeric score; and notching adjustments for additional risks—including liquidity, operational, technology, and structural considerations to arrive at a final deposit rating.

The bigger picture: Stablecoins are already a core building block of digital finance and global payments. Market capitalisation reached roughly $300 billion last year and could grow to $2–$3 trillion by the end of the decade. As their role in payments and settlement expands, understanding credit risk becomes critical.

The Bottom line: This first‑of‑its‑kind framework gives investors and policymakers a capitalisation lens for comparing stablecoins, helping to strengthen market confidence, collateral mobility, and liquidity in a rapidly evolving digital payments ecosystem.

Are tokenised assets a big opportunity for market makers?

There is money to be made, but only if genuine on-chain demand materialises and significant operational hurdles can be cleared

By Toby Lawes

If 24/7 liquidity and the instant settlement of everything is an unstoppable train, market-making firms will be essential for greasing the wheels. But whether tokenised real-world assets (RWA) and ETFs represent an attractive spot to put their precious trading capital to work is a question being asked across liquidity provider C-suites. For some, like Amsterdam-based Flow Traders, tokenisation represents a new frontier. Volatility and inefficiencies will present plentiful arbitrage opportunities for skilled players. For others, concerns remain that genuine appetite for on-chain exposure and out-of-hours trading will materialise.

“We live and die on volumes and volatility,” explained Jake Ostrovskis, head of OTC trading at Wintermute, a historically crypto-native market-making firm that has backed some early token projects. “For now they remain niche products, but we do we see a world where tokenised equities and by extension ETFs become more and more interesting. It is something we are watching very, very closely,” he said.

Secondary market trading for tokenised assets and funds is still in its infancy. Aside from a small handful of ETFs that have been tokenised, most blockchain-based funds operate similarly to mutual funds: once-a-day liquidity and once-a-day pricing. Leading tokenised equities issued by xStocks and Dinari’s dShares, for example, enjoy some secondary market volumes, but the leading way is on-chain precious metals, where trading volumes amount to a few billion per day.

As for the underlying assets themselves, the trading of tokenised products is intermediated by market making firms. These liquidity providers charge bid-ask spreads for each trade they facilitate – quotes are often given in stablecoins – but can also profit from arbitrage opportunities and even short-term directional bets.

Amsterdam-based Flow Traders, which started life in 2004 as an ETF market maker, has been one of the most vocal proponents of the tokenisation opportunity, with CEO Thomas Spitz describing it as the ‘next ETP moment’ on the firm’s Q4 results call. Flow Traders is supporting early liquidity for Dinari’s token project and recently announced a 24/7 over-the-counter (OTC) offering for tokenised money market funds, equities, and commodities – a bet on genuine institutional demand to trade and hedge exposure both overnight and on the weekend.

“As a market maker, you want to see as much flow as possible. And we do see tokenised assets taking off,” said Flow Traders co-head of trading in a recent interview with The InterSection. “I look at tokenised products as a new asset class. You get the same exposure but with some attractive add-ons like 24/7 trading, programmability, interoperability and the ability to fractionalise. They are getting bigger and bigger,” he said.

The early days of cryptocurrency trading – also a 24/7 market – were famously fertile ground for market makers. Significant mispricings between exchanges and low levels of competition created arbitrage opportunities aplenty and wide latitude for steep bid-ask spreads. For Roger Bayston, head of digital assets at Franklin Templeton and architect of the firm’s blockchain-based investment platform Benji, tokenisation represents a “massive opportunity” for market makers.

“There’s a lot of volatility in these markets and that’s how these firms make money. If there’s big uptake and enough fungibility across the space, then it’s potentially lucrative business.” Bayston said Franklin Templeton was engaging with several liquidity providers to establish secondary-market functionality for its tokenised money market funds (MMFs) – something Flow Traders has since said it will provide as part of its new OTC offering.

Another asset manager eyeing 24/7 liquidity for its tokenised MMFs is WisdomTree. The New York-based firm recently announced round-the-clock trading and instant settlement for the WisdomTree Treasury Money Market Digital Fund (WTGXX) – the first example of such a capability within the US regulatory perimeter. To facilitate that liquidity, a WisdomTree subsidiary will offer bilateral trading by holding a large inventory on hand, but the firm hopes to attract additional liquidity providers over time.

This model is one that WisdomTree is plotting to extend beyond money funds. “We want to see other exposures become available and tradable on chain and are actively exploring tokenised ETFs,” said Will Peck, head of digital assets at Franklin Templeton. “We view that as the next evolution.” On the appeal of tokenised asset trading for market makers, Peck felt there would be arbitrage opportunities for market makers but stressed that there must be genuine demand from customers to trade them.

Whether that demand will materialise is tokenisation’s trillion-dollar question, but it is not there yet. In fact, issuers of tokenised assets are incentivising market makers to show prices at appealing spreads for their products – not dissimilar to the contractual market maker model that is widely used within ETFs. xStocks, for example, the largest issuer of 1:1-backed tokenised equities and ETFs, uses retainer models and negative-swap rebates to entice market makers to provide volume.

The firms providing liquidity in tokenised assets to-date largely fall into one of two camps: crypto native market makers like Wintermute and GSR or proprietary trading firms like Jane Street, Flow Traders and Cumberland, the latter a subsidiary of DRW. Conspicuously missing are the large investment banks, but several, including Goldman Sachs, are starting to build out tokenisation desks, a person familiar with the plans told The InterSection. The prop trading firms believe they are best placed to win in this new world. “If markets go towards 24/7, we already have sophisticated pricing models for closed markets from trading ETFs, so we can roll them out on the crypto rails we are already comfortable with given our crypto trading,” said Flow Traders’ Jansen.

He added that while “the crypto native firms are comfortable on crypto rails, they are a bit behind on the even more complex more traditional finance rails” – an assertion disputed by one specialist crypto market making firm The InterSection spoke to. “Right now, it makes no sense to market make a bond on crypto rails because you need to pre-fund it. For a specific bond, you can count the number of trades each day on one hand – the economics just don’t make sense,” explained Flow Traders’ Jansen whose firm’s new OTC facility is designed to help clear this hurdle.

Another problem is that settlement in tokenised markets remains largely bilateral – at least outside of individual exchanges – increasing operational complexity for market makers and limiting the netting benefits enjoyed within centrally cleared systems. As a result, market makers often need to fund positions on a gross rather than net basis, increasing balance sheet usage and funding costs – a pain point that will be reflected in wider spreads.

And although progress is being made on this front, prime broking on crypto rails also remains limited. This impairs market makers' ability to take on leverage to provide quotes, meaning they are required to use more of their own balance sheet. Instruments tracking the same assets but with greater capital efficiency like perpetual futures – ‘perps’ – have seen a real surge of interest in recent months, perhaps a reflection of this difficulty. But where market makers will really be tested is on the weekends. With traditional markets shut, they will be unable to create and redeem tokens by trading the underlying, will be unable tap pre and post market venues as they can on weekdays, and will find it difficult or impossible to source proxies and hedges.

“There’s very little trading over the weekend because there is no real way to hedge and therefore traders are having to warehouse large amounts of risk,” said Wintermute’s Ostrovskis. “Spreads will have to be measurably wider to account for that.” But thin trading will lead to large dislocations – and that brings significant opportunities for market makers. “It is common for us that when a market is closed on a Monday we need to price not just over the weekend but from Friday evening until the next Tuesday. There are a lot of similarities from our ETF trading we can reuse,” said Flow Traders Jansen.

Toby Lawes is a writer over at www.etfstream.com. He came from a fund management role at Ruffer LLP where he worked on the multi-asset, global macro strategy. He holds an undergraduate degree in Economics from the University of Edinburgh and a postgraduate degree in Financial History from the University of Cambridge. Toby is a CFA charterholder.

Instant market access provided by tokenised ETFs enhances opportunity but demands equally agile risk oversight

By Anatoly Crachilov, CEO and Founding Partner at Nickel Digital Asset Management

The growing adoption of tokenised funds reflects a broader transformation within capital markets that has been building momentum in recent years. By retaining the familiar investment structure that investors know and trust while leveraging blockchain technology, tokenised funds introduce a range of new capabilities such as near-instant settlement, 24/7 trading and enhanced transparency for both institutional and individual investors. This advanced infrastructure aligns with the demands of today’s faster and more interconnected financial system, and appeals to investors seeking more cost-effective ways to diversify portfolios and manage their risk more dynamically.

In recent years, leading global institutions have begun launching or exploring tokenised products, reflecting growing confidence in the innovative model and its potential to reshape the market. Our recent survey found that 97% of institutional investors believe that major asset managers launching tokenised ETFs will help drive wider adoption of the technology, a view we share. BlackRock, for example, which manages over $2 trillion in traditional ETFs, recognised the opportunity that tokenisation presents and launched its first tokenised fund, BUIDL, in 2024. After launching in March 2024 with around $180m in assets, by March 2025 BUIDL had surpassed $1bn assets under management and continued to grow to $2.5bn by late 2025, highlighting the strong demand for blockchain-enabled investment structures.

The broader market for tokenised real-world assets has also expanded rapidly, growing from around $10 billion in 2024 to more than $25 billion earlier this year. As more institutions continue to launch and support tokenised products, they will play an important role in bridging the gap between traditional investment strategies and the digital asset ecosystem.

A number of innovative models are emerging, demonstrating how technology is reshaping the investment landscape and accelerating the transition of tokenisation from a conceptual idea to mainstream adoption. One of the most transformative developments is fractional ownership. While the concept of shared ownership already exists within traditional ETF structures, tokenised ETFs allow assets to be divided into much smaller digital units on blockchain networks, enabling more granular portfolio construction through enhanced precision and flexibility compared to traditional ETFs. The fractional ownership also opens the door for investors to gain exposure to assets that were previously hard-to-access, providing more diversification within their portfolios, and the potential for greater returns from assets that, without tokenised ETFs, investors could struggle to access. By lowering barriers to entry, smaller family offices and even retail investors can access strategies that were previously mainly within the remit of large allocators. Fractional ownership and reduced entry barriers will help create a more efficient investment environment by fostering a more diverse and liquid investor base. This is expected to become a key component of the market evolving towards greater accessibility.

Another key innovation is the integration of decentralised trading platforms with tokenised assets. Unlike traditional ETFs, which are constrained by fixed trading hours and rely heavily on intermediaries to facilitate transactions, tokenised ETFs can trade continuously. This 24/7 market access would fundamentally change how investors interact with their portfolios, allowing them to respond to market developments in real time.

Presently, the 9:30 am to 4 pm trading hours over 5 working days, or 32.5 hours of available trading time, capture less than 20% of the available calendar hours. The potential 5x increase in trading hours offered by the new technology, enables investors to adjust their positions more dynamically, rather than wait for markets to open before responding.

However, this continuous trading environment also introduces new operational and risk challenges. Nickel Digital’s CEO, Anatoly Crachilov, notes: “The instant market access provided by tokenised ETFs enhances opportunity but demands equally agile risk oversight mechanisms to dynamically adjust portfolio exposure.”

Regulatory developments over the past six months have also catalysed the expansion of tokenised ETFs. Several European jurisdictions have launched pilot programmes involving established banking institutions to explore how tokenised securities can operate within existing regulatory frameworks. While the results of these initiatives are still emerging, regulators' willingness to engage with the technology demonstrates a growing recognition that digital assets are not a passing trend but are becoming an integral part of the evolving financial infrastructure.

As JPMorgan Chase CEO Jamie Dimon commented earlier this year: “Digital assets and tokenisation are an inevitable part of the future financial ecosystem. It’s no longer a question of if banks and investors will adopt these technologies, but how quickly they can do so to meet client expectations and unlock new efficiencies.” If tokenised ETFs continue to grow at their current pace, they will significantly accelerate the broader acceptance of blockchain technology and potentially pave the way for wider adoption of digital assets more generally.

Institutional participation, such as the critical DTCC pivot project with Nasdaq, which allows equity trades to be settled in either blockchain or traditional ledger at clients' discretion, plays a crucial role in building trust in emerging financial technologies, helping to overcome lingering scepticism and demonstrating the practical benefits of these innovations. In this sense, the increasing embrace of tokenised ETFs by major financial institutions may prove to be a key catalyst in bringing digital assets closer to mainstream adoption.

London's award-winning Nickel Digital Asset Management is a regulated investment manager at the forefront of merging traditional finance with the fast-paced digital asset market. We have designed a diverse portfolio of funds specifically for institutional clients, capitalising on the volatility of digital asset markets. By adapting arbitrage and technical analysis techniques from traditional financial markets, we generate non-directional or venture-style returns while maintaining a monthly liquidity profile.

Events on our radar

Digital Assets Forum Abu Dhabi launches on 13 May 2026, bringing together banks, asset managers, regulators, and digital asset leaders to discuss tokenisation, market infrastructure, and institutional adoption across the Middle East and global capital markets - tickets HERE

Bitcoin 2026 – Las Vegas, 27-29 April - premier Bitcoin ecosystem event – tickets HERE

DigiAssets Connect Zurich, 16-17 June - Custody, banking, and institutional infrastructure – tickets HERE