Welcome to the ninth letter from TheIntersection team - and happy Easter!

We hope you are enjoying this weekly letter.

Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: Congress & tokens and BlackRock and the regs, plus privacy on public blockchains

- Data: Tokenised RWA assets hit $26 bn

- Analysis: Lloyds and Archax in UK blockchain breakthrough

- Our weekly events round-up

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

Congress signals tokenisation is inevitable

Washington is no longer debating whether tokenised securities should exist — only how to regulate them. A landmark hearing by the U.S. House Financial Services Committee on 25 March marked a clear shift in tone, with bipartisan agreement that tokenisation is now an inevitable part of capital markets. Lawmakers focused on practical barriers ( including legacy rules such as TEFRA) and how existing securities frameworks will need to adapt. The discussion is expected to feed directly into the upcoming CLARITY Act, scheduled for Senate markup in late April. Why it matters: U.S. policy is moving from caution to construction. Regulatory alignment ( not technology) is now the main gating factor for scaling tokenised markets.

News in Brief

TradFi embeds blockchain into core systems Major infrastructure providers are integrating tokenisation directly into existing financial workflows. Murex has partnered with Quant to enable programmable settlement for bonds and deposits, while BMO is building a tokenised cash platform on Google Cloud’s Universal Ledger to support 24/7 institutional transfers. Why it matters: Tokenisation is shifting from standalone pilots to embedded infrastructure within banking and trading systems.

Privacy and compliance move on-chain A key technical barrier — privacy on public blockchains — is beginning to be addressed. The T-REX Network has integrated fully homomorphic encryption (FHE), allowing regulated transactions to be processed without exposing sensitive data. Why it matters: Solving privacy could unlock broader institutional use of public blockchain networks, reducing reliance on fully permissioned systems.

Commodities and strategic assets gain traction Tokenisation is expanding beyond financial assets into “hard assets.” Recent initiatives include a $78m programme to tokenise U.S. strategic minerals such as antimony, gold and silver, alongside new models linking gold-backed tokens to DeFi liquidity and stablecoins. Why it matters: Commodities and real-world inputs ( particularly those tied to energy, defence and sustainability ) are emerging as the next frontier for tokenisation.

Deep Dive — BlackRock and regs: why tokenisation still isn’t scaling

The Top Line

BlackRock’s vision for tokenised markets is already technically viable — but outdated legal frameworks remain the biggest barrier to scaling.

The Details

BlackRock CEO Larry Fink has laid out one of the clearest institutional cases yet for tokenisation: a financial system where stocks, bonds and funds can be issued, traded and held as easily as digital payments. The firm isn’t speculating — it is already building parts of that system, with tokenised funds and growing exposure to digital assets. The problem is not infrastructure, according to FinTech Weekly. It’s the rulebook. A key obstacle is TEFRA, a 1982 U.S. tax law designed to eliminate bearer bonds. While effective at preventing tax evasion, it unintentionally blocks many forms of tokenised bond issuance on public blockchains - particularly where ownership is represented digitally rather than through traditional intermediaries. There are additional frictions. Custody rules written for physical certificates still shape how securities must be held and transferred, while tokenised assets often fall into unclear legal categories - neither fully traditional securities nor entirely new instruments. The result is institutional hesitation. Around two-thirds of investors cite regulatory uncertainty as the main reason they have not deployed into digital assets - ahead of both market and technology risk.

Tokenised RWA assets hit $26 bn

Five Trends Shaping the Market in Q1 2026

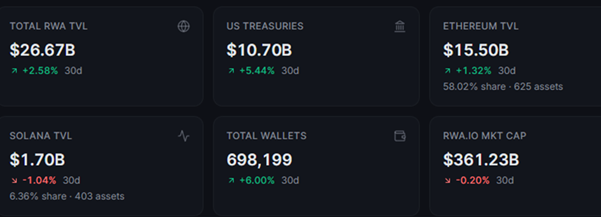

On-chain RWA value reached $26.67 billion in March 2026, up 75% over ten months, with wallet counts rising to 698,199 - a 6% jump in just 30 days.

Headline data points

Data sourced from RWA.xyz & RWA.io

1. US Treasuries Are the Anchor Asset Class

Tokenized US Treasuries now account for $10.7 billion in TVL - roughly 40% of all on-chain RWA value and up over 80% from mid-2025. This is the asset class that proves tokenization works at scale. Circle's USYC leads at $2.61B (up 40% in 30 days), followed by BlackRock's BUIDL at $2.14B and Ondo's USDY at $1.34B. Janus Henderson's Anemoy fund surged 84% in a single month to cross $1B, while Franklin Templeton's BENJI and WisdomTree's WTGXX each sit comfortably above $750M. The appeal is straightforward: 3.2–3.8% yields with on-chain settlement, instant redemption, with DeFi protocols. Institutions now treat these instruments as on-chain cash equivalents i.e a core liquidity tool.

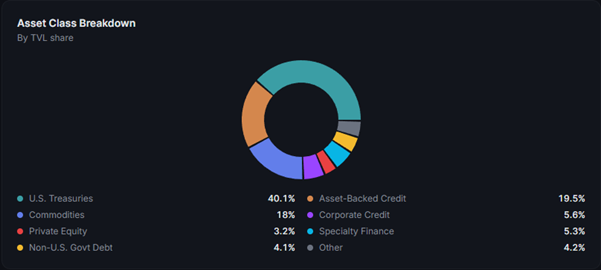

Asset Class Breakdown

Data sourced from RWA.xyz & RWA.io. By TVL share

· U.S. Treasuries 40.1%

· Asset-Backed Credit19.5%

· Commodities18%

· Corporate Credit5.6%

· Private Equity3.2%

· Specialty Finance5.3%

· Non-U.S. Govt Debt4.1%

· Other4.2%

Ethereum holds $15.5B in tokenized RWAs (58% of the market) across 625 distinct assets. That dominance is real, but it is slowly eroding. BNB Chain surged 31% in 30 days to $3.4B (12.6% share), while Plume Network posted a remarkable 67% monthly gain to $355M. Stellar, Arbitrum, and Avalanche each hold meaningful positions between $620M and $1.4B. The implication is that institutional issuers are distributing across chains rather than consolidating on one. Multi-chain issuance — seen in products like BUIDL and USYC deployed across Ethereum, Solana, Avalanche, and others — is becoming the norm, not the exception.

Chain TVL Breakdown: Top 10 networks · Source: RWA.xyz

|

Chain |

TVL |

Share |

30d |

Assets |

|

Ethereum |

$15.5B |

58.02% |

1.32% |

625 |

|

BNB Chain |

$3.4B |

12.59% |

31.02% |

366 |

|

Solana |

$1.7B |

6.36% |

1.04% |

403 |

|

Stellar |

$1.4B |

5.25% |

6.44% |

34 |

|

Liquid |

$1.3B |

4.9% |

20.75% |

6 |

Data sourced from RWA.xyz & RWA.io

3. Solana Is the retail and speed Play

Solana's RWA TVL stands at $1.7B, roughly 6.4% of the market, across 403 tokenized assets. That is modest relative to Ethereum by value, but Solana has consistently led in wallet onboarding — accounting for the majority of new RWA holders in several weekly periods this year. The chain's throughput and near-zero transaction costs make it the natural home for fractionalised, retail-accessible RWA products. .

4. The Credit and Commodity Layer Is Building Beneath Treasuries

Beyond Treasuries, the asset class breakdown reveals a diversifying market. Asset-backed credit instruments hold $5.2B (19.5%), led by Maple's Syrup USDC at $1.78B yielding 6.23%. Tokenized commodities — primarily gold via Tether's XAUT ($2.53B) and Paxos Gold ($2.27B) — account for 18% of TVL. Corporate credit, speciality finance, and non-US government debt each contribute meaningful slices. This layering matters. The RWA market is evolving from a single-product story (Treasuries) to a multi-asset on-chain fixed-income and commodity market. Private credit yields of 5–9% and commodity price exposure through physically backed tokens are attracting a different investor profile than that of Treasury buyers.

Top Tokenized Assets: Ranked by TVL · Source: RWA.xyz

|

# |

Asset |

Platform |

Class |

TVL |

7d |

30d |

APY |

|

1 |

Circle USYC |

Circle |

U.S. Treasuries |

$2.61B |

7.2% |

39.9% |

3.17% |

|

2 |

BlackRock BUIDL |

Securitize |

U.S. Treasuries |

$2.14B |

3.9% |

9.4% |

3.44% |

|

3 |

Tether Gold XAUT |

Tether |

Commodities |

$2.53B |

0.8% |

12.6% |

— |

|

4 |

Paxos Gold PAXG |

Paxos |

Commodities |

$2.27B |

1.4% |

9.3% |

— |

|

5 |

Ondo USDY |

Ondo |

U.S. Treasuries |

$1.34B |

10.4% |

4.0% |

3.55% |

|

6 |

Syrup USDC |

Maple |

Credit |

$1.78B |

0.5% |

5.6% |

6.23% |

|

7 |

Anemoy JTRSY |

Centrifuge |

U.S. Treasuries |

$1.04B |

7.8% |

83.7% |

3.53% |

|

8 |

Franklin BENJI |

Franklin Templeton |

U.S. Treasuries |

$1.02B |

2.4% |

0.1% |

3.50% |

|

9 |

WisdomTree WTGXX |

WisdomTree |

U.S. Treasuries |

$752M |

0.1% |

3.1% |

3.49% |

|

10 |

Superstate USTB |

Superstate |

U.S. Treasuries |

$739M |

7.0% |

5.4% |

3.48% |

|

11 |

Ondo OUSG |

Ondo |

U.S. Treasuries |

$682M |

2.2% |

9.7% |

3.36% |

|

12 |

Spiko EUTBL |

Spiko |

Non-U.S. Govt Debt |

$916M |

2.5% |

19.1% |

1.66% |

Data sourced from RWA.xyz & RWA.io

5. Wallet Growth Signals Broadening Adoption — Not Just Deeper Pockets

Total RWA wallets reached 698,199, growing at 6% month-on-month. This is not purely institutional accumulation. Retail-oriented products on Solana and BNB Chain, fractionalised real estate tokens, and stablecoin-denominated yield instruments are pulling new participants into on-chain RWAs for the first time. The wallet-to-TVL ratio remains heavily skewed — at roughly $38,000 in average value per wallet — implying institutional capital dominates. But the trend is toward broader distribution. If wallet growth continues at this pace, the market will cross 750,000 holders before mid-year, which would mark a meaningful threshold for network effects in secondary liquidity.

Lloyds and Archax in UK blockchain breakthrough

by Damien Black

Naysayers take note – if you’re still thinking tokenization is just a tech fad for crypto bros, a venerable banking giant begs to differ. Lloyds recently cut a deal with digital asset broker Archax that saw tokenized deposits issued on the blockchain for the first time in the UK.

Lloyds, which was established in 1765, said the move “illustrates how tokenisation can revolutionise traditional banking, turning real-world assets into digital forms that can be purchased, sold or transferred instantly”. Public blockchain ledgers permit universal access and are therefore said to guarantee transparency – the technology’s advocates say this spells an end to disputes over accounting discrepancies. Asset tokenization’s backers are hailing it as a future cornerstone of the global financial system. And that future, they say, has arrived.

How Lloyds got into the game

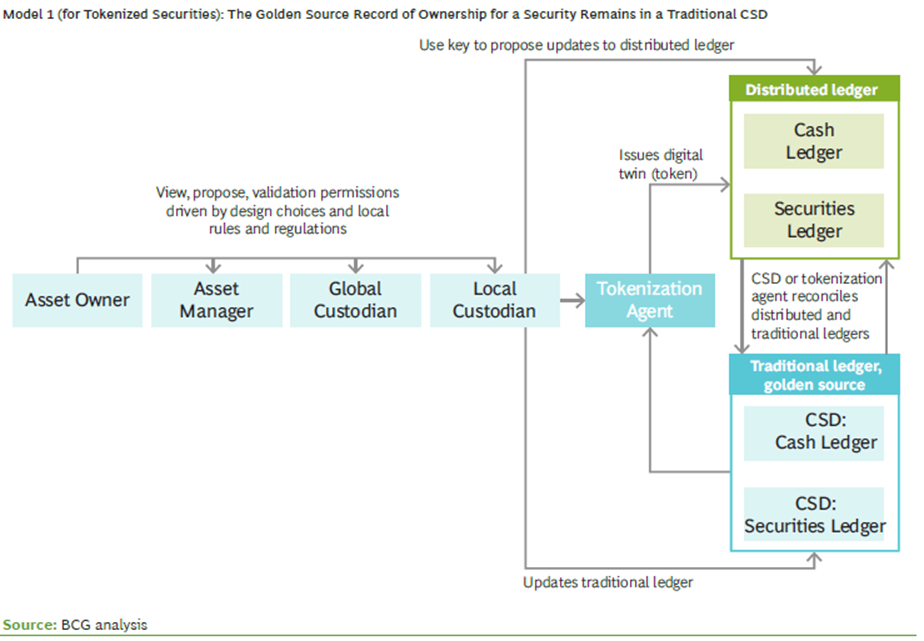

The British bank announced earlier this year (January 7) that it had issued tokenized deposits on the Canton network, a publicly accessible blockchain designed for regulated financial markets endorsed by Microsoft, Goldman Sachs and BNP Paribas. Lloyds then used the Canton deposits to purchase a “tokenized gilt” – essentially a digital government bond.

Traditional bonds, known as gilts in the UK, are typically registered in siloed databases guarded (a cynic might say jealously) by a conventional middleman such as the Debt Management Office. A tokenized gilt, on the other hand, is stored on blockchain technology that is immutable and therefore cannot be tampered with – ownership, in this case Lloyds’, represented by a digital token. Canton hosts an estimated $6 trillion in assets, though not all of them are yet fully tokenized. Other major players in this field include Kinexys, formerly known as Onyx – set up by JP Morgan in 2020, it has processed around $900 billion in tokenized US Treasuries at the time of writing.

A landmark transaction

Nor is tokenized trading a one-way street that results in assets proving difficult to shift once they are sitting comfortably in their shiny new blockchain home. “Archax then moved the underlying funds back into its regular Lloyds account, showing how easily transactions can flow between blockchain and traditional banking systems,” said Lloyds. The fluidity described by Lloyds – not to mention the UK bank’s credible reputation – might do something to appease critics.

Blockchain-based transactions using tokens also benefit from enhanced speed, settling in minutes as opposed to days. This is because token-based transactions do not depend upon manual processes reliant on good-old-fashioned homo sapiens. This need for multiple human intermediaries – who tend to have things like mortgages, lifestyles and families to fund and therefore require remuneration – naturally pushes up the cost of doing business. Whereas blockchain is facilitated by smart contracts, which can automate essential tasks such as interest payments, auditing and collateral management. Sounds too good to be true? Well, no pioneer undertaking is without its hazards – or to put it another way, there can be no reward without risk.

Tokenized securities vs. the traditional model

Some potential pitfalls

In a media-cited report published in November, the International Organisation of Securities Commissions (IOSCO) warned that “as the transition progresses and asset tokenization scales up, risks will continue to evolve”. A primary concern noted by IOSCO is cybersecurity. Ownership of real world assets (RWAs) on distributed ledger technology (DLT) is typically gate-kept by private keys – a digital code long used in cryptocurrency to verify ownership.

“Tokens stored on-chain can be transferred only through private keys,” explained IOSCO. “In turn, these private keys are stored in digital wallets. Tokenized asset custodians are responsible for the safeguarding of these private keys [and] investors’ holdings can be compromised through [...] fraud or theft where malicious actors exploit security vulnerabilities to gain control.” Likewise, blockchain investors should be wary as keys can be lost or destroyed due to human error, hardware failure or poor digital system back-up.

Too good to be true? Tokenization promises streamlined transactions:

IOSCO also points to a potential legal minefield, with uncertainty over whether ownership of a token signifying a RWA always aligns with ownership of the asset itself. To put it another way, the map is not the territory. “Most jurisdictions have historically mandated in their legal frameworks how ownerships and transfers of financial assets such as shares and debentures should be recorded or performed in order for it to be legally recognized,” said IOSCO, warning that DLT records of ownership and transfers “might not feature or fit cleanly within these framework requirements, as such technologies were not contemplated at the time the legislation was created.” It concluded: “Investors face legal risks if ownership or transfers made using tokens on the DLT are invalidated or not recognized as envisaged.”

Blockchain not as transparent as it seems

Doing business on the blockchain might not be as smooth as Lloyds et al would have you believe. IOSCO highlighted confusion that arises when DLT operators adopt varying models of ownership record-keeping, with some prioritising off-chain over on-chain and vice versa. “Some operators continue to maintain off-chain records as the official legal source of ownership records, which takes precedence over the on-chain records,” it said. “Some have combined features – off-chain book-entry centralized records on systems, with on-chain records as the official legal source of ownership.” While others use the on-chain records for official legal ownership but keep off-chain records as a back-up.

If reading that gave you a headache, don’t despair – it means you’re paying attention. IOSCO dryly notes that such varying approaches “might confuse investors” in tokenized assets “on what is the authoritative record of ownership [...] and potentially lead to disputes, if not properly disclosed”.

So much for an end to ledger disputes.

In a joint notice issued with IOSCO in October, the Financial Stability Board pointed to “challenges such as fragmented responsibilities and inconsistent definitions”. It added: “Enhanced international cooperation and coordination is essential to address regulatory arbitrage and ensure consistent and coherent oversight.” Unfortunately, if there’s one thing business can’t abide, it’s regulation. The stance taken by IOSCO and the FSB doesn’t sit well with the idea that tokenized transactions will make investing a smoother, faster process.

And more generally speaking, it’s wise to be wary of tech innovations that promise an easier, better life. Social media was once heralded as a phenomenon that would bring people together, fostering global “digital town squares” where folks could exchange ideas and stories to the benefit of all.

The rest, as they say, is history.

Events on our radar

Digital Assets Forum Abu Dhabi launches on 13 May 2026, bringing together banks, asset managers, regulators, and digital asset leaders to discuss tokenisation, market infrastructure, and institutional adoption across the Middle East and global capital markets - tickets HERE

Bitcoin 2026 – Las Vegas, 27-29 April - premier Bitcoin ecosystem event – tickets HERE

DigiAssets Connect Zurich, 16-17 June - Custody, banking, and institutional infrastructure – tickets HERE