Welcome to the thirteenth letter from TheIntersection team.

Our aim is simple: to decode and deconstruct the world of real-world asset tokenisation, stablecoins and DeFi for mainstream professional investors.

In this issue:

- News: GlobalX launches Token ETF, DTTC & tokens

- Data: RWA market crosses $30B milestone

- Analysis: Investing in art using tokens

- Opinion: Always Embrace a New Asset Class

- Our weekly events round-up

And it's all free! If you haven’t already, please subscribe using the link below

Before we dive in, one request: please forward this weekly letter to anyone you think might be interested. We also very much welcome feedback (and contributors). If you want to email us, just drop an email to us at teams@theintersection.news.

Global X launches ETF targeting tokenisation and stablecoins

Global X ETFs has launched a new exchange-traded fund designed to give investors exposure to the growing tokenisation and stablecoin ecosystem. The product — listed in Europe on major exchanges including the London Stock Exchange and Deutsche Börse Xetra — tracks companies involved in building and enabling blockchain-based financial infrastructure. Rather than investing directly in digital assets, the ETF focuses on firms developing the underlying rails — from stablecoin issuers to tokenisation platforms and settlement infrastructure. Why it matters: The launch signals rising demand for “picks and shovels” exposure to tokenisation — as investors look to back the infrastructure powering digital finance, not just the assets themselves.

News in Brief

BlackRock challenges U.S. stablecoin reserve rules

BlackRock has pushed back against proposed rules from the Office of the Comptroller of the Currency that would cap tokenised assets at 20% of stablecoin reserves. The firm argues the restriction could limit the growth of tokenised Treasury funds like BUIDL. Why it matters: The outcome will shape whether tokenised Treasuries can become a core reserve asset for stablecoins.

Franklin Templeton pushes tokenised funds into real-world use

Franklin Templeton’s BENJI tokenised money market fund is nearing $2bn AUM and is now being used in corporate transactions, including M&A payments.

Why it matters: Tokenised funds are moving beyond investment products into operational financial tools.

Institutional wallets and infrastructure accelerate

Banks like Morgan Stanley are preparing dedicated digital wallets to hold tokenised equities, funds and crypto assets, while firms such as Ondo Finance continue scaling integrations with traditional financial networks. Why it matters: The next phase of adoption depends on how easily institutions can custody and move tokenised assets.

Deep Dive — DTCC brings tokenisation into the market’s core

The Top Line

DTCC is moving tokenisation out of experimentation and into live market infrastructure — a shift that could reshape how securities are issued, settled and traded.

The Details

The Depository Trust & Clearing Corporation — the backbone of U.S. securities settlement — has set out a clear path for its new tokenisation service. The timeline is deliberate: July 2026: limited live trades, October 2026: full rollout. This isn’t another pilot running in isolation. It’s a controlled move into production, built with input from more than 50 institutions across banks, exchanges and digital asset firms. What DTCC is building is relatively simple in concept, but significant in impact. The service allows securities already held within its existing system to be represented as tokens — without changing the underlying asset. So:

- Ownership stays the same

- Investor protections remain intact

- But settlement and transfer can happen on new rails

The initial focus is on highly liquid instruments — large-cap U.S. equities, ETFs and Treasuries — where efficiency gains matter most. And the scale is hard to ignore. DTCC already sits at the centre of global markets, with over $100 trillion in securities under custody. This isn’t tokenisation at the margins — it’s happening where most of the market already lives. The shift isn’t about creating new assets. It’s about improving how existing ones move. Rather than trying to replace traditional systems, DTCC is layering blockchain infrastructure into them. The aim is straightforward: faster settlement, better collateral mobility and fewer operational bottlenecks. There’s also a longer-term goal — interoperability. The system is being designed to connect across different blockchain networks, not lock participants into a single ecosystem. Three things stand out: Scale is finally here: Most tokenisation projects operate on the edges. DTCC operates at the centre.

This is infrastructure, not experimentation:The focus is on settlement, custody and post-trade processes — the parts of the market that actually move money.

A hybrid model is taking shape: Traditional systems aren’t being replaced. They’re being upgraded, with blockchain handling speed and flexibility while existing rails handle compliance and control.

The bottom line: DTCC isn’t asking whether tokenisation works — it’s working out how to run it inside the system at scale. If it succeeds, this won’t feel like disruption. It’ll feel like markets quietly getting faster, smoother — and a lot more digital under the hood.

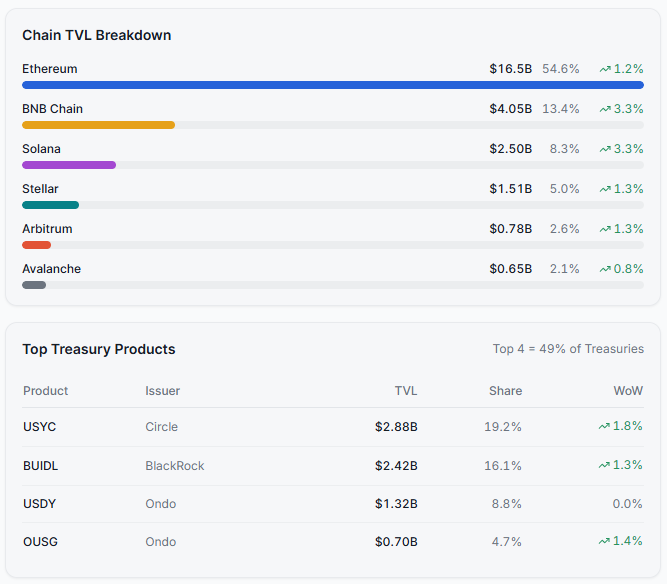

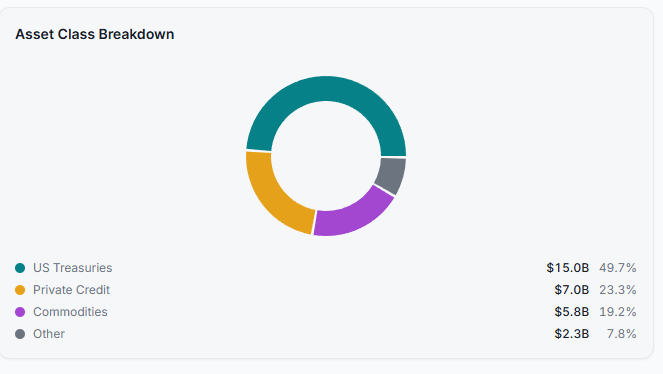

RWA market crosses $30B milestone — Treasuries hit $15B

Total tokenised RWAs surged past the $30B mark this week, reaching $30.2B — a 420% gain since January 2025. US Treasuries hit $15B for the first time, accounting for nearly half the market. Solana RWA has now crossed $2.5B, marking a 10x increase from $215M a year ago.

Morgan Stanley's mid-April announcement of an institutional digital wallet for H2 2026 confirms that Wall Street has fully committed to tokenisation as core infrastructure. Trajectory now points to $40-50B by year-end, with private credit and tokenized equities as the most likely next breakout categories. The risk: 50% concentration in Treasuries means RWA TVL is increasingly correlated with US rate policy.

Key Trends

- 1. Total RWA TVL crossed $30B milestone — up from $5.8B in January 2025 (420% gain)

- 2.US Treasuries reached $15B for the first time, with USYC at $2.88B and BUIDL at $2.42B

- 3. Solana RWA hit $2.5B all-time high — 10x growth in 12 months, now firmly the third chain after Ethereum and BNB

- 4. Tokenised treasuries growing faster than stablecoins for the first time ever (added $2.12B in Q1 vs stablecoins' $1.19B)

- 5. Wallet count nearing 740K, up 5.8% in 30 days — institutional batch transfers driving most of the value

Investing in art using tokens

by Michael Hunter

Investing in art is becoming more accessible through blockchain, as the latest financial technology opens up a new way to buy into the full range of works, from the avant-garde to the old masters. The rise of Digital Ledger Technology (DLT) has made it possible to buy tradeable tokens linked to blockbuster pieces.

One of the best-known names in the trade is Masterworks, a New York-based investment house which buys art and sells shares in what it calls “multi-million dollar, blue-chip artworks”.

With 125 staff based on the 57th floor of Manhattan’s One World Trade Center, the firm buys art. Its portfolios are securitised in line with oversight rules set by the main United States financial regulator, the SEC. Ownership is tracked using the blockchain, right down to specific paintings. This so-called fractional ownership means art buying is now a possibility for many more people.

The blockchain is used to track ownership, right down to specific paintings, making so-called fractional ownership a possibility for many more people. Open and reliable proof of ownership is available to would-be buyers of artists from Banksy to Cecily Brown, and even some old masters.

Masterworks has “over 1,000,000 users from around the globe” according to its website {https://www.masterworks.com/} from first-time buyers to experienced collectors. It has raised over $1.2bn in capital as of January last year. Scott Lynn, its founder, claims to be the first company “to offer art investment products to the retail investing public,” adding:

“Contemporary art has outpaced the S&P for nearly the past 30 years overall, but there has been no way to invest in it.” Blockchain and DLT has changed that. Properly transparent and regulated use of the tech can connect fresh investment capital with a new source of assets, with provenance and colour all of their own.

But with as with any frontier tech, with the opportunity comes risk. There are unverified reports that some globally resonant paintings have been tokenised and offered to investors, via non-fungible tokens or NFTs, without the full regulatory oversight seen elsewhere. Perhaps the most famous example is Leonardo da Vinci’s Salvator Mundi. The renowned portrait of a long-haired, blue-robed Christ holding his right hand up in a casual-looking blessing gesture was sold for over $450mn by the old-school auction house Christie’s in New York. Now in private ownership in the Middle East after the record-breaking auction, this Renaissance masterpiece has been linked with an unregulated fractional sale.

Caveat emptor in the online age

An NFT proves ownership of a portion of a blockchain record, but it does not provide definitive evidence of the physical asset claimed to back it. These tokens are, in this sense, similar to safety deposit boxes at banks. An investor may have the key to an empty vault. The saying “buyer beware” has rung out through the ages for a reason.

Digital finance expert Oliver Oram, the founder of HyYield, an AI-powered blockchain platform, points out that art sales using the latest ownership-tracking tech are part of the wider wave of innovation in the industry:

“Tokenisation isn’t really about the art itself, it’s about infrastructure,” he told The Intersection. “It shows we can turn illiquid, high-value real-world assets into fractional, verifiable and easily transferable instruments.”

He was also the chief executive of Chainvine, which applied the same principles to fine wine and art, as well as other areas. “The asset class changes, but the core challenge remains the same: creating a single reliable record of ownership, provenance and custody.

“That’s where tokenisation adds real value slashing information asymmetry and unlocking capital in private markets and commodities.”

There was a mania for NFTs in everything from internet memes to parts of the so-called “metaverse”, the new form of online space, pioneered in the early part of this decade and now more peripheral. Amid much hype on social media and a slew of celebrity endorsements, the NFT boom was lit up by the $69m sale at old-school auction house Christie’s of an entirely digital work in March 2021. It secured global attention for the artist – Beeple – and his piece, a rendering of a gurning emoji under construction on scaffolding called “Everyday: The First 5000 Days”. The climax of the sale was watched by 22mn people online, with the artworld and the investment industry paying stunned as the landmark price smashed through forecasts.

Times have changed since the heady days of the Beeple boom. The metaverse has been eclipsed by the rise of Artificial Intelligence. Beeple-style emojis and NFTs in general are not as lucrative. Christie’s shuttered its specific digital art department last September, with sales of digital art now run from the 259-year old firm’s 20th and 21st century art category.The closure was a quiet one. At the time, a spokesman for the venerable London firm told the trade press Christie’s “made a strategic decision to reformat digital art sales”. Sotheby’s was reported to have taken similar action in 2024, when the bulk of its specialist metaverse and NFT team left.

Trading volumes in art NFTs, as tracked by DappRadar, a blockchain database site, fell from a high of $2.97bn in 2021 to just $197mn in 2024. Nonetheless, after the boom gave way to a more sober market, it had also set a precedent. Blockchain and digital ledger technology have offered a new route of entry into the art market, as well as wider alternative assets. Concern that fractional ownership could see underlying assets over-securitised is, says Oram, “not fundamentally a blockchain problem — it’s a governance and legal one.” He adds: “You need one authoritative issuer with exclusive rights to mint the token, backed by strong legal title and tightly integrated with custodians, insurers and registries.

“Blockchain gives you immutability and traceability, which is excellent at preventing fraud and unauthorised copying of important works.”

According to Deloitte’s latest Art & Finance Report, covering last year in detail, the use of tokenisation has evolved. “NFTs have come to be viewed less as a new art genre and more as technological infrastructure for distribution and ownership. Interest has shifted toward investment-driven use cases, especially NFTs linked to physical artworks.” The ninth edition of the consultant’s annual analysis said “the novelty-driven appeal” of NFTs “appears to have diminished”, with the technology now being used “in provenance tracking or digital ownership”.

Deloitte found that: “While the initial hype has cooled due to over-speculation and market volatility, the underlying applications of NFTs remain highly relevant....From digital authenticity certificates to programmable ownership rights and resale royalties, the utility of NFTs continues to evolve, offering real solutions to the art ecosystem’s longstanding inefficiencies.”

Oram points out that there is another reason that tokens tracking non-financial assets has appeal: “Art and fine wine attract new capital because they’re culturally familiar and far easier to understand than abstract financial products”, he says.

Digital ledger technology is making art a bigger part of the asset-backed landscape, allowing retail investors to add a splash of tradeable colour to their portfolios. It means owning art is no longer solely the preserve of multi-billionaires. As tokenisation moves into the mainstream, the capital flows that will be unlocked by properly transparent use of the technology could become a spectacle in itself. Investors and the industry will be watching closely, as this eye-catching corner of the market frames the outlook for frontier financial tech.

Always Embrace a New Asset Class

by Charlie Morris, CEO ByteTree Research

New asset classes come around every few hundred years, and you’ll know when one does because it will terrify the establishment. Just look at Bitcoin, on the face of it, a simple electronic ledger. Rather than be amazed at vast wealth creation at the hands of the network effect, and the possibilities for computers to transact, the establishment treated it just they would have done to a witch in the Middle Ages.

In early civilisation, there were commodities, art, and real estate, the physical assets, and of course, debt. Debt was the original form of money and the first virtual asset that likely preceded official coinage. Equities took off at the time of the English and Dutch East India companies. They were important because they provided a legal framework for joint-stock companies, allowing collective labour to be another’s profit and enabling companies to scale.

Since the 1980s, we’ve had derivatives, hedge funds, private equity, infrastructure, and private credit, but none of these are asset classes. Private equity is still equity, and private debt is still debt. Infrastructure is real estate, hedge funds are strategies, and derivatives are the bookies. You can own them, but don’t expect the diversification benefits associated with genuine asset classes.

When Bitcoin came along, it was a new asset class. The idea of digital value was groundbreaking. It is truly decentralised, cannot be copied, and can move across borders 24/7 in a permissionless manner. Some were excited, and others horrified, yet it was no more than a computerised ledger.

It caused so much grief because it represented a new form of financial freedom, for everyone, and everywhere. Until that point, governments had been able to control the money, but now that was under threat. Without control of money, governments lose the most critical part of their power structure.

Over the years, it soon became clear that Bitcoin was not as scary as first feared, and as compliance, custody, regulation, and acceptance, improved, it would coexist with the prevailing systems. Governments started to open up. In 2004, London managed to list a gold ETF before they managed it in New York. Two decades later, the tables have turned as New York launched a Bitcoin ETF two years before London.

There are millions of crypto projects, but the one that stands out is Ethereum. This has paved the way for tokenisation, which means anything, from shares to dollars, can be held in cyberspace and represented by a digital token.

Dollars on the blockchain have become known as stablecoins, a sort of joke in a once volatile and nascent industry. They came from nothing and have grown to $320 billion and driven initially by government resistance to change. In the early days, the banks blocked interactions with crypto exchanges, and the solution was for the crypto industry to bank themselves, once again, in a decentralised manner.

Many have said that Bitcoin is a solution in search of a problem, but if that was true, why would the asset class have grown so much? Why would stablecoin issuance continue to grow? And why are the banks getting involved. In recent weeks, Morgan Stanley has launched an Bitcoin ETF, Goldmans Sachs have stated their intent to follow, and Charles Schwab are opening up crypto trading to their customers. This follows the early lead by iShares, Fidelity, WisdomTree, and others.

Crypto has been a driver of innovation. Therse days a young entrepreneur is priced out of the stockmarket where listing fees have skyrocketed. Instead, they go to crypto and launch technology projects with less cost and red tape.

Then comes AI, where the agents will never call the bank. As they grow, their direct involvement in trading and commerce will explode. They will not use traditional banking as we know it, and head straight for crypto. They may opt for stablecoins over Bitcoin, but that doesn’t matter. The stablecoins run on Ethereum, and other “layer 1” platforms, and increased circulation and activity drives their value higher, as they receive fees.

Bitcoin’s direct linkage to the growth in utility within digital assets is perhaps less obvious, but it has remained the reserve asset of this asset class since inception in 2009, with no signs of that changing. In that regard, bitcoin has something in common with gold, which has seen $20 trillion of value creation since 2020. Like gold, Bitcoin is a highly liquid reserve asset, whose fortunes are more closely linked to the digital world than the real world.

Today, Bitcoin, Ethereum, and stablecoins make up $2.1 trillion of a $2.6 trillion asset class. The global wealth management industry looks after $170 trillion dollars in assets, and their exposure to digital assets is close to zero, especially in Europe. It stands to reason that digital assets are here to stay and will be much larger in the future than they are today.

The Bitcoin, Ethereum, and BOLD ETFs are here, with the regulatory hurdles largely overcome. It is oft said that diversification is the only free lunch in investing. When a new asset class comes along, it is much better to embrace it that run away.

Events on our radar

DigiAssets Connect Zurich, 16-17 June - Custody, banking, and institutional infrastructure – tickets HERE

European Blockchain Convention 12, Europe’s Deal Floor for Digital Assets. BARCELONA · 16-17 SEPTEMBER 2026 - tickets HERE