by Anna Fedorova

The UK Treasury’s choice of HSBC to facilitate the tokenisation of gilts as part of its Digital Gilt Instrument (DIGIT) pilot is predictable and debatable in equal measure. A 160-year-old bank to lead a strategy whose aim it is to position the UK as a G7 leader in the use of blockchain technology? The choice itself is worth exploring as much as the wider strategy.

The Orion platform, which won the tender process, is HSBC’s proprietary, permissioned digital asset infrastructure specifically designed to issue and settle bonds within the traditional financial framework. It boasts extensive experience working with governments and institutional initiatives, notably a successful green bond issuance in Hong Kong.

The DIGIT project aims to issue short-dated sovereign bonds in tokenised form for the first time within the UK’s Digital Securities Sandbox (DSS). With this move, the Treasury is very much testing the waters – the new bonds will be managed outside of the government’s main debt management programme.

While the tokenised US treasuries market is already $10.84 billion, none of these bonds are issued natively on a blockchain by the US government.

Source: RWA.xyz | Tokenized U.S. Treasuries

Yet its goals are lofty: to be the first G7 country to ever tokenise its sovereign bonds. To be clear, we’ve seen several experiments with corporate bond tokenisation – including Germany’s Siemens, which issued a €60 million digital bond on a public blockchain in 2023.

But, to date, no other nation has issued a digital government bond, so it’s a big deal. Especially at a time when some other nations, notably the United States, are moving rapidly to incorporate digital assets into their financial policies. If successful, this could be a major power signal.

The rules of the game

And that’s exactly why the choice of provider is so critical. It’s not just about how competent or successful they are, but also about how it positions Britain in the global digital asset race.

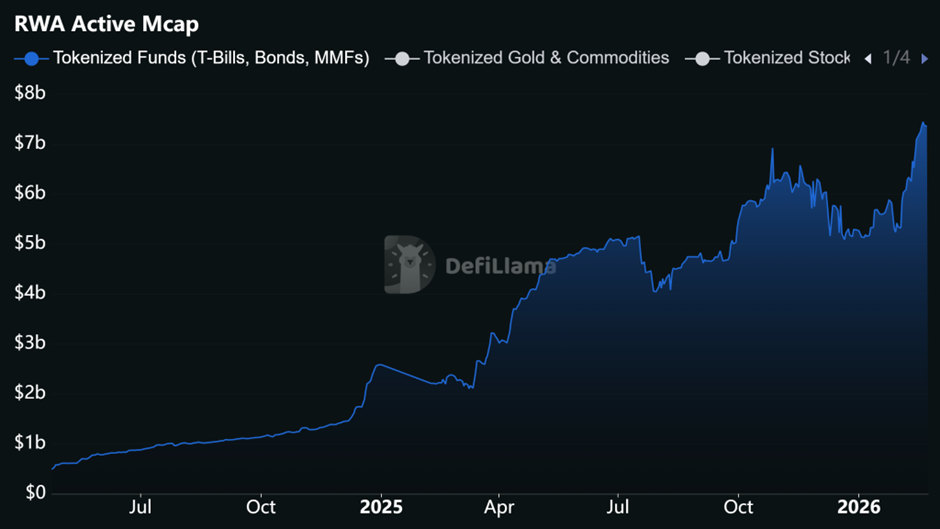

Tokenised funds with exposure to T-bills, bonds and MMFs have grown continuously, with active on-chain market cap now sitting at $7.35 billion

Source: Real World Assets - DefiLlama

HSBC Orion is a cautious choice. Conservative, even. An incumbent with proven acumen, not a novel experiment. Private, permissioned, and operated by one of the world's biggest banks, Orion is an invite-only club that’s fully integrated into the broader institutional settlement process.

Through this platform, HSBC has already facilitated some $3.5 billion worth of “digitally native” bond issuance for entities ranging from the European Investment Bank (EIB) to the Hong Kong government. This proven pedigree, and HSBC’s leading position in the UK’s existing financial infrastructure, remove much of the risk associated with the digital asset sector.

The message is loud and clear: the UK intends to adopt distributed ledger technology (DLT) by integrating it into the existing financial system rather than experimenting outside it.

That is a sober choice – especially at a time when global perception of digital assets is subdued due to the widespread sell-off across Bitcoin and other cryptocurrencies. During times of heightened market risk, optics matter. HSBC may not be a shiny new digital start-up, but perhaps the choice is boring by design.

The move is all the more meaningful in the post-Brexit context, amid concerns over the loss of competitiveness for UK businesses. In particular, financial services exports to the EU have shrunk markedly since Brexit, with the market share of UK financial services in major EU countries falling across the board.

On top of this, recent reporting by the Financial Times suggests that nearly 6,000 entrepreneurs, the majority from the technology sector, have left the UK for pastures new due to sweeping tax changes. Against this backdrop, digital assets become an even more important avenue to re-establish global leadership.

Permissioned versus permissionless

When it comes to government-led blockchain initiatives, there are broadly two distinct tracks forming. On the one hand, the UK seems to be following in Hong Kong’s footsteps by choosing a permissioned blockchain operated by a financial services incumbent. Using the tried-and-tested provider who successfully executed Hong Kong’s digital green bond issuance last year fits this mould.

On the other hand, there is the more experimental style adopted by nations like Singapore. As part of its Project Guardian, which was announced back in May 2022, Singapore and its partner banks – DBS Bank, JPMorgan and SBI Digital Asset Holdings – turned to permissionless blockchains Polygon and Aave.

As early as November 2022, Singapore was already experimenting with cross-currency transactions involving tokenised Japanese yen and Singapore dollar deposits on these open blockchains. At the time, Mr Sopnendu Mohanty, the Monetary Authority of Singapore (MAS) chief fintech officer, said that “digital assets and decentralised finance have the potential to transform capital markets”, but with “appropriate guardrails in place”.

Of course, a permissionless blockchain comes with its own set of concerns – including counterparty, security and data privacy risks. Singapore’s strategy to minimise these is quite clever. It controls access to the sandbox at the onboarding level, so only approved counterparties who have passed KYC and AML checks can participate. It works for now, though this approach is yet to be tested at scale.

Shaping innovation

In contrast, the UK’s digital gilt project seems less about experimenting and more about integrating blockchain technology in a controlled, permissioned environment from the outset. This cautious strategy could, paradoxically, enable the UK to integrate digital assets into its financial ecosystem more quickly by circumventing the regulatory roadblocks associated with experimental technology.

Not only that, but infrastructure developed by a 160-year-old bank will likely inspire far more confidence from an equally well-established financial institution than a bootstrapped crypto project that hasn’t even been around for a decade. It’s the best of both worlds: the speed and efficiency of digital technology alongside institutional-level compliance and trust.

However, there are downsides. With a banking giant like HSBC leading this project, there could be less room for the UK fintech sector to showcase the value it can add to the UK’s DLT initiatives. Less input from crypto-native firms also means potentially missing out on hard-won experience at the bleeding edge of blockchain innovation.

For example, the tightly controlled environment means that composability outside the Orion platform, or access to wider liquidity beyond institutional circles, will likely be limited. In decentralised finance (DeFi), a tokenised gilt could theoretically be used as collateral across the ecosystem, interact with other tokenised assets, or be reused in repo-like structures. In this model, though, the likelihood is it remains within the sandbox.

In addition, permissionless blockchains are often built on open-source code. As a result, innovations and integrations happen faster. HSBC’s Orion is built for pilots like these, but the key question is: how will this scale as digital issuance grows? What if a trillion pounds were to move on-chain?

Is T+0 wishful thinking?

Regardless of the blockchain choice, the main benefit of blockchain technology remains: T+0 settlement. In theory, this could mean instant international transactions. No more 24-hour-plus waits, no more need for interim credit exposure, lower counterparty risk. At least, that’s the theory.

In reality, though, the typical settlement for UK gilts today is T+1. And, indeed, according to last year’s implementation plan from The Accelerated Settlement Taskforce Technical Group, not even T+1 settlement is universal across the UK securities market at present. The document cautioned that “the move to T+0 or Atomic Settlement should not take place until after the move to T+1”.

In a similar vein, the US Securities Industry and Financial Markets Association (SIMFA) has previously warned of the risks of transitioning to T+0 settlement too soon. These include major changes across the operations of market participants such as prime brokers and clearing houses, reduced time for compliance testing, and disruption to global settlement and FX conversions.

The point is that for T+0 settlement to be truly beneficial, the entire financial ecosystem must upgrade. That means repo markets, which are closely linked to the UK sovereign bond market, as well as FX markets, central bank clearing houses and custodial chains.

Regardless of DIGIT’s success, if it remains on a separate settlement rail to the rest of the bond market, the benefits will remain theoretical. In fact, paradoxically, it could add more complexity and introduce more fragmentation into the system – at least for the time being. So the real test isn’t about settling intra-day trades. That’s just the proof of concept. The real test will be when the UK tries to integrate digital bonds into the existing financial market.

A part of the system

In practice, the success of the pilot will depend on several factors. Once the issuance details are announced, subscription levels and investor breakdown will tell us a lot about the real interest in this project. Solid trading volumes and tight bid-offer spreads with other short-dated gilts would be a positive sign.

But this will also depend on how easy it is for institutions to hold DIGIT via standard custodial chains such as Euroclear and Clearstream. Is there a clear path toward integrating digital bonds with CREST and traditional settlement infrastructure? Or will they exist in a complete silo? Any form of friction could reduce uptake. What matters more than any of this, though, is whether the new digital bond will be eligible for use in repo markets on the same terms as other similar gilts. And, if it is accepted by the London Clearing House, other clearing venues, and the Bank of England, how will this work in practice?

Given that the Treasury has said this bond will sit entirely outside other gilt management operations, that may not be the case. And it’s this practical use within the wider market that really matters when it comes to securities. Once again, the real roadblock could be interoperability. And for the UK, which has evidently chosen to integrate digital assets within its existing financial framework rather than build out novel infrastructure, interoperability is even more pertinent. Without this, the pilot risks remaining just that.